Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Event Risks

This is one week in which we will dispense with charts, technicals & stuff. That is because we see event risks all over the place. We don’t mean dumb stuff like the NYT Op-Ed or even the Woodword book. We mean real events including, of course, threats of additional sanctions as we saw on Friday afternoon.

So our approach this week is to highlight C (clips) within TACs instead of T (tweets), clips that actually try to shed some light on the event risks.

2. FOMC vs. Stagflation or Slowdown

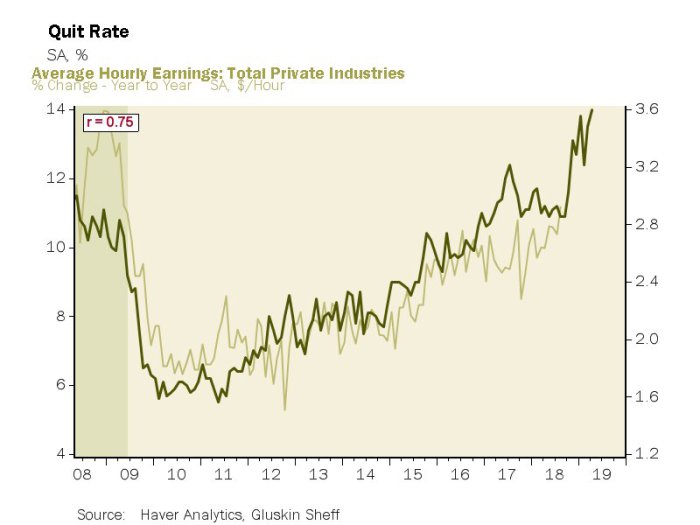

The yr/yr wage growth of 2.9% in Friday’s NFP report hit the Treasury market very hard. The Treasury curve rose in a parallel upward shift in yields by 5-7 bps on Friday. The 30-year yield only rose 5 bps vs. the 5-year yield which rose 7 bps. So instead of the 9-year high in wage growth steepening the yield curve, it flattened it by 2 bps. Is that a clear warning from the Treasury market that a couple more rate hikes will invert the yield curve?

So the first & actionable event risk is whether the FOMC admits they are behind the inflation curve & speak hawkishly on September 26 or whether Chairman Powell doesn’t see a big risk & reinvokes Greenspan’s reluctance to raise rates in 1990s.

David Rosenberg is clearly on the former side:

- David Rosenberg @EconguyRosie – Wage growth accelerates to a nine-year high but the clue for more pick-up comes from the quit rate — it soared to an 18-year high. Fed ain’t done.

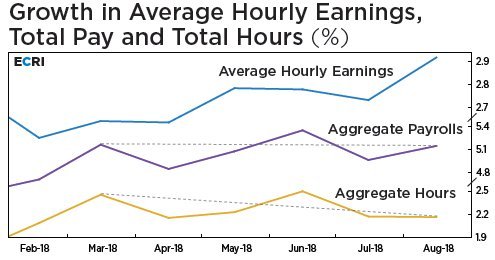

But Rosenberg also saw some weak internals in the NFP report. Lakshman Achuthan of ECRI went farther with his ongoing global industrial slowdown thesis. He also has a simple explanation for the rise in Average Hourly Earnings (AHE):

- Lakshman AchuthanVerified account @businesscycle – It’s not that complicated: since Mar ’18, growth in total pay is flat but growth in total hours – which reflects economic growth – is down. THIS is the arithmetic behind rise in AHE growth, and is in line with our earlier slowdown call. https://goo.gl/cXLRtd

Achuthan was as clear as Rosenberg about what Fed should do, but in the opposite direction – “I don’t like the idea of tightening into a slowdown”.

So if Chairman Powell concurs with Mr. Achuthan, then risk assets may not be hurt badly. But if he concurs with Mr. Rosenberg & acts on that, risk assets could be hit hard. This is probably the biggest event risk for September-October.

2. China-US

Ian Bremmer runs a consultancy organization and such head honchos rarely run ahead of their clients. That is why Mr. Bremmer doesn’t usually speak with high clarity, especially unpleasant clarity. One exception is the clip below with Francine Lacqua of BTV.

He states categorically that China is Enemy No. 1 and the Mexico deal was important for President Trump to demonstrate to his voters that being tough on trade gets results. So he says succinctly in the first couple of minutes – “nothing before mid-terms; all you are going to see are escalations in terms of announcements of additional sanctions“. That is another event risk, a more headline type of event risk actually.

Then in his second act from minute 5:40 onwards, Mr. Bremmer explains how President Xi is recalibrating his approach and acting more flexibly towards USA. He has agreed to buy less oil from Iran and that “takes off 1 million barrels out of Iranian production“. He cancelled a historic summit in Pyongyang with Kim Jong un and sent his number three guy there instead. The messaging is “they don’t want a smackdown war with the US“.

What Ms. Lacqua did not ask and what Mr. Bremmer did not address is the simple question – Will President Trump put into effect his previously announced tariffs on $200B of Chinese goods &, if so, how will China react?

Guess we will all find out next week.

3. Emerging Markets

A moderately warm outlook was presented by Ruchir Sharma of Morgan Stanley Investment Management this week on CNBC Closing Bell. He pointed out that half the increase in global debt of the past 10 years was from China. So it all comes down to China. Putting it another positive way, Mr. Sharma said for the EM markets to suffer a second leg down, something bad has to happen in China. He added that we are coming pretty close to a once in a lifetime buying opportunity in EM like the 10-year up cycle in EM post the 1998 crash in EM. But as we remember vividly, that up move did not begin till Chairman Greenspan eased twice in October-November 1998.

A different viewpoint was presented by Mark Chandler & Lakshman Achuthan on BTV Surveillance. Mr. Achuthan said there is a global industrial slowdown going on and EM, with its hyper exposure to global industrial growth, is right in the eye of that. That is why while valuation may seem like it is cheap but it is not there yet.

This will be a risk to US market because “at some point over there comes back here“.

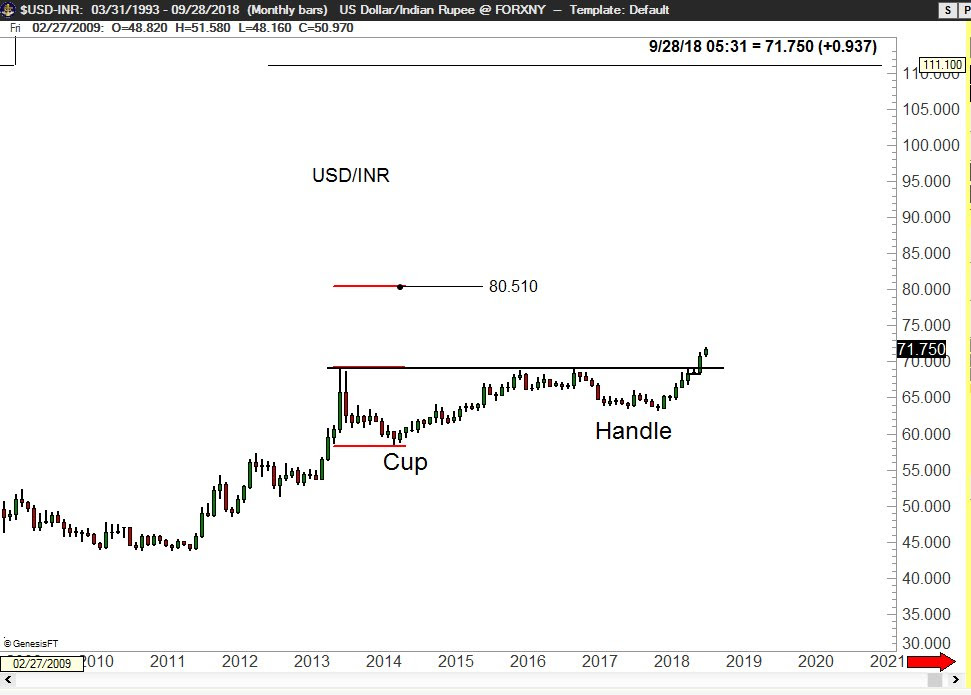

Well, talking about EM risk, the Indian Rupee broke above 71 Rs vs. Dollar this week. And what target does that suggest?

- Peter BrandtVerified account @PeterLBrandt – The multi-year Cup and Handle pattern in $USDINR sets a target for the Rupee of 80.51.

Isn’t there some sort of tenet that an asset class does not bottom until the strongest or most resilient sector of that class finally falls? If there is such, then perhaps EM may not bottom until the Indian stock market gets hit hard with the Rupee.

Isn’t there some sort of tenet that an asset class does not bottom until the strongest or most resilient sector of that class finally falls? If there is such, then perhaps EM may not bottom until the Indian stock market gets hit hard with the Rupee.

We are not hoping for it, just saying.

4. “A Slowly Ticking Time Bomb“

Fortunately, we don’t have any material updates on the Italy-EU event risk we discussed last week, except of course what is reflected in the German DAX, besides the negative reality & forecasts of global trade:

- Peter BrandtVerified account @PeterLBrandt – Chart of the day. For those who care,

$DAX$GX_F is possibly completing a 15-wk descending triangle that would be the right shoulder of a massive H&S top. This would be known at the Merkel Fiasco trade.

Neither Italy nor EU-Germany is anything akin to a slowly ticking time bomb. That is the event risk we discussed last in our article of last week. It is Idlib, the province of Syria near Turkey, about which all powers want to make a deal & throw out HTS, the Al Qaida affiliate. But they can’t make a deal and that is why the French envoy, Francois Delattre, called Idlib “a slowly ticking time bomb” this week. He added,

- “Few disasters have been so clearly anticipated and have been subject to so many convergent warnings by the international community. ”

Weren’t these sorts of words used in 1914 before the actual First World War broke out? So what is the problem? From what we understand, Russia would resist pressures from Iran & Assad if Putin gets convinced he could pull Turkey out of the Western alliance & America. But he thinks he cannot, then Russia will choose to side with Assad & Iran against Turkey. Russia is already conducting bombing raids in Idlib against HTS.

Apparently, the meeting in Tehran between Russia, Turkey & Iran featured a shouting match between Putin & Erdogan. On the other hand, America, UK & France are united in their absolute opposition to Assad cleaning up HTS in Idlib because of the hell that would create for civilians.

So if Syrian troops go into Idlib in strength, does Turkey act against Russian air force? Do either Assad or HTS detonate a chemical device that forces President Trump to retaliate against Assad? What does Russia do in that case? Clearly Iran would like nothing better than to provoke a skirmish between Russia & US.

Frankly, America doesn’t care much about Idlib but America’s major objective is to get Iranian forces out of Syria. So does US act against Hezbollah inside Syria or against Iranian forces inside Syria?

Notice something weird & bad happened in Basra, the Shitte portion of Iraq located near the Iranian border. Iraqi protestors burned down sections of the Iranian consulate in Basra shouting death to Iran. This is weird because Shiite Basra was among the most pro-Iran areas even during the 8-year Iraq-Iran war under Saddam. Also weird because Iraqi dinar seems far more steady than Iran’s Rial:

- ((The Daily Shot))) @SoberLook Chart: Iran’s rial collapsing in the black market –

So you would think Iranians would be protesting & burning down Iraqi consulate & not vice versa. Of course, we know that the Trump Administration is committed to punishing the Iranian regime which typically tends to double down under pressure.

So you would think Iranians would be protesting & burning down Iraqi consulate & not vice versa. Of course, we know that the Trump Administration is committed to punishing the Iranian regime which typically tends to double down under pressure.

(Courtesy – NYT – Nabil Al-Jurani/Associated Press)

(Courtesy – NYT – Nabil Al-Jurani/Associated Press)

Of course, we all know what asset class would benefit if Idlib creates a real event. As it happens, Carter Worth recommended buying oil stocks on Friday:

5. Sentiment & Irony

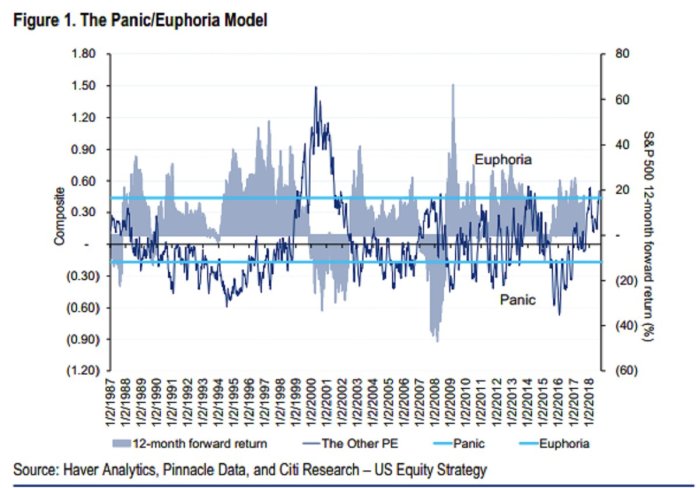

- Babak @TN Citi’s Panic / Euphoria Model is also flashing a warning as it once again reaches “euphoria” levels similar to Jan 2018

#sentiment

What does this mean in plain talk?

- Citi’s panic/euphoria model, tracking everything from margin debt to options trading and newsletter bullishness, just showed sentiment climbed to extreme levels for the first time since January. Such readings have preceded equity losses over the following 12 months 70 percent of the time since 1987, more than three times the random probability.

After all of the above, wouldn’t it be ironic if China doesn’t retaliate and we see a rally come Monday morning that lasts into Options Expiration next Friday? After all, events not resulting in a risk is also a type of Event Risk, right?

6. Mother protecting her kids

So beautifully captured in the photo below:

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter