Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Pair Trades Review

Two weeks ago JP Morgan’s Marko Kolanovic recommended Long Oil vs. Short S&P trade & BAML’s Michael Contopoulos recommended Long High Yield vs. Short S&P trade. Jeffrey Gundlach had recommended a Long High Yield Closed End Funds vs. Short S&P trade a few weeks ago and he reiterated that trade in last weekend’s Barron’s Roundtable. Bill Gross had simply suggested buying High Yield Closed End funds outright a few weeks ago. His recommendations were DPG, PCI & UTG. Earlier this week, he reiterated UTG in his conversation with CNBC’s Brian Sullivan.

How did these trades work out after a torrid week that ended with a scorching rally? It seems clear in retrospect that the lows of Wednesday, January 20 were at least a short term low. So we measured the performance of the above trades from the lows of January 20 to the close on Friday. Look at the performance of the trade components over that week & half:

- Long Oil vs. Short S&P – USO up 22% & BNO up 29% vs. S&P up 7%, (QQQ up 7% & IWM up 8.3%).

- Long High Yield CEFs vs. Short S&P – DPG up 18%, PCI up 5.4% & UTG up 22% for an average gain of 15% vs. S&P gain of 7%.

Kudos to the gurus who recommended these trades. This is just fantastic. See Donald Trump is right. Watching TV is an efficient way to get smart.

No one had discussed Long Gold Miners vs. Short S&P Trade. That recommendation would have been just as great.

- Long Gold Miners vs. Short S&P – GDX up 13.5%, NEM up 24% & ABX up 27.5% vs. S&P up 7%, QQQ up 7% & IWM up 8.3%.

These proved to be essentially going long more oversold assets vs. going short less oversold assets. By the way, TLT was only up 70 bps during that week & half. So the trade of 2016, Long TLT vs. Short S&P failed during this week & half long bounce.

What happens next? Is this a real turn in these asset classes or just an oversold bounce? That depends on why the bounce took place and what happens to the fundamentals? One technician’s view below says we are in a 2008 analog while another technician argues below for a change in the leadership for awhile.

2. “Kuroda didn’t know what Kuroda was going to do“

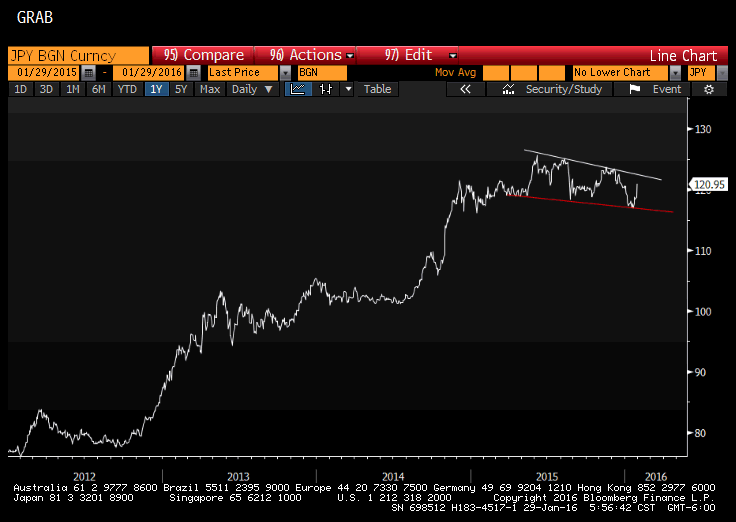

Remember the bounce off of 1812 on Wednesday, January 20 was a classic hard rebound from a major support level. It got extended into something else thanks to more QE commitment from Mario Draghi the next morning in his ECB speech on Thursday, January 21. The next morning Kuroda “laughed his head off” in his BTV interview and “said there was 2/3rd of the JGB market he had not bought yet“.

Then Kuroda stunned the world on this Thursday night by announcing negative interest rates after having denied such a possibility the week before at Davos.

- Timothy Reazor @TJReazor – And the #Yen falls out of bed

- “When stocks are falling this much, it’s hard to justify not acting,” said one of the individuals, who has occasional contact with Kuroda

- Raoul Pal @RaoulGMI – Well, $JPY chart pattern is now finally clear. It is a wedge and its next target is the high 130’s. $ rally goes on

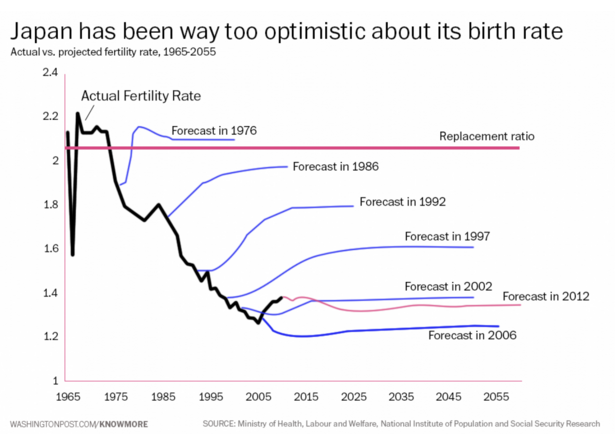

- Charlie Bilello, CMT @MktOutperform – One day the BOJ will go to -10%, corner the JGB mkt, & buy every Nikkei company. But still, Demographics is Destiny.

3. Come on Mr. Cashin, will you get bold?

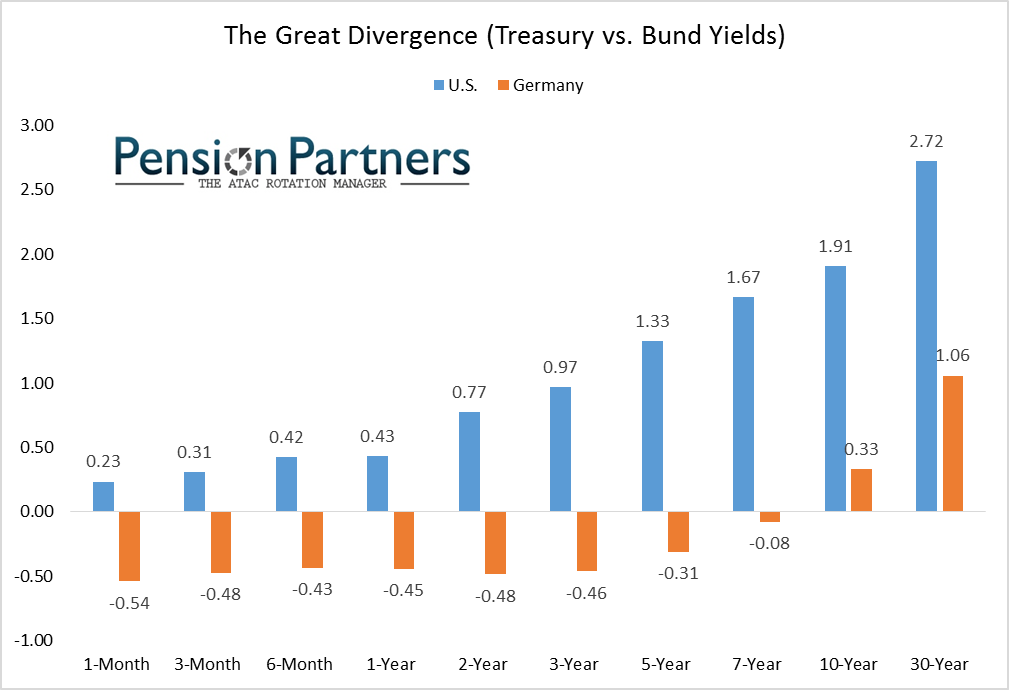

The venerable Art Cashin has said and keep saying “we will see 0% before 1%“. Isn’t that so passé, Art? No one really expects 1% any more. Isn’t it time for you to proclaim “we will see 0% before we see 0.50%-0.75%“? Just look at the evidence:

- Charlie Bilello, CMT @MktOutperform – US Real GDP: +1.8% yoy German Real GDP: +1.7% yoy The massive differential in rates…can this persist?

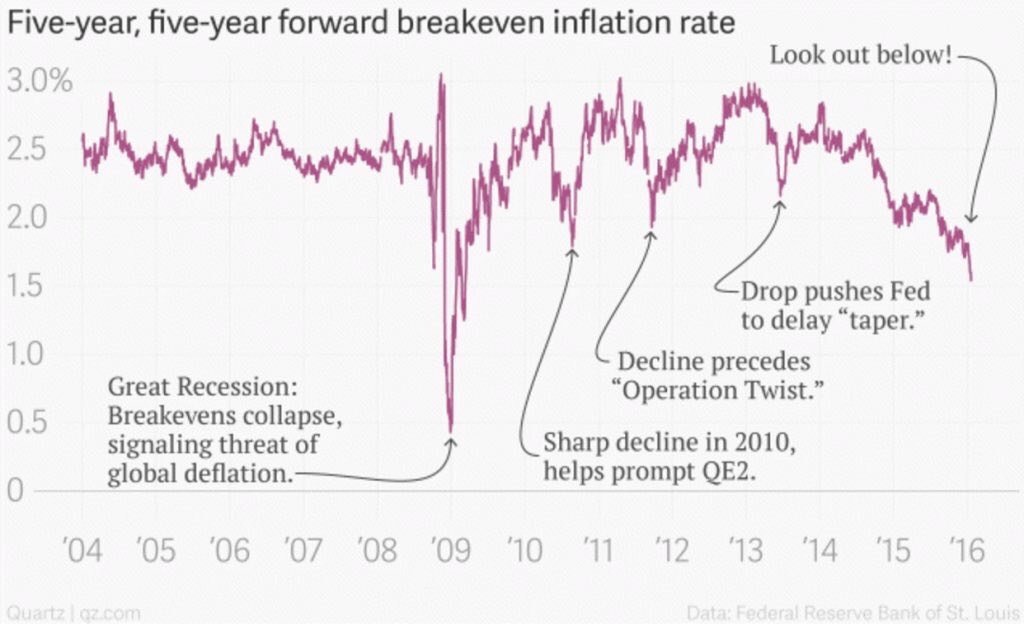

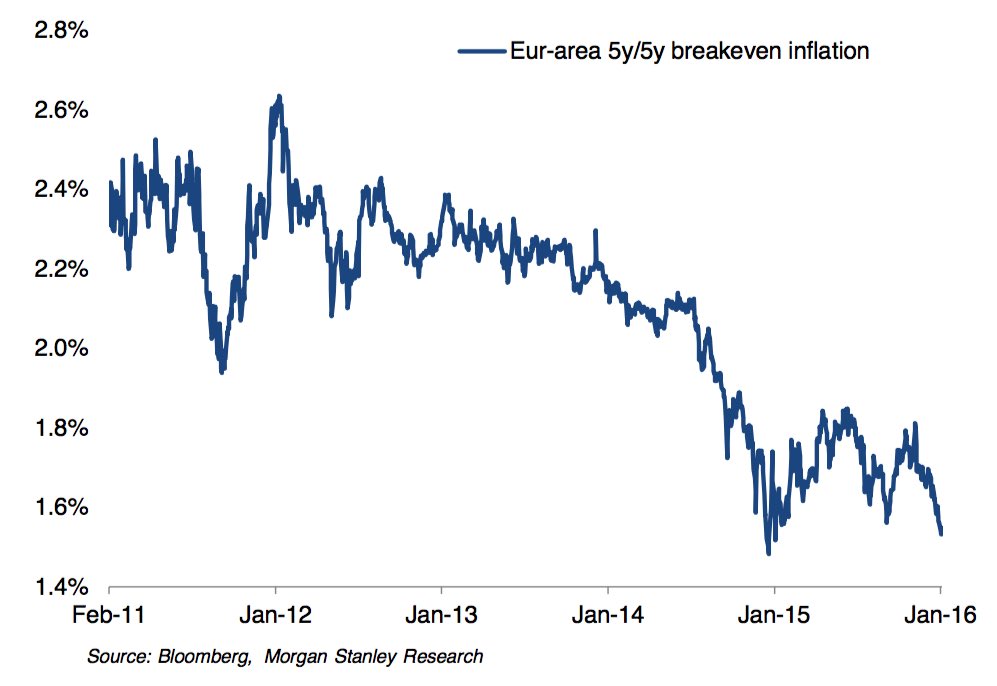

- Lawrence McDonald @Convertbond – Five year, 5 year forward breakeven inflation US vs Europe Both in plunge mode with Fed hiking and ECB in QE??

- @Sully – how many rate hikes this year?

- Gross – I don’t think they should raise any but I do think the Fed is focused on historic models which are focused on employment; they might raise twice … I think they are using the wrong road map

We will get a better sense about employment next Friday. Then we can revisit this question.

4. R-Word

- David Rosenberg – All we have to do is avert a recession & upside surprises will abound through the balance of the year

- @Sully – will the US economy be in recession 12 months from today?

- Gross – not but near recession

- @Sully – will the US economy be in a recession 24 months from today?

- Gross – I think between now & then US will experience a recession; its been a long time; a mild recession in the US is hard to avoid when the rest of the world is significantly depressed; ultimately that lends a flavor to what we experience here

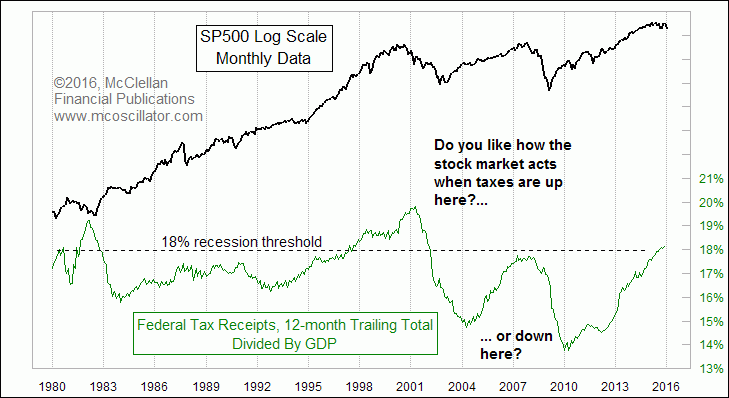

- Thursday – Tom McClellan @McClellanOsc – Should be #1 debate topic. Every time federal taxes >18% of GDP, we get recession. Now 18.2. http://www.mcoscillator.com/learning_center/weekly_chart/us_taxes_returning_to_economy-killing_level/ …

5. Treasuries

Treasuries may have underperformed the S&P this week but they did rally in a sharp bull-steepening thanks to the FOMC statement. The 5-year & 3-year yields dropped 15 bps & 13 bps resp while the 30-year yield fell by 7.5 bps. If prosperity is a lady, then the un-faint hearts won her by buying the 5-year auction at 1.49% at 1: 00 pm before the Fed. Why? Because the 5-year closed the week at 1.33%. A 16 bps move in two & half days, wow.

The 10-year yield closed the week below 2% at 1.9226%. Jeff Kilburg of CNBC Futures Now stated his target as 1.67%. In contrast:

- Raoul Pal @RaoulGMI – #Bonds US 10 yr yields have broken key head and shoulders neckline support. My target remains 0.5% by 2017

That is a strategic intermediate term call. Next week’s jobs number may determine the near term direction.

6. US Stocks

The huge rally on Friday was almost a perfect storm for the shorts. Kuroda and the need to mark up equity portfolios after a horrendous month were two obvious forces. But there was another – a huge rebalancing of asset allocation that had become skewed by the steep fall in equities & big rally in bonds. So there was a forced need to buy equities & sell bonds – some $50 billion worth according to Bear Traps.

The real question is what happens after such a perfect storm? Actually the bigger question is how far this equity rally can run? Recall that Tom DeMark had called for a 5%-8% move and others had spoken about 1960-2000 target band. By Friday the rally had gained 7% and 1960 was merely a good day away. The call from Lawrence McMillan of Option Strategist seems consensus:

- “In summary, we expect a short-term rally to a level above the declining 20- day moving average of $SPX, perhaps to the 1960 level or so. However, unless the intermediate-term indicators begin to improve, we continue to view the intermediate-term as bearish”

- “Boroden believes that the Jan. 20 low of 1,812 reached in the S&P intra-day is now a key level, but it doesn’t represent a genuine bottom. She is watching for another downside failure to occur soon.”

- “The last two rallies lasted for just 10 and 11 trading days. Therefore, Boroden thinks that this current rally will hit the 11-day mark by next Thurs., Feb. 4, and it is unlikely that the current rally will last beyond that 11-day window. That is also exactly when her methodology noted that the S&P 500 is likely to change trajectory again … Boroden also pointed out that there is a ceiling of resistance running from 1,911 to 1,915, and another ceiling running from 1,978 to 2,000.”

If you watch the 7-minute clip, you will see that Boroden’s longer term targets for the S&P are 1350 & 1225.

- “Hemachandra was an Indian mathematician who discovered these numbers before 1,000 CE. Al-Khwazirami published Hemachandra’s work in his Arabic treatise Hisab al-Hind or Arithmetic of the Hindus. The western word Algorithm is reportedly a derivative of Al-Khwazirami. Fibonaaci learned of these numbers from Al-Khwazirami’s book.”

7. Analog of 2008?

Richard Ross of Evercore ISI was emphatic in his call in on CNBC FM 1/2 on Friday:

- “Technicals suggest this is precisely January of 2008; look at the unintended consequences of the overnight move; We have a very strong Dollar & that strong Dollar will continue to weigh on the Crude complex, EM & High Yield; look at the 2-10 year spread; it looks exactly like oil which looks exactly like high yield which looks exactly like private equity; strong finish to January but we are still playing out with 2008 analog; we are looking at a normal cyclical bear market correction consistent with the cross asset class decline we have seen; a 20% correction to 1670-1700;”

- “it is going to be a very challenging first half but ultimately we go lower to go higher in the second half; I don’t think this is a secular bear market; stage will be set for a very nice finish to the year”

“Well I’ve been posting it for days on end and if you traded it you banked, spooky as it is, but here it is”:

From a more fundamental point of view:

- ValueWalk @valuewalk – Zulaf says in note to clients “what US housing was in 2008 is China Today” http://www.valuewalk.com/2016/01/soros-china-warning/ …

8. An outperformance call on EM, Crude & Commodities vs. S&P

J.C.Parets has been steadfastly negative on EM relative to S&P. He has also been steadfastly negative on Gold & Gold Miners. Last week, he turned positive on Gold and wondered whether breakdown in GDX was false. Well, GDX responded with a 9.5% rally this week and Newmont with a 20% rally.

- I think that a very telling chart right now is the S&P500 vs the MSCI Emerging Markets Index.

- “Notice how momentum is putting in a bearish divergence at the recent highs. With the ratio making a new 11-year high this month, momentum put in a lower high. This is what we call a bearish divergence. I think there is a very good chance that we get back under 5.75 in this ratio. There are two ways to take advantage of this.

- One – keep it simple stupid and just play the spread. For every $1 short the S&P500 $SPY, we are long $1 of the MSCI Emerging Markets Index $EEM. Risk management-wise, we only want to be short this spread if we are below the upper of the two parallel trendlines that define this channel.

- The second way is much more global and “theme-based”. I think there is a lot going on right now as money flows back into emerging markets and commodities that effect them like Crude Oil and Copper.”

- Thomas Bruni @BruniCharting – @allstarcharts Don’t tell’em it’s occurring at a key resistance level & Fibonacci retracement in $SPY / $EEM either.

On the other hand, Tim Seympur of CNBC FM asked viewers to sell/short EEM at $31. Who is right? Depends on what the Dollar does. And that may depend on next week’s payroll number.

9. Gold

What a great week for Gold & Miners! What’s next?

- Raoul Pal @RaoulGMI – With yet another country headed to negative rates, #Gold is going to become a big focus later in 2016. Possibly another sell off first tho’

On the other hand,

- ValueWalk @valuewalk – Three Major Reasons For Gold In 2016 [INFOGRAPHIC] http://www.valuewalk.com/2016/01/three-major-reasons-for-gold-in-2016-infographic/ … $GLD $GDX $VIX $OIL

On a more near term basis from @365CryptoFX

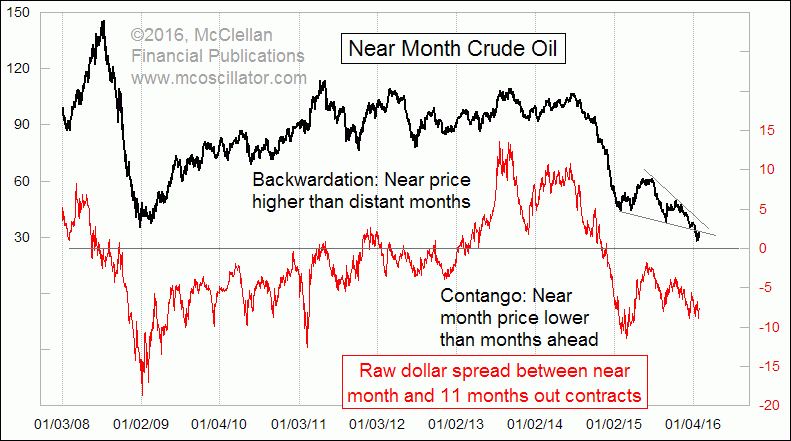

10. Oil

What is the major force behind oil? Is it the Dollar, is it Iran or is it Contango?

- Tom McClellan @McClellanOsc – Oil contango is pretty big now, a sign of a bottom for near month oil futures price.

What about Copper?

- Bespoke @bespokeinvest – Copper was up 3% for back-to-back weeks for only the third time since it peaked in Q1 2011.

Is this a statement or a warning? Next week’s payroll number will shine a light on this as well.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter