Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance

- “not omnipotent and omniscient“.

These words are part of a quote from Jim Chanos which reads:

- “People are beginning to realize the [……………..] is not omnipotent and omniscient,” he said. “In fact, like many of us, sometimes they don’t have a clue“

Mr. Chanos used the above words for the Chinese leadership. But they are just as suited for the FOMC. And that might well be the real reason why the US stock market sold off so viciously in the last two and quarter days. The minutes were more dovish than the consensus expected and that did lead to a fast rally that turned Dow positive from a 160 points drop on Wednesday morning. But the rally reversed almost immediately thereafter and the stock market closed down hard. The selloff accelerated on Thursday and the pace & ferocity of the selloff was more intense on Friday. It was as if the minutes had revealed a potential hike of 50-100 basis points in the September Fed meeting.

Why did the dovish minutes create such a selloff? The consensus in the market was for some degree of conversation about a September rate hike. The minutes did not suggest that at all. That was evident by the steep fall in the short end of the Treasury curve – 15 bps in the 5-year yield, 15 bps in 3-yr & 10 bps in the 2-yr. So there is no doubt what the minutes signified.

So why the precipitous fall in the US stock market? We think people suddenly realized that the FOMC doesn’t have a clue. In a sudden stroke of mental lightening, investors realized that the FOMC is neither omnipotent nor omniscient. Forget being omniscient, people realized that the Fed doesn’t have a handle on the economy. And the belief in the infallibility of the Fed was the main foundation of the 5-year stock market rally. A rudderless economy piloted by a Fed that is almost clueless as the rest of us – that doesn’t justify current multiples, does it?

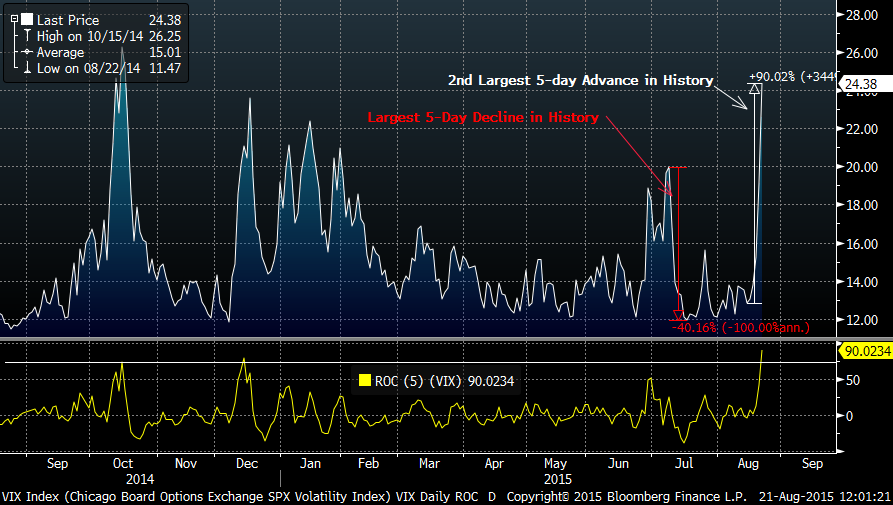

All of a sudden, this light went on and the foundation on which the resilience of the US stock market was based suddenly crumpled. And VIX soared as if shot from a cannon:

- adam warner ?@agwarner – OK, its the 3rd biggest 1 day $VIX spike ever, and THE biggest premium above the 10 Day SMA ever

- Charlie Bilello, CMT ?@MktOutperform – … 2nd largest 5-day spike in history (trails only ’11). Follows largest 5-day decline last month

And then there is the other small matter of transparency or honesty. It is easy to see that the minutes released this week differ substantially from the statement released during the July FOMC meeting. How is that possible? Unless the minutes “released” this Wednesday do not mirror what was actually said during the July FOMC meeting and de facto reflect what the current thinking of Fed. Candidly put, these are not “minutes” but a new statement on updated thinking of the Fed.

This Fed clearly believes that they have to guide the market’s thinking and, in fact, correct the market when they think the markets are wrong. The Fed also believes that they can, via their public comments, tactically manage markets. As we recall, Jeff Gundlach had criticized the Bernanke Fed for doing this during the multitude of Fed-head comments during the taper tantrum of 2013. And the Yellen Fed is being worse or, may we say, more duplicitous than the Bernanke Fed.

Whether they are being duplicitous or just clueless, the stock market selloff shows that, at least for now, the Fed’s credibility has suffered a big blow. That, we think, is the real driving force behind this week’s sudden liquidation of stock positions.

A less damaging criticism was delivered by a veteran insider on Friday morning. Peter Fisher, the Treasury veteran, the man who manned the Treasury desk during the 1998 crisis was blunt on CNBC Squawk Box:

- “I think we also have to unpack a problem with the Fed here. This is the most telegraphed move in history that we expect to come some time but its meaning, its significance is still remote to us; The Fed has been publishing, every member of the Fed publishing their own forward path of interest rates ; they have to get on one page; … their most important output is the expected path to short term rates”

- “They’ve been having a free lunch all of them explaining their own views … when it hasn’t mattered. It’s going to start mattering … A year ago, … [Yellen] was saying once they start raising rates they’d raise quickly. Now other members of the committee are starting to introduce that. They need to get on one page on the path“

Has the Fed failed? Fisher said:

- “The policy they’ve been pursuing is to pump up asset prices in the hope it generates consumer price inflation, and it hasn’t worked for five years“

Forget inflation. It hasn’t even worked well enough for the US economy for the Fed to raise rates by a lousy 25 bps after 9 long years. And in this Fed we are supposed to trust? Investors said no after the minutes on Wednesday and began liquidating their positions.

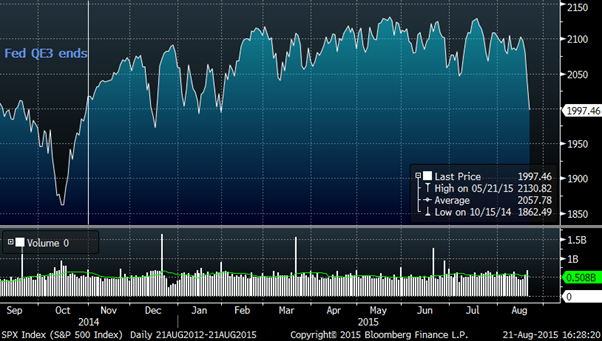

- Lena Komileva ?@komileva – S&P negative ytd, losing all post-Fed QE3 gains. Asset price deflation joins commodity deflation joins EM debubblin

So there goes the wealth effect, the goal of QE3. Far from being omnipotent & omniscient, the Fed has been thoroughly useless, right? If you think our disgust is even 10% valid, would you pay today’s multiple for the S&P?

Where is Jim Cramer with his rant? Is he waiting for 1820 print in the S&P that his CNBC colleagues Guy Adami & Steve Grasso discussed on Friday afternoon? His mind does seem to be in the right place even if his passion is absent. He made the same point on Thursday evening that Peter Fisher made on Friday morning.

- “We need those people to shut up so the Fed can speak with one voice. News flash to the Fed: Your job is bigger and way more important than the NFL, so get some discipline and rein it in, for heaven’s sake. Frankly, it’s an embarrassment to the institution“

Did it work? Of course not. Fed-head Bullard was back on Friday afternoon talking about the possibility of a September rate hike.

Did you hear that Jim? No body listens when you voice an opinion like a typical CNBC guest. You got to release your own inner Cramer to make a difference.

2. Chinese Mess

So much for the largest economy on the planet. What about the second largest? Jim Chanos was succinct on CNBC FM 1/2 on Friday:

- “It’s worse than you think. Whatever you might think, it’s worse; … People are beginning to realize the Chinese government is not omnipotent and omniscient,” he said. “In fact, like many of us, sometimes they don’t have a clue”

Peter Fisher spoke in more detail:

- “They have got an economy that is closing down; They have been used to be able to fix things for the past 25 years with more investment & that game is over; they have been talking a decade now about boosting consumption, reducing investment as a share of GDP, now they really have to get on with it …So I am not sure they are going to be able to save the rest of the emerging world from the challenge of the Chinese slowdown & commodity markets”

None of this was the worst news we heard about China this week. The worst was the news that Secretary of Treasury Jack Lew told a top Chinese official in a phone call on Friday that the United States would be closely monitoring China’s recent change in the way it allows the yuan to be traded. So we now warn China for a small devaluation of the Yuan band after our Fed has engaged in currency manipulation for the past five years?

And Japanese Finance Minister Taro Aso on Friday warned China “against frequent manipulation of yuan rates, saying that Tokyo would face a tough decision on how to respond to any such interventions from Beijing“. This from a country whose central bank has devalued its own currency by 35% against the Dollar.

It would be funny if it were not so scary. The world needs China to cut rates and get back on its feet if such a thing were possible.

Why do voice such skepticism? Partly because of our nature and partly because of an article on Friday in the South China Morning Post titled – Xi Jinping’s reforms encounter ‘unimaginably fierce resistance’, Chinese state media says in ‘furious’ commentary. The message of this article?

- “President Xi Jinping’s wide-ranging reform push, covering everything from politics to the military, has come up against “unimaginably” fierce resistance, according to a tersely worded commentary carried by state media on Thursday. … “The in-depth reform touches the basic issue of reconfiguring the lifeblood of this enormous economy and is aimed at making it healthier,” the article said. “The scale of the resistance is beyond what could have been imagined“

Xi Jinping is described by those who know him as one who “speaks like Deng and hits like Mao“. So when, how, and against whom does Xi hit?

But that is for the medium term. Next week depends on whether Shanghai market holds 3,500. Art Cashin reported on Friday morning that it took a great effort on the part of Chinese authorities to hold 3,500. If they are unable to hold 3,500, then it will reverberate through world markets, he said. Remember what Tom DeMark said a couple of week ago that “3,200 was a given“?

Do the Chinese still wish to live in interesting times?

3. US Stocks

It is very simple right now. US stocks are very oversold and the DSI of the S&P was as low as 3 on Friday. The put-call ratio was 190%, something that Helene Meisler said ” Not sure I have ever seen this“.

The simple and only question is whether this is a “good” oversold or a “bad” oversold condition. Meaning that a “good” oversold condition leads to a real bounce while a “bad” oversold condition doesn’t allow a real bounce. Much depends on overseas markets because

- Urban Carmel ?@ukarlewitz – 80% of the drop in the last 9 sessions came overnight. I think that gives you the narrative for what is primarily driving price lower

If we do bounce, what level do we bounce from and when? We already have seen a 10% decline in the Dow. We could see a 10% decline in the S&P to 1920 as CNBC FM guys speculated on Friday. A neat scenario would be to have a really bad Monday followed by another bad morning on Tuesday that reverses and closes green. We saw this speculation from Jeff Saut of Raymond James on Friday morning but we doubt whether he expected a 530 point fall in the Dow on Friday.

Tom McClellan got credit for calling this decline in the exact period that his forecast had specified. So what does he say about a potential bounce?

- “my expectation is for a relief rally which will set up for the more significant decline in September and beyond. We won’t get out of the downtrending phase until early April“

And what is the potential downdraft of this “significant” decline from September? McClellan writes:

- ” … notice that this latest drop in the COT data went from a high level down to around zero. That’s about half of the magnitude of the drop in this indicator ahead of both the 2000-02 and 2007-09 declines. That’s a really crude approximation, but half of either of those ugly bear markets would still be a big deal“

4. Dollar & Commodities

Gold was the star commodity this week. Was this mainly because of the 2% drop in the Dollar? Oil performed horribly. But if the Dollar stays down, will Oil finally have a rally? Dennis Gartman turned positive on Oil on Friday with a “small punt” but a “big change” in his psychology. Isn’t it called a “short” punt, Dennis? ACG Analytics recommended starting a position in USO on Friday. Will such a rally, if it happens, lead a rally in stocks?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter