Ivan Petrovich Pavlov (1849-1936) & his experiments with dogs are now synonymous with studies in temperament, conditioning and involuntary reflex actions. Unfortunately for him, Pavlov lived before injecting hormones was became possible. Imagine how much he could learned & demonstrated had he experimented with injections of hormones into his dogs. He could increased or decreased doses of hormones to study how aggressive behavior on in dogs waxes & wanes. Imagining the experiments he could have run boggles the mind.

But we don’t really need to imagine, do we? Modern Pavlovs are engaging in insane experiments right before our very eyes, experiments that are driving modern dogs to crazy behavior. At least experiments of old Pavlov were in isolation & didn’t alter lives of ordinary people. In contrast, experiments of these modern Pavlovs are impacting the entire world.

Who are these modern Pavlovs? They are the world’s central bankers. And their dogs are the big banks in their countries. The primary job of a Central Banker is to regulate the behavior of the banks and they do so by raising or lowering monetary liquidity injections. Over the last 100 years, banks have been conditioned to respond meaning alter their behavior when central bankers change the doses of injections. When central banks make big mistakes in their dosages, banks go nuts & bubbles rise. When the dosages are then cut, banks contract & bubbles go bust. We have all seen this happen in 1999-2000 & in 2006-2008.

But what happens when central bankers, these modern Pavlovs, go nuts? What happens to their dogs, the big banks? How does that impact economies & common people? Just look at the carnage in markets in the last two weeks.

By the way, we are actually being respectful & polite in calling these central bankers as modern Pavlovs. Investment luminaries are being far less kind:

- Marc Faber, Editor of Gloom, Boom & Doom Report on Fox Business on Thursday, February 11- “The central banks remind me of the movie ‘One Flew Over the Cuckoo’s Nest’ where the doctors are the insane, whereas the inmates are actually quite common people with common sense and normal, … This is exactly what I think is happening today“

And what is the most nutty experiment these modern Pavlovs are doing? Negative Rates. We are simple, polite folks. We wouldn’t dare to call these august personages insane. We leave that to luminaries like:

- David Rosenberg of Gluskin Sheff on Bloomberg TV on Thursday, February 11 – “The latest experiment on negative rates is falling flat on its face, but in a classic case of following Albert Einstein’s definition of insanity, the academics who run the world’s central banks show no sign of backing away from a policy that is undermining the banking system“

Mirror Mirror on the wall, who is the nuttiest Pavlov of them all?

1.Harakiri on January 29?

Bank of Japan Governor Haruhiko Kuroda is an aggressive central banker who has tried to carry out the mandate of his boss, Prime Minister Abe. His goal has been to inject growth into the Japanese economy via injections of monetary liquidity & thereby weaken the Yen. Japan’s main market and competitor is China. China’s economic & monetary system is facing mammoth challenges & China could decide to devalue its currency in one large onetime cut. To protect Japan against that & to shore up its falling stock market, Kuroda acted on Friday, January 29.

Doctors have understood for centuries that you don’t throw the human body into a shock by sudden & very large injections. You gently increase the dosage as your monitor the body’s responses. But modern Pavlovs like Kuroda obviously have no patience with these wishy washy approaches.

So Kuroda stunned the entire world on Friday ,January 29 by announcing his new policy of negative interest rates after categorically assuring his own country & the international Davos summit, just a week before, that he had no plans to do.

You want to see what a shock of this magnitude does to the body of a monetary system? Look at the simple charts of the Yen & the Japanese stock market. Focus on the last vertical time period bar in the charts to see the vertical rise & steep fall from end of January to this Friday:

(ETF of Japanese Yen to US Dollar)

(Japanese Stock Market ETF)

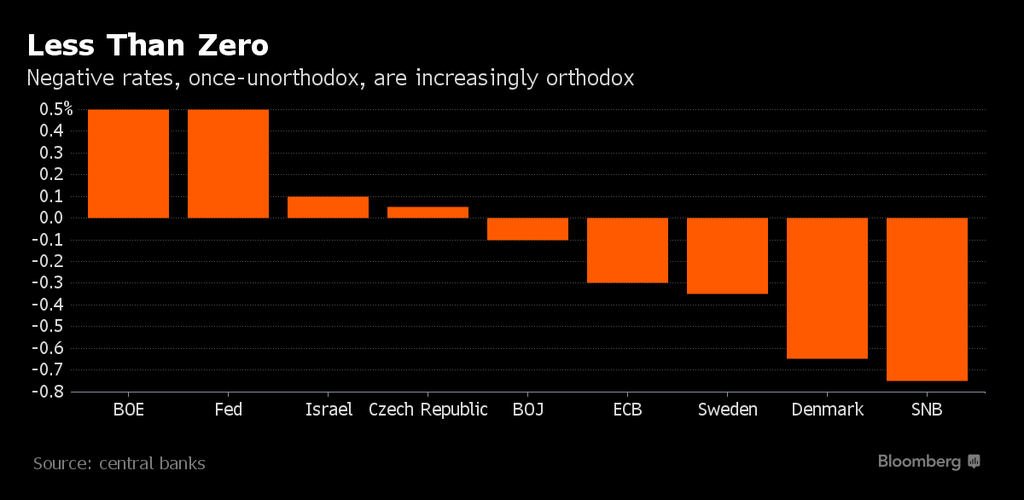

No country or economy is an island these days. And the negative interest rates announcement by Kuroda instantly dropped interest rates around the world. Look at the chart below from two weeks ago to see how this insanity of negative interest rates is spreading in the world

2. Insanity of Negative Interest Rates

Everyone knows how banks make money – they entice depositors to put their money in the bank by paying interest to depositors & then the bank lends this money to borrowers at a higher interest rate & pockets the difference in interest rates as profit. This is called Net Interest Margin (NIM). Higher the NIM, higher the profit of the bank. Simple.

But what if the economy is weak and borrowers don’t need to borrow because they don’t have profitable opportunities to invest? Banks cut the interest rates on their loans and in turn cut the interest rates they pay the depositors. So, the modern Pavlovs said, why not take this to the ultimate level? Why not entice borrowers to borrow more by actually providing NEGATIVE interest rates on loans? Meaning by paying borrowers to borrow. Meaning telling borrowers they would need to pay less money back than they borrowed. Free money in other words.

Wait. Banks can’t pay money to both depositors & to borrowers. They would go bankrupt and only one of the Jacobson, Julius & Harshberger attorneys would be able to help them then. So banks try to protect themselves by paying zero interest to depositors and finally charging depositors for the privilege of putting their money in banks. So, at best, banks would make zero profits. But that assumes depositors have no choice but to meekly pay charges to banks for keeping their money in the banks.

Folks, this is going back to an era when there were no banks, not at least for the poor & middle class. How did such people store their money in those days? By buying Gold and burying it in several places in their farms. And guess what asset class has gone up in a vertical spike in the last two weeks in today’s modern world? Gold.

(Chart of GLD, the Gold ETF)

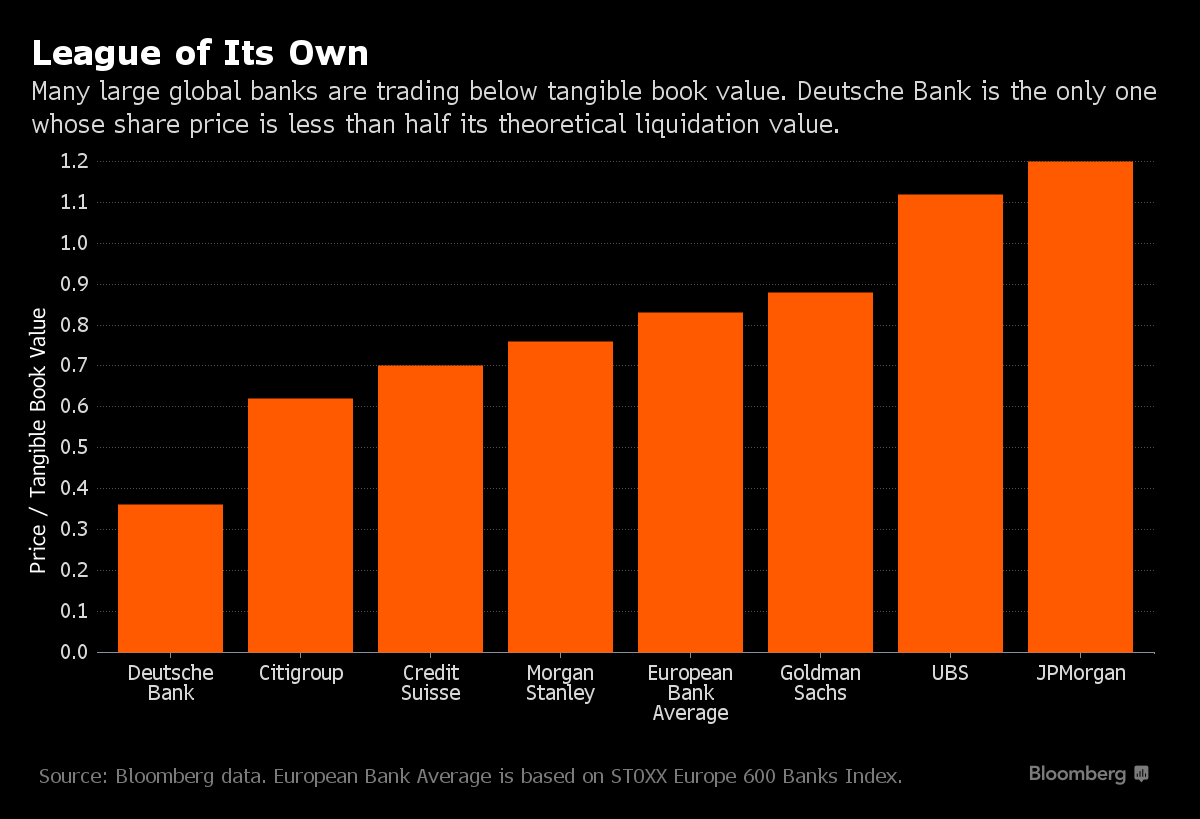

That’s fine for those who can buy Gold & protect their present & future purchasing power. But that is hell for banks & their profit margins. What profit margins? Banks stand to make big losses in this era of free money to borrowers & charges to depositors. What happened to stock prices of banks & their credit ratings? Look at the chart below:

By the way, the above discussion doesn’t even touch the problem of bonds that pay negative interest. And how big is that problem? The world has $7 trillion of negative yielding bonds, according to Larry McDonald of Societe Generale and a veteran of the Lehman bankruptcy.

But why is Deutsche Bank, that proud symbol of ultra-conservative Germany, so hard hit? To understand that, we need a small detour via Europe & the 2008 crisis.

3. Insanity in Europe

Culture plays such an important role in success & failure of nations and societies. The United States let Lehman go bankrupt and then marshaled all its resources to put $800 billion in its banks, forced banks to write off bad debts, push up liquidity ratios & increase equity capital. Thanks to the combined actions of Secretary Hank Paulson, Fed Chairman Bernanke & Secretary Geithner, the US banking system was fixed in 6 months by March 2009.

That is neither the culture of Japan nor of Europe. That is why Japan’s banks & Japan’s economy have been virtually moribund since 1989. Europe is just as bad. They have done virtually nothing to write down bad debts or force European banks to increase equity capital. And the European economy needs healthy banks much more than America does. Because, as veteran banker Bill Rhodes explained this week on CNBC, “75% of credit creation in Europe comes from the banking system because Europe doesn’t have well developed capital markets that America has“. Add to that problems of debts of peripheral Europe and you see why Italian Banks, Portuguese Banks and other European banks are in so much trouble.

But Deutsche Bank, the proud standard bearer of that economic behemoth Germany? And why should Bank of America & Citibank fall so hard because of Deutsche Bank & other European Banks? Didn’t we just say US banks were fixed?

4. Most “Dangerous” Banks in the World

What would you call a dangerous bank? Not one that is about to go bankrupt. That is the problem of that bank & its owners. A truly dangerous bank is one that is systemically risky, meaning it can bring down the entire global banking system.

So which is the most systemically risky bank? That answer was provided in November 2011 by Nobel Laureate Robert Engle & Professor Viral Acharya of NYU Stern Volatility Institute. The most risky bank was deemed to be Deutsche Bank followed by BNP Paribas & Barclays PLC.

But why would problems of a German bank matter create such fear in the entire world? One word – Derivatives. Reportedly Deutsche Bank has $55 trillion in derivatives on its books – yes $55 trillion or 3 times the size of America’s GDP, 5.5 times the size of Chinese GDP or 27.5 times the size of India’s GDP. That is why every market in the world fell hard this week, including the Mumbai Sensex.

Remember 2008? Why a relatively small entity named Lehman created such huge problem for the world? Because these derivatives are counter party agreements with other major banks & there are multi-partite swap agreements in place between European Banks and US Banks & other European banks. Through these agreements, problems at one bank become the problems of all its counterparty banks Now you understand why stocks of Bank of America, Citibank and Goldman Sachs fell so hard & so fast in the last two weeks.

Understand that these derivatives are not a problem by themselves. They pose theoretical risks not practical risks as long as the credit ratings or health of the banks are fine. But the moment the credit rating of a bank comes in question, then the theoretical risk of derivatives becomes practical and real. And that happens to a behemoth like Deutsche Bank, it puts the entire banking system at risk.

And what can put credit ratings or health of banks in jeopardy? Sustained & material threats to the profitability of banks. And what is today’s source of such threats? Negative Interest Rates. The rates in Germany are now negative all the way from 1 year to 7 years. How can German banks be profitable in their lending operations under such horrific conditions?

And what might happen to such banks if current conditions persist? Raoul Pal, publisher of Global Macro Investor, addressed this on CNBC on February 3 – “stocks of many European banks are on the path to going to zero“. And which banks did he mention as possibilities? Deutsche Bank, Credit Suisse, Banco Santander, RBS, Barclays etc. Listen to him yourselves in the short five minute clip below:

Man, this would make 2008 & Lehman look puny, right? Now ask yourselves, why are the highly educated well experienced august central bankers engaging in such insane experimentation like negative interest rates?

5. Are these Modern Pavlovs Insane or Compelled to Insanity?

What we discussed above are the symptoms. What then is the disease that is the cause of these symptoms? The enormous rise in global debt post 2008. Just look at America, the strongest economy in the world. The debt burden of US has risen from $10 trillion in 2008 to $19 trillion now – an increase of 90%. China is at the other extreme with a far more meteoric rise. Europe is in between and Japan is worse than Europe.

High debt levels are OK as long income growth is greater than the growth of debt. And the income of global economies has been falling. As a result debt payments have begun taking greater share of income produced and so less income is available to finance future growth. Central banks, especially the US Federal Reserve, have been trying to create growth by creating a wealth effect by artificially raising asset prices like stock markets. This has worked some in America but not so much in Europe where stock ownership is small & credit creation is mainly via the banking system.

As a result, the contagion of deflation has been spreading around the world as we have been warning since October 2014. Nothing scares central bankers like deflation and that is what is prompting them to go nuts in panic & resort to insane self-defeating measures like negative interest rates. Their only alternative is to throw up their arms and resign en masse.

The real problem is that the Executive & Political branches of all major governments have washed their hands of this mess and left it to the Central Bankers. Europe has been in an economic civil war between the poor debt ridden Southern & Peripheral Europe and the Rich North led by Germany. Any real solution would involve writing off debts of Peripheral Europe and implementing real labor reforms. The first would mean an instant transfer of wealth from North Europe to South-Peripheral Europe while the second would mean total change in work rules for Southern-Peripheral Europe. North won’t tolerate the first and South-Periphery won’t tolerate the second. China is facing a greatest bust in human history and Japan has to stop being Japan as the first step towards real recovery.

That leaves, as usual, the President of USA as the one leader who can bring the world together to fight this contagion. To do that, President Obama will first have to admit he has been wrong in his message and substance for the past 8 years and change his policy completely in the last 10 months of his presidency. This is one case to which we will assign a negative probability.

President Bush didn’t have to let Lehman fail. He could have bailed out Lehman for a few months by injecting $20 billion into Lehman in September 2008. That would have been a punt and dropped the crisis into the lap of President Obama just as President Clinton dropped the bust of 2000 into the lap of President Bush. It was courageous of President Bush to let Lehman go and that crisis ended up cleaning up the US banking system. But it destroyed the reputation of President Bush forever.

President Obama is not going to make the same mistake. He will do everything he can to push this mess into 2017. That is why we said back on January 2, 2016, this is going to be an interesting year indeed.

6. Before We Collectively Slit our Wrists

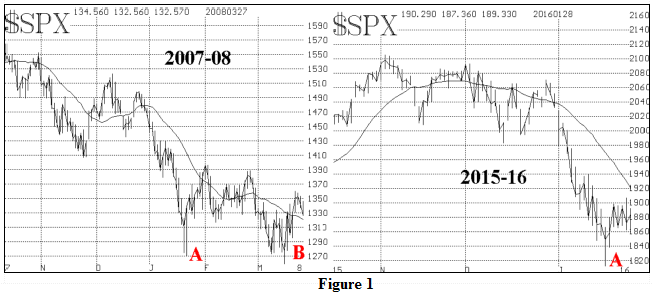

This past week was climactic. Gold & Interest rates went on an asymptotic & parabolic rise and that usually doesn’t last. Fear was rampant and that doesn’t last either. William Dudley, President of the New York Federal Reserve, said categorically on Friday that “negative rates should not be a part of the conversation” in America. That was important and reassuring. And the markets reacted so. Deutsche Bank announced a $5 billion buy back of its bonds, a symbolically important step. And the Deutsche Bank stock rallied by 10% on Friday.

And remember the fire in February-March of 2008 was also followed by a soothing rally in the spring.

- Lawrence G. McMillan ?@optstrategist – Is it looking like 2008 again? $SPX

Remember the next meeting of the European Central Bank is on March 10 and the next meeting of the US Federal Reserve is on March 15-16. So the markets will begin looking forward in hope to these meetings. If past is prologue, then some semblance of peace should prevail until then. But this is rank supposition on our part and it could prove totally false especially if some central banker says something dumb in the next couple of weeks. We don’t know as we said and nobody else knows for sure either.

But we do know one thing. That both President Obama & the US Congress hope that, if there is to be a B in the above 2016 chart ahead, then it happens in 2017.

Send your feedback to [email protected] Or @MacroViewpoints on Twitter

Thanks for that econo-finance-politic analysis. BTW: Negative Probability ?? ….. let’s hope more Pavlovs (& dogs) go for that experiment …