Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Damn Damocles!

Last week, we wrote:

- “A rate rise on Friday would have eliminated any uncertainty and removed the Damocles sword of a December rate hike from hanging over our heads for the next 5 weeks. Remember, the biggest headache for all markets has been the will-they-won’t-they uncertainty.”

It is back on our heads again with Art Cashin saying on Friday “the Fed might have missed its window mightily” because of what he called “near deflationary free fall going on in commodities“. Cashin said in the same segment that “If they’re going to walk back from [raising rate], they’re not going to walk back this week, … They’re going to wait right to the very end unless markets seem to get really bruised and they step back a little bit earlier“.

This Fed is determined to “prepare” markets for their action before they take it. They haven’t yet realized that the markets prepare not just for their first action but their next action as well. The Fed wanted the markets to price in a rate hike in December. That the markets did but they didn’t stop there. Instead, as an article argued on Tuesday,

- “… already another rate hike is priced in six to nine months thereafter. Typically the market prices in expected news 6-9 months out. Therefore the current market price, according to CME figures, already has priced in, to some degree, two rate hikes from here.”

Those who doubt this should look at the carnage of this week – Oil down 8.5%, base metals in near deflationary free fall, and

- Ryan Detrick, CMT ?@RyanDetrick – Second worst week of the year. $SPY

The Fed may not understand how markets or people react. But shouldn’t they at least understand recursive loops? Whenever the Fed has signaled a forthcoming rate hike this year, the Dollar has risen, commodities have crashed, liquidity in high yield markets has disappeared, stocks have fallen leading the Fed to not tighten as promised. This, in turn, has resulted in Dollar weakening, commodities & commodity markets rallying, high yield market recovering and stocks rallying leading the Fed to signal a rate hike ahead which in turn has re-initiated the rise in the Dollar, commodity collapse and stock decline & so on.

This is why we felt it was incumbent for the Fed to tighten last Friday after a fantastic NFP number. Had they done so with a clear statement about no further rate hikes till March 2016, all uncertainty would have disappeared and the feared Fed hike would have been in the rear view mirror. Markets would have priced that much faster and much cheaper.

Instead, long live Damocles and his sword.

2.Bonds

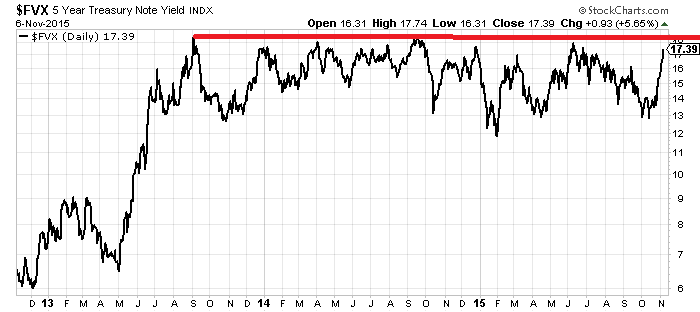

Last Friday it looked like yields were headed for a breakout. But one smart technician raised a significant question last Friday:

- Friday, November 6 – Helene Meisler @hmeisler – .@mark_dow is this 5 yr yield ever gonna get over 1.80% ???

The 5-year answered by declining by 7 bps this week. What about the longer end? Another smart technician made a very well-timed call this week:

- Wednesday – J.C. Parets ?@allstarcharts – LIVE on #Periscope: We’re live looking at why we are buying Treasury bonds down here and shorting stocks https://www.periscope.tv/w/aROmAjY4OTEwNHwxWXFHb01ZWE5MTnh2y6L83QNk_RxrqqZZ88BvdgZ-bvEFu_udpMKAxCyS4og= …

A day later, Parets published his call on yields:

- Thursday – J.C. Parets ?@allstarcharts NEW POST: Here is Why I Think Interest Rates Are Heading Lower http://allstarcharts.com/

heres-way-i-think-rates-are- heading-lower/ … $TLT $ZB_F $TNX $TYX

And the 30-5 year yield bull-steepened by 4 bps this week, a sign of a leak in the wall of certainty of a December Fed hike. The 2-year yield closed the week at 85 bps, a full 10 bps lower than the 95 bps level in the immediate aftermath of last Friday’s NFP number.

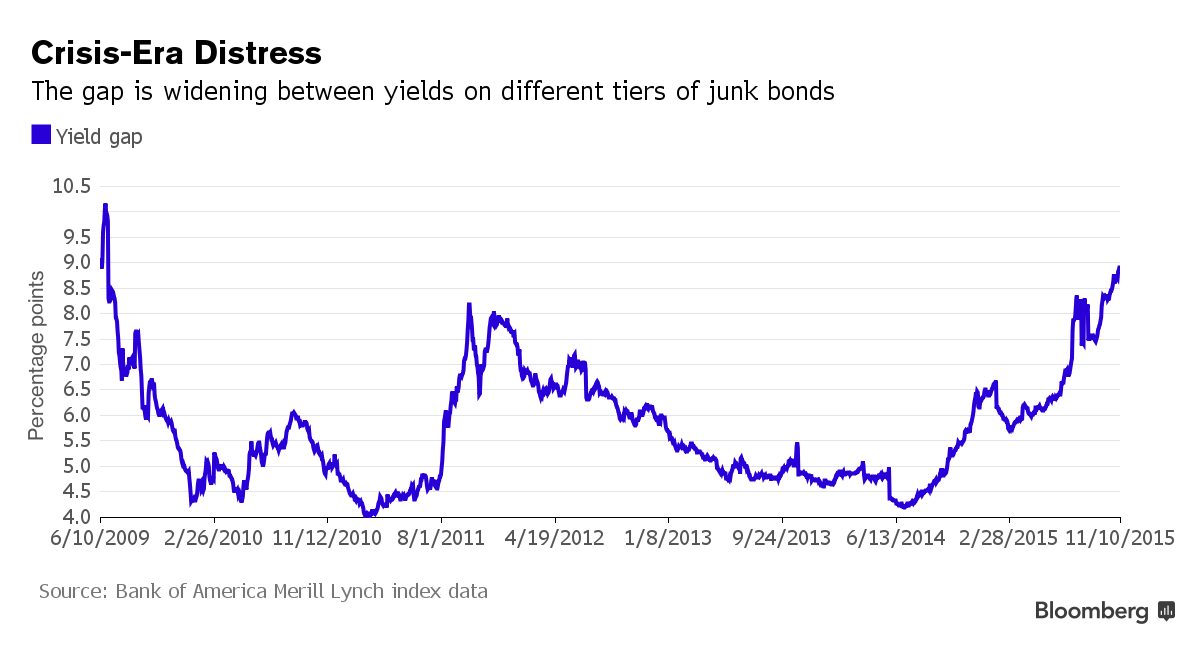

Not only did Treasuries rally but high yield ETFs underperformed TLT by 2% (HYG) & 2.5% (JNK).

- Lawrence McDonald ?@Convertbond – Warning Divergence – Market wide open to accept Investment Grade new bond sales but high yield issuance is taking a serious pause

And as a Bloomberg article stated:

- “Investors are largely shunning the riskiest U.S. corporate bonds, and those brave enough to tiptoe into the stuff are demanding the biggest premium relative to safer notes since the last financial crisis. The lowest-rated junk bonds are now yielding 14.7 percent on average, 8.9 percentage points more than the highest-rated speculative-grade debt.”

3.Stocks

Last week we featured several opinions that suggested a decline in the short term. These proved spot on. One such opinion was reiterated this week:

- Thursday – Ryan Detrick, CMT ?@RyanDetrick – This is amazing. Been talking about it for over a month now. Still playing out. $SPY

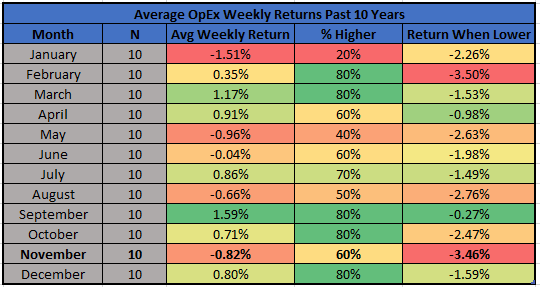

This chart and the record of November expirations suggest difficulties ahead:

- Ryan Detrick, CMT ?@RyanDetrick – Next week is November OpEx. Past 10 years, $SPX has been weak. Also, when it is lower, it is really lower. $SPY

The S&P broke below both the 200-day and the 100-day moving averages. It closed at 2024 which to some was an important level. Parets focused on another level:

- J.C. Parets ?@allstarcharts – I’ve said 2040 is a big level for the S&P500. If we’re below that, this is a big problem. I’m telling you….. $SPY $SPX $ES_F

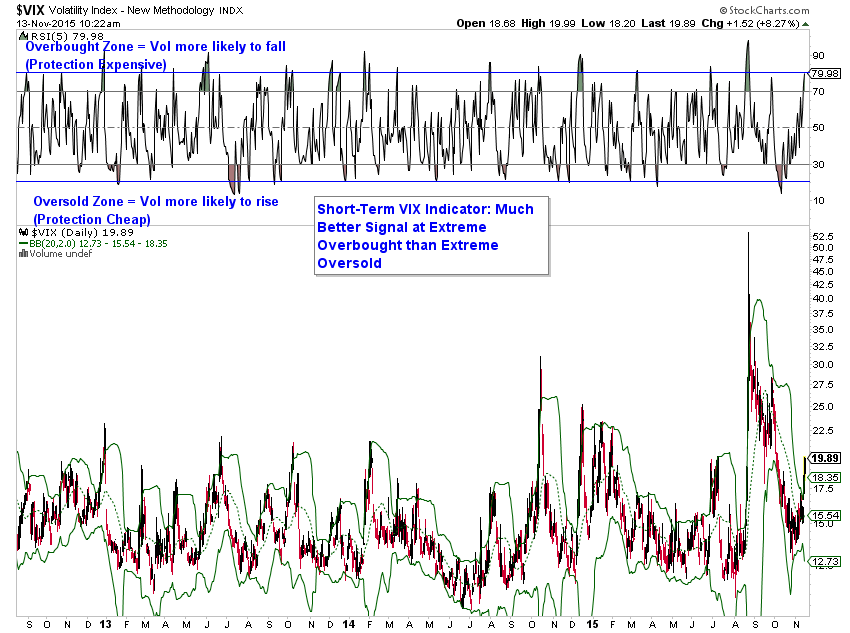

The stock market is either oversold or almost oversold depending on the oscillator used. But what about volatility & other indicators?

- Helene Meisler ?@hmeisler – Put/call ratio 122%, highest since 9/29. Nothing like price moves to change sentiment.

And,

- Charlie Bilello, CMT ?@MktOutperform – Volatility getting stretched (short-term), overbought, above upper bollinger band. $VIX

But markets that don’t rally when oversold get really ugly. And the horrific attacks in Paris may add velocity on Monday to this week’s decline.

4.Commodities

What happens to the U.S. Dollar? Does this week’s weaker data create a little headwind for the Dollar? Or does the uncertainty about the Paris attacks make the Dollar stronger?

Tom McClellan wrote about copper and the Dollar in his article on Thursday:

- “The 10 month cycle in copper price bottoms says that a bottom is due imminently. But we are not yet seeing a big negative reading on the ROC to say that we have seen a washout selloff. When that washout eventually comes, there will likely be some big geopolitical or economic news to justify the selloff, and to help facilitate the washout selling wave. So when you hear that the sky is falling in the copper market, that will be the signal that the bottom is almost at hand.”

McClellan also wonders “does that mean a real bottom for copper prices, or a top for the dollar? That is the interesting question, and I do not have an answer.”

What about Gold?

- Thursday – J.C. Parets ?@allstarcharts – there’s your reversal in Gold right near July lows. Nice candle today. We probably get a bounce, but a bounce I would still fade $GC_F $GLD

And in the same spirit,

- DK1 ?@canuck2usa – Mean Reversion in Commodities next Major play in my mind atm

Of course, all of this was pre-Paris attack. Will France & Europe use this to get militarily active in Syria? If they do, do they side with Putin and catch ISIS in a pincer? Or do they get into Syria against Assad and begin arming the “moderate” rebels a la Afghanistan? Oil was down 8.5% this week? Will it bounce next week on fears of escalation?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter