Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.The Question

Last week our question was,

- “Wouldn’t it be interesting to see a decline sometime next week just to scare some chasers? A weekly close in VIX below 13 is just the right sort of trigger for that and it is quite common to see one hard down day during Options Expiration week.”

We did get the one hard down day on Tuesday, down 270 points to close down 193 points. After a small rally on Wednesday, we got another down day on Thursday, this time triggered mainly by some negative comments attributed to President Trump about China trade discussion. This decline of 129 points was reduced in the afternoon to close down 55 points. Did these declines scare some chasers? $VIX did close up 5.7% on the week thus alleviating some of the low $VIX situation of prior week.

The big indices, Dow Jones, SPX, Nasdaq, closed down on the week while Russell 2000 went to new highs three straight days to close the week. This divergence leads to the critical question:

- The Chartist @thechartist – “so here’s the question: are the all-time highs in Small-caps and Micro-caps

$IWM$IWC a historic epic failed breakout and the entire market rolls over from here? Or is it evidence of risk appetite for equities and large caps will be next$QQQ$SPX$DJIA” via@allstarcharts

If large caps are next, then wouldn’t SPY/IWM underperformance decline?

- Thomas Thornton @TommyThornton – Thu – One thing we noticed in Feb was

$SPY vs$IWM ratio upside DeMark exhaustion signals but tomorrow there will be a downside signal. Now a limiting factor for continued upside in Russell

Even bullish gurus exhibit misgivings.

- Peter BrandtVerified account @PeterLBrandt – While I remain constructive on U.S. equities, particularly the Russell 2000, I cannot ignore the potential sell signal in

$SPX$ES_F$SPY under 2700

Others are waiting for a decisive breakout above 2750:

Others are waiting for a decisive breakout above 2750:

- Lawrence G. McMillan @optstrategist – The Option Strategist Weekly Updater 5/18/2018 – https://mailchi.mp/optionstrategist/the-option-strategist-weekly-updater-2619029 … “In summary, the indicators have all turned bullish, and $SPX has made a positive trend move by closing above the April highs and by breaking through the downtrend line. This is about as close to a fully bullish signal as one can get, but we have seen this market reverse downward suddenly several times in the last few months, so we are not going to change our intermediate-term outlook unless that gap at 2750 is closed.”

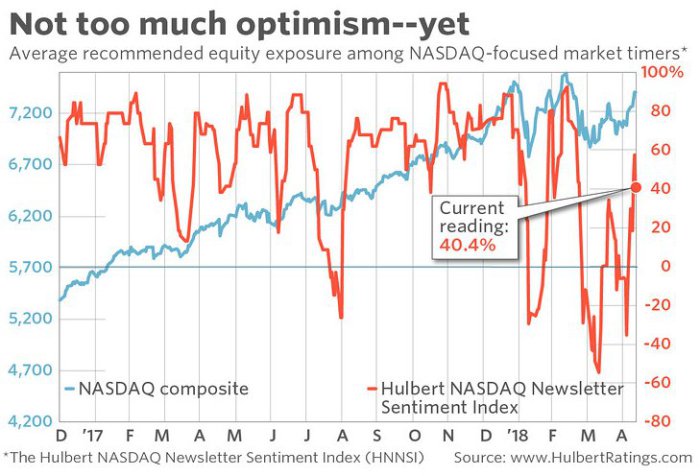

What about sentiment?

- Babak @TN Hulbert Nasdaq Newsletter

#Sentiment Index at 40.4% suggests that traders are reluctant to jump back on this rally, which is#contrarian positive for the primary trend to reassert itself https://www.marketwatch.com/story/heres-how-youll-know-when-this-bull-market-is-just-about-done-2018-05-15 …

Sentiment is helpful but isn’t bullish action in Credit necessary for an equity rally?

- Mark Newton @MarkNewtonCMT – High Yield CDX gradually bottoming out – Demark TD 13 Combo buys on Markit CDX right at lows 1/26 when Equity market peaked.. Momentum gradually lifting

@VictorZubarev

But what about that other serious divergence in global equities?

But what about that other serious divergence in global equities?

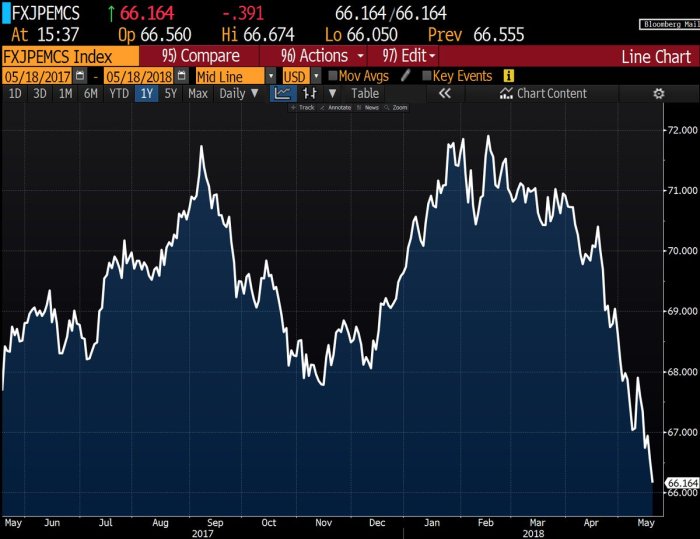

2. Emerging Markets

Since their peak in January, Emerging Market assets have literally plunged.

- Jeroen bloklandVerified account @jsblokland – EM FX continue their decline against the

#USD. Now down 8% since Mid February!

If EM currencies are in this state, what is the state of Emerging Markets local currency bonds?

If EM currencies are in this state, what is the state of Emerging Markets local currency bonds?

- Lisa AbramowiczVerified account @lisaabramowicz1 – The biggest local-currency emerging-markets ETF has lost nearly 20% of its assets since the beginning of April, dropping to $6.5 billion from $7.9 billion.

@TheTerminal$IEML

Guess what has happened to EM equities since January highs? EEM is down over 11% and EWZ is down almost 20% since January 5. It was down 6.5% this week alone. But are things so bad that they are beginning to look good?

Guess what has happened to EM equities since January highs? EEM is down over 11% and EWZ is down almost 20% since January 5. It was down 6.5% this week alone. But are things so bad that they are beginning to look good?

- Thomas Thornton @TommyThornton –

$EWZ Brazil achieved wave 3 downside price objective we have been expecting since February.

But what fundamental reason can any one provide for a bounce in Brazil? Larry McDonald of Bear Traps Report provided one on CNBC:

But what fundamental reason can any one provide for a bounce in Brazil? Larry McDonald of Bear Traps Report provided one on CNBC:

- “With bond yields moving higher, there are a lot of losses around the country, around the world in bonds. Those assets have to move somewhere and they’re moving into commodities, commodity-producing countries, … About 30 percent of Brazil’s GDP is related to the commodity space, so from an economic standpoint, that’s a very big positive.”

Larry McDonald went negative on EM in January 2018. He proved spectacularly right then. We will see if his current bullishness on Brazil proves right.

But what about the main reason for this decline in EM assets? Dr. Carmen Reinhart, Harvard professor & co-author of Ken Rogoff, argued the following to justify her assertion that emerging markets are worse off now than during their two most recent moments of weakness: The 2008 global financial crisis and 2013 taper tantrum.

- “It’s what it implies for the reaction of U.S. monetary policy. The bigger the tightening, the more the anticipation that rates will go higher and higher and that has multiplier consequences for emerging markets. … ”

In other words, US interest rates are a very big factor. And we all know what they did this week – the US 10-year has decisively crossed the 3.03% level and the 30-year yield closed above the critical 3.22% level.

3. US Treasury Rates

Was Thursday’s close of the 30-year Treasury above 3.22% a sell signal for interest rates? Not yet, tweeted Jeffrey Gundlach, the man who set 3.22% as the all-important level that could signal the end of the multi-decade bull market in bonds.

- Jeffrey GundlachVerified account @TruthGundlach – The day’s not over, but looking like 30 yr UST is not going to give the “2 consecutive closes above 3.22%” sell signal…not today, anyway.

The action in Treasuries impressed some:

- Blake MorrowVerified account @PipCzar – Bond bears better take a look at some of those reversal candles today.

Friday’s move in the 30-year yield was impressive indeed. From 3.24%+ in the morning, it fell all day to close to just above 3.20%. The 30-year yield had risen by 12 bps on the week & the speculator short position is so large that some profit taking might have made sense to shorts on Friday. So the fall away from 3.23-3.24% might simply have been due to reduction of short risk over the weekend.

The shorts could easily come back on Monday if rates start rising after the weekend. But the existence of such a huge short position could itself act as a speed breaker on the up move in rates. So argued Jim Caron of Morgan Stanley to Rick Santelli:

Also seasonality could start playing a helpful role:

- Movement Capital @movement_cap – May has historically been the start of a seasonally positive period in the 30yr treasury bond https://commodityseasonality.com/financials/

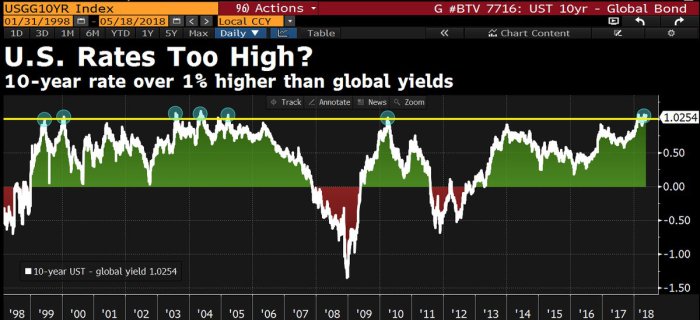

There is also a limit for divergence between rates in USA & the rest of the developed world:

- Lisa AbramowiczVerified account @lisaabramowicz1 – U.S. 10-year yields are more than 1 percentage point higher than global yields, a level that typically can’t last too long.

@queenofchartz

But until & unless the above materialize, the following stance seems popular:

But until & unless the above materialize, the following stance seems popular:

- Mark Newton @MarkNewtonCMT – Yes, BONDS were more important than STOCKS this week, & yields ratcheting up around the globe is something to pay attention to, given breakouts of long-term trends- I am a Treasury Seller on today’s TY strength/yield weakness, & like

$TBT$DRV$TYO

4. Energy

The move in Crude Oil & Energy stocks has been spectacular. But has it been so good that it is almost bad now?

- Thomas Thornton @TommyThornton – For the last few days Hedge Fund Telemetry Daily Note has been saying to start selling down Energy long exposure with upside DeMark exhaustion signals and other OB indicators. We liked them long from 4/2

$OIH$XLE$XOP@TruthGundlach

Other strong sectors like miners sold off badly on Friday. Was that just normal profit taking on a Friday or was that similar to the above sell energy recommendation?

Other strong sectors like miners sold off badly on Friday. Was that just normal profit taking on a Friday or was that similar to the above sell energy recommendation?

We will find out next week.

5. Gold

Frankly, we are fed up of Gold. Every strength has been viciously sold & every guru who has recommended buying Gold & Silver has been wrong, at least so far. Instead of breaking to 1,400 & above, Gold broke below 1,300 this week. How can Gold rally when the Dollar keeps rising and interest rates keep rising?

So we are not going to comment on Gold until the Dollar starts declining again and/or rates start falling decisively.

6. Google vs. Matrimony.com

First Facebook vs. Match.com and now Google vs. Matrimony.com. The first is simple competition. But the second “requires Google to change the way it conducts business in India on a lasting basis and the way it designs its search results page in India” and Google could be “irreparably harmed” according to a filing by Google. An article in the Hindustan Times states:

- The Competition Commission of India (CCI) in February fined Google $20 million for abusing its position in online web search and also slammed the company for preventing its partners from using competing search services. Google last month obtained a partial stay on the ruling from India’s company law tribunal, which allowed it to deposit only a small part of the imposed penalty.

- But Matrimony.com – which first brought the case in 2012 – has also appealed against the CCI ruling as it believes Google has gotten off too lightly.

- The appeal will be heard on May 28.

The social media companies will increasingly come under regulatory scrutiny in India both because Indian Regulators are getting more sophisticated and because they are also aware that India is now paramount for Facebook, Google & Twitter. Virtually every one we know uses Gmail and WhatsApp has over 200 million users in India. These market shares are expected to explode as India implements 4G nationwide.

And they face an uphill battle in America as well. 60 Minutes is scheduled to do a segment on Google. We would bet it would be quite negative for Google. Any takers for that bet?

7. Longer Term Views

May be the discussion above about rates falling or at least slowing their ascent can find support if David Rosenberg proves correct in his Thursday comment – “We are seeing the global economy beginning to cool off , as the synchronized growth story begins to fade“.

A less rosy outlook from him below:

- David Rosenberg @EconguyRosie – Fed hiking rates. Bond yields popping. Oil prices soaring. Think 1973-75. Think 1979-80. Think 1989-90. Think 1999-2000. And think 2006-07. And tell me a recession isn’t coming our way.

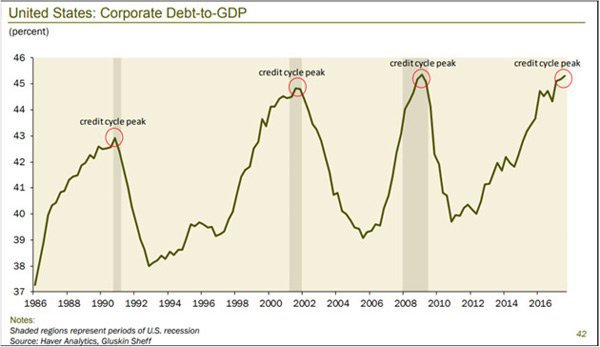

Even less rosy is:

- Dave Collum @DavidBCollum – Seems a little sketchy to me. Maybe I am just old fashioned and didn’t get the memo that debt no longer matters….

The above should lead you to both the S & R words:

The above should lead you to both the S & R words:

- Jim Rickards @JamesGRickards – I’m filing this volcano photo under, “Act like nothing’s wrong.” Sort of portrays how central bankers are ignoring the build-up of systemic risk.

Let us now go to something bright, orange & delightful, something that you should get almost immediately after reading this article. It is virtually guaranteed to put you in a great mood:

8. Let You Eat Cake

Not any cake, but the one below from Amazon Whole Foods.

Yes, our preference for cakes has so far been limited to Chocolate Mousse, Chocolate Ganache & other forms of Chocolate Cakes.

A couple of weeks ago, a very nice lady at Whole Foods asked us to try the above Mango Mousse cake. We did and became very happy. This is a seasonal delicacy, according to her. So rush to your Whole Foods to try it.

We are not the type to forsake our old love because something equally lovely comes along. So now we buy both the Chocolate Mousse Cake and the Mango Mousse Cake when we visit Whole Foods. And why not? We are simply doing what Marie Antoinette asked us simple folks to do.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter