Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”Goldilocks” & “Mission Accomplished”

Friday’s NFP number came in at 164,000, leading some to use that old “term”:

- David Rosenberg – Friday – I detest the term “goldilocks” but readily admit that today’s employment report was neither too hot nor too cold

One un-rosy side from his own tweet:

- David Rosenberg @EconguyRosie – For the second month in a row, payrolls were below consensus. To make matters worse, the Birth-Death model flattered today’s headline by 45k, so the number was really closer to 120k.

On the rosier side:

- Urban Carmel @ukarlewitz – Most recent data: – Unemployment claims at new 45 yr low – 1Q18 GDP growth highest in 2-1/2 yrs – Housing starts +11%, sales +9% – Core CPI still 2% Net, a recession this year looks increasingly unlikely. New from The Fat Pitch https://fat-pitch.blogspot.com/2018/05/may-macro-update-recession-in-2018.html …

No recession this year sounds fine. But what about the aggressive Fed? See how one analyst interpreted the FOMC statement:

- Scott MinerdVerified account @ScottMinerd – The clear message of today’s FOMC statement is “Mission Accomplished.” Full employment and 2 pct inflation.

Wait a minute. Isn’t “Mission Accomplished” inherently dovish?

- Holger Zschaepitz @Schuldensuehner – Renaissance Macro’s Dutta on

#Fed: The only things of significance are addition of “symmetric” & taking out reference to monitoring inflation developments. This suggests they’re not overly worried about upside or downside risks to inflation in near term, so I think it’s dovish.

So the net message of the two big monetary events is no recession and a Fed that is not unduly worried? How is that not a bullish message?

What about corporations & their CEOs? We got one answer from PwC’s 21st annual survey of chief executive attitudes :

The article states:

- … we found that company leaders around the world were enthusiastically bullish about the global economy. … In general, business leaders’ expectations of accelerating economic growth are genuine, broad-based, and linked to global economic fundamentals.

OK then! But what about sentiment in the equity market?

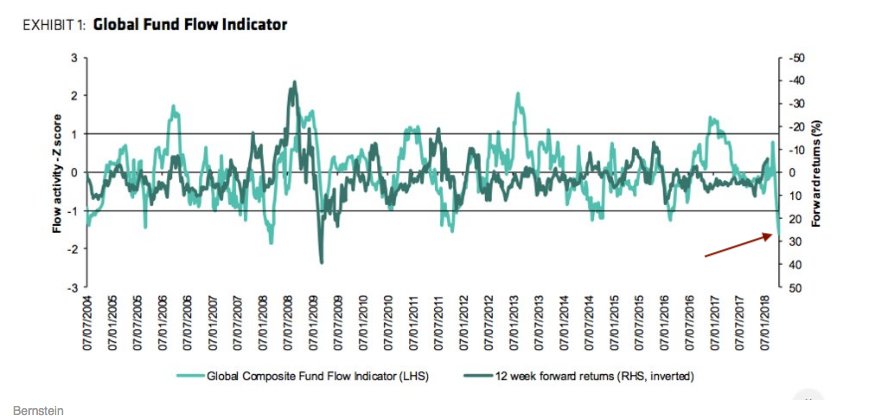

- Urban Carmel @ukarlewitz – Bernstein: fund flow indicator that monitors the pace of sentiment deterioration at 2nd most pessimistic level in 14 years

$SPX

How does Bernstein analyze this?

How does Bernstein analyze this?

Normally, we would scoff at this caution ourselves. But why do so when we can find a smart guru doing it for us?

- Tony Dwyer @dwyerstrategy – Fri – So let me get this right…

$SPX oper EPS look up 25% this qtr and 20% for year, yld curve is still positive, labor inflation is ok, profit margins are at new high, no recession in sight, the$SPX is down almost 10% from peak – and now is the time to get cautious? Not in our opin

The above are strategists & opinionators. Is there a technician investor who shed his caution and got bullish with real money?

2.”Kinetic Energy” & “Very big Resolution”

On Thursday when the SPX was at 2599, @toddgordontrade alerted his audience:

- ” … we are coming up on e-wave support level that must hold; we are at 2599; if we don’t hold (2580) that’s big trouble … “

Then something semi-magical happened:

We watched this turn in real time and, frankly, we were mega-impressed. It reminded us of the Friday morning of the week following 9/11. The week was all negative and so was that Friday morning when all of a sudden around 11-1130 am, the market turned. That was a big &, as it turned out, a momentous turn that came literally from nowhere. We have no idea whether the turn on Thursday May 3 at about 11:00 am will be sustained or not. But our simple minds & eyes were impressed.

We watched this turn in real time and, frankly, we were mega-impressed. It reminded us of the Friday morning of the week following 9/11. The week was all negative and so was that Friday morning when all of a sudden around 11-1130 am, the market turned. That was a big &, as it turned out, a momentous turn that came literally from nowhere. We have no idea whether the turn on Thursday May 3 at about 11:00 am will be sustained or not. But our simple minds & eyes were impressed.

Todd Gordon concurred and he called it a turn on CNBC Fast Money on Thursday afternoon. Kudos to him for very quickly turning from a highly worried bear to a bull on that turn. Watch & listen to him explain in the first 52 seconds of the clip below:

- “Simple triangle – lower highs & higher lows – at some point all this potential energy that has been stored up in this market will be released & go into kinetic energy;”

- “tried for 3rd time to break the 200-day & snapped back; I think that’s the buy signal … we got a cool little candle ; that’s going to be the reversal signal“

Then came Friday with its dovish payroll number and stocks, after an initial decline, reversed & did not look back until the close. The Dow closed on Friday approx 700 points higher from the reversal signal identified by Todd Gordon.

Remember the eyes of the beholder proverb? Carter Worth, the resident technician at CNBC Fast Money (pm edition) looked at the same triangle and predicted that the S&P would break down instead of breaking up from the triangle. His reasoning is that so many stocks have broken down that the presumption is the S&P will also breakdown. However in keeping of Gordon’s “kinetic energy” description, Worth said there will be a “very big resolution out of this“.

Another technician, Mark Newton, took the middle on CNBC Closing Bell on Thursday & said he expects more selling next week but added “we are getting close to a level where we are going to put in a low” from which the market can rally into fall. Technology is still leadership he said, but not Semis.

Who is left to opine? We have heard here from strategists & technicians. What about a Quant guru who has been right before? Let us fix that by listening to Marko Kolanovic of JP Morgan:

Actually Marko made 5 points:

- Market bottom is in at 2532, intra-day low of February 9.

- Market volatility will subside; we will see VIX at 13-14 later in the year

- equity positioning has declined, especially in systematic managers;

- valuations have improved with forward PE below 16 whereas historical forward PE is 16.9

- He thinks the S&P can reclaim the old high & go above that to 2900-2950-3000 – global growth remains strong and earnings are very strong

Amazingly, this view of a rally to new highs later this year is shared by a strategist who actually said on this past Monday that the bull market is coming to an end:

First the immediate:

- “We are very bullish right here – 2625-2650 – we think it is actually a good entry point for a move towards higher highs; we think there are higher highs ahead this year – that’s a pretty good return.”

So what about the end of the bull market?

- “Valuation peak was December 2017; Sentiment & Positioning peak was January; now we are waiting for a price peak; we see a beginning of a topping process; it can last awhile; its a much different environment than last year obviously”

Of course, if Carter Worth proves correct and the big resolution of the S&P triangle is to the downside, then all the above bets are off.

Getting back to Mike Wilson, allow us to wonder whether his last statement will remain true. Last year became last year because of President Trump’s victory in November 2016. Last year ended as last year with a valuation peak because of the Tax Cut. Right now, many if not most believe that the Republicans will suffer in midterm elections in November 2018. But what if the Republicans keep both the Senate & the House and win big in November 2018?

Look at the big story of Friday – the scathing criticism by the Federal Judge of Special Counsel Mueller and his “overreach” of indicting Paul Manafort for the purpose of getting Trump. Last week, Chuck Todd, host of NBC’s Meet the Press, talked in his round table about how the American people see the Stormy Daniels case as so far from “Russia Collusion”. He wondered whether they would rebel against do anything to “get Trump” movement. Then you have the doubling of President Trump’s poll numbers among African-Americans after the Kanye West story. And the Trump base is thrilled that he has delivered what he promised.

Each one of these may not be much alone but the combined effect could be quite substantial. Anecdotally we can report a cousin sister, who had never heard of Sean Hannity 3 years ago, now says she looks forward to watching Hannity’s show every week day.

So what if President Trump campaigns aggressively promising an infrastructure bill & a prescription drug cost bill after the election and asks voters to vote in Republicans to achieve that?

Would the country, the economy & the stock market get another jolt of confidence if Republicans win & increase their majority in both the Senate & the House? In that case, would we see higher peaks in valuation, sentiment? Possibly. That is why we are not willing to pretend to know how the economy & the country would look & feel after November 2018.

3. Interest Rates

Unlike stocks, there is very little to say about rates which essentially did nothing week/week. The 2-year yield rose by 2 bps to 2.50% and the 30-year yield fell by 1.2 bps to 3.116%. The 10-year at 2.946% remained resolutely in range. This is despite two dovish triggers of the Fed & the NFP number. This led Rick Santelli to term the 2018 Treasury market as similar to 2017 stock market – nothing fazes it.

4. Dollar, Sector & One Emerging Market

A bigger story is the U.S. Dollar. It rallied 1.3% on the week after a 1.4% rally last week. So far the two dovish triggers of the Fed & the NFP number have not done much to stop the rally. But what if the Dollar doesn’t get much stronger and the 10-year stays peaceful?

Jim Cramer discussed this on his 9:00 am show this week and suggested that the consumer staples sector could rally from its severely beaten-down state. Then, on Friday, Carter Worth made a forceful case for a rally in Consumer Staples, mainly because of their severely oversold condition.

An emerging market that can benefit from both peaceful 10-year Treasury & a stable Dollar is India. This week, J.C. Parets made the case for Indian stocks in his article Here’s What Fuels India’s Next Leg Higher. A quick summary is:

- “In India we’re seeing failed head and shoulders topping patterns across the major indices which have helped to wash out longs, frustrate shorts, and lead to higher prices by forcing buyers back into the market. Within the asset class the IT, Fast Moving Consumer Goods, and Energy sectors are showing relative strength and are the areas we want to be looking at on the long side. We have our levels for risk management in case we’re wrong, but for now the weight of the evidence suggests stock prices in India (and globally) are headed higher.”

5. Commodities

The big beneficiaries of a dovish Fed & a dovish NFP number were materials. If global growth remains strong, interest rates stay peaceful and Dollar doesn’t move much higher, then commodities should do well.

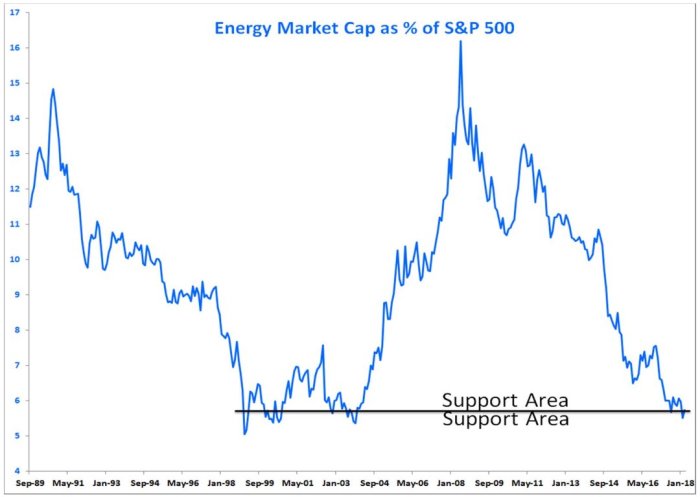

Mike Wilson of Morgan Stanley said, in his clip above, that energy is by far their #1 sector. The chart below could, in itself, drive its outperformance:

- Babak @TN– – the Energy sector, in contrast, is at a historic low weight ~5.5%, comparable to late 1990’s

$XLE

Since May 12, the deadline for the Iran deal recertification, is almost upon us, :

- Holger Zschaepitz @Schuldensuehner – WTI

#oil nearing $70 with traders on edge ahead of#Iran deal decision. Sanctions on#Iran may lead to disruption of oil exports. https://www.bloomberg.com/news/articles/2018-05-04/oil-set-for-weekly-gain-as-market-waits-for-trump-s-iran-action …

Week after week, Gold does nothing but we keep seeing smart people promising a big rally ahead:

- Jesse Felder @jessefelder – The ratio of gold prices versus silver prices is now up to the type of high reading that in the past 2 decades has marked an important low for both gold and silver prices. http://www.mcoscillator.com/learning_center/weekly_chart/gold_silver_ratio/#When:17:17:42Z … by

@McClellanOsc

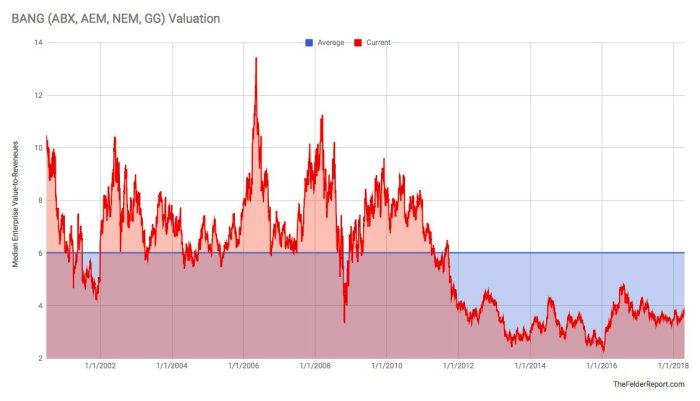

Now a seemingly outlandish claim about gold miners:

Now a seemingly outlandish claim about gold miners:

- Jesse Felder @jessefelder – BANG: Why The Gold Miners Could Soon Make FANG Look Tame https://thefelderreport.com/20

18/05/03/bang-why-the-gold-min ers-could-soon-make-fang-look- tame/ …

6. Cinco de Mayo

6. Cinco de Mayo

This is the day of Cinco de Mayo, a historical national holiday in & of Mexico. We will not touch the historical or cultural part lest we get accused of cultural appropriation. But we love two Mexican items, margaritas and mole poblano, the amazing sauce called by some as the national dish of Mexico. A cuisine that combines chocolate with chili peppers is brilliantly innovative indeed.

We wait for a day when Bollywood brings out a light celebratory movie about Mexico. Since we don’t have one yet, we decided to present an Indo-Spanish song about desire & love being a universal language that speaks with eyes. The clip provides English subtitles of both Spanish & Hindi lyrics.

[embedyt] http://www.youtube.com/watch?v=C2Xu6FkgPtQ[/embedyt]

Instead of throwing a traditional bachelor party for their friend, two guys decide to take him on a trip through Spain. The plan is to let go of their inhibitions and do what they normally would not do. In the clip above, they see 3 Spanish women performing a dance in a town center. The guys don’t know a word of Spanish. But they jump on the stage and begin singing in Hindi. The Spanish dancers don’t know the words but they see the look in the eyes of the men and begin dancing with them. The message is about how desire enriches life.

The title of the film is Zindahi Na Mile Dobara – You can’t get life twice – meaning enjoy your life now because you won’t get that chance again. This is a modern fresh light urban film about successful professionals and about how their views of life change in this trip through Spain. We recommend it to all.

The easiest way to watch it is on Amazon Prime Videos. By the way, Indian tourism to Spain exploded after this film was released, a reason more & more cities are trying to entice Bollywood to shoot films in their scenic locales.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter