Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Kudos & Thanks

After a week like this, it is entirely appropriate to say kudos & thank those who alerted all of us & protected capital of investors. Remember what David Kotok of Cumberland Advisors wrote in the first week of August in the article article titled Why the Yield Curve is Flat & Why It May Steepen :

- By using Treasury strips … you can lock up the funding of your long-term pension liabilities. When you do, your creditworthiness according to rating agencies goes up, and your funding ratio is more secure.

- Put this all together and there are huge incentives for certain companies to buy US Treasury strips, and those companies have been doing so in increasing amounts.

- Barclays reports that US Treasury stripping activity has accelerated. Here are numbers from the US Treasury. (We present them in first-half-of-year increments so there is no seasonality distortion.) H1 2015 stripping was $1 billion; H1 2016 was $6 billion; H1 2017 was $14 billion; and H1 2018 was $26 billion. Note that the US Treasury auctions about $14 billion of 30-year bonds each month. So in the first half of this 2018 year the equivalent of about 1/3 of the newly created long bonds were stripped. For the corresponding period in the previous year that was about 1/6.

The article also warned that this incentive to buy strips will expire on September 15. This article on August 11, 2018 should have alerted longs in Treasuries to watch out for waning of demand after September 15. Add to this the 3 different warnings issued by Greg Harmon of DragonFly Capital about TLT & Treasuries.

Any one who read & followed these warnings avoided this week’s collapse in Treasuries. So kudos to David Kotok & Greg Harmon. Kudos also to @TommyThornton for warning investors about small caps:

- Thomas Thornton@TommyThorntonMore –

$IWM I recall a few people thought it was funny how DeMark upside exhaustion signal on Russell wouldn’t work. Whatever, I just keep my head down and stay focused.

2. Bull in China Shop

Two factors created the explosion in Treasury yields that shocked markets this week. The first & harder to take back is the sudden & stunning decision by Jeff Bezos to raise salaries of all Amazon workers to $15/hour. Whatever his motives & tactics to hedge the increase in Amazon’s compensation costs, the public announcement scared bond investors as little else could. It created the scary vision of permanent wage raises for all workers through out America.

The next day came a very strong ADP and a stunningly high Service-Sector ISM. Long maturity Treasury yields exploded up by 10 bps. Added to the inferno were comments by Fed Chair Powell. Seemingly unconcerned about what he was signalling, Chairman Powell said the Fed might have to overshoot beyond what was thought to be neutral rate. That did it. Nothing could stop Treasury yields from breaking decisively out of the 30-year old channel. Friday’s NFP report did nothing to slow down the up move in rates. While the headline jobs number was much lower than expected, the revisions to August & July more than made up for the headline miss.

Unlike the Amazon announcement, Chairman Powell can take back at least part of his statements. Who expressed the strongest reaction to Powell’s comments? The same TV host who stunned everybody 10 years ago by ranting “they know nothing” on CNBC. Jim Cramer was only a pale version of that ranting red faced Cramer, but he was explicit. He said on Friday on his Mad Money:

- “That’s exactly what happens when the chairman of the Federal Reserve tells us he may need to overshoot with his rate hikes to ensure inflation is kept in check … It’s going to be hard for stocks to stabilize until he walks back those comments, or at least clarifies that he’s going to make his decisions based on the data rather than giving us a series of lockstep, autopilot rate hikes that the economy, as strong as it is with these employment reports, may not be able to handle”.

Then he added,

- “I see housing, autos and now, after this week, maybe even retail slowing, so it’s entirely possible the Fed is ahead of the curve already when it comes to stamping out inflation, … In the end, there’s only so much they can control, and these three industries really tell us that the rate hikes are already working like they’re supposed to.”

Chairman Powell certainly spoke like a bull & he created a stampede. But did this bull damage something? Is the US Economy more like a china shop which can be broken? While almost everyone would probably say no, David Rosenberg remembered something from 1970:

- David Rosenberg @EconguyRosie – Lowest unemployment rate since December 1969. Guess what? The recession started in January 1970…the one nobody saw except for Gary Shilling!

Look what Lakshman Achuthan of ECRI said this week:

- “For the overall economy, we have a yellow light. We think there’s a slowdown that’s happening here but on the housing and home price growth, absolutely it’s a red flashing light.”

“Our leading home price index has made a downturn that it hasn’t made in a long time … this leading index in 2006 really did call the housing bust“

“Our leading home price index has made a downturn that it hasn’t made in a long time … this leading index in 2006 really did call the housing bust“

This could spill over to the broader economy, he said.

- “The link really goes through the wealth effect … Instead of being a wind at the back of the consumer and consumer confidence, it’s now more of a headwind going forward. It remains to be seen just … how sharply this can fall, but the direction we have is clear“

David Rosenberg recalled some “famous last words” from Fed Chairs on Friday:

- David Rosenberg @EconguyRosie – “There’s no reason to think that the probability of a recession in the next year or two is at all elevated” (Powell, Oct. 18); “The Federal Reserve is not currently forecasting a recession” (Bernanke, Jan. 2008); <1/3>

- David Rosenberg@EconguyRosie – “Wedon’t have the capability of reliably forecasting a recession” (Greenspan, Dec. 2000) <2/3>

3. What’s Next for Treasury Rates?

This breakout could well prove to be secular.

- Jeffrey GundlachVerified account@TruthGundlach – Two consecutive closes above 3.25% = a breakout from multiyear head&shoulders base. Last man standing is down. 7/16 was indeed the rate low.

What is a technical target for the 30-year yield?

- Peter BrandtVerified account@PeterLBrandt –

#Factor_MembersGenerational breakout in T-Bond yields. A three decades long bear market in yields is now officially over. Targets for 30-Yr Bonds 4.37 and 5.04.

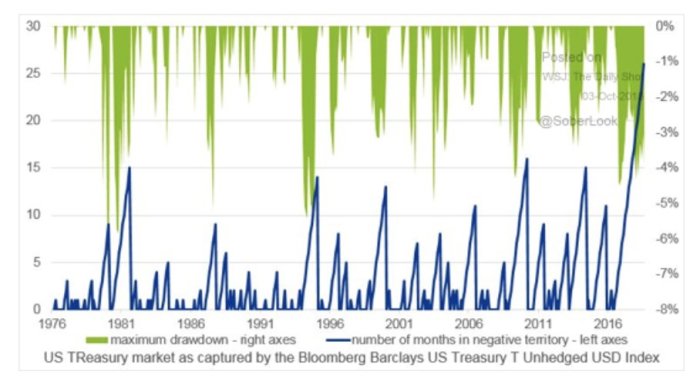

It is highly unlikely yields go there in a straight line. Already, the fall in Treasury prices has been historic both at short & long end:

And on a total return basis:

And on a total return basis:

- Trevor Noren@trevornoren –“Treasuries have experienced the longest losing streak (on a total-return basis) since 1976 (perhaps even earlier).” https://blogs.wsj.com/dailyshot/2018/10/03/the-daily-shot-u-s-farmers-are-hurting/…

So the question is when does this explosion in yields simmer down? Believe it or not, one says almost now:

So the question is when does this explosion in yields simmer down? Believe it or not, one says almost now:

- Thomas Thornton @TommyThornton –

$TLT has a downside DeMark Sequential Countdown 13 today. And the Erlanger short interest intensity rating is 92%. Short squeeze potential. I’m waiting for first day up to start small long and will add when above 4 previous closes.

Jim Bianco said on BTV that this leap in yields will be short lived without rising inflation. He added rates might keep going for a couple of more weeks but he thinks we are near the end of the move rather than near the beginning.

Jim Bianco said on BTV that this leap in yields will be short lived without rising inflation. He added rates might keep going for a couple of more weeks but he thinks we are near the end of the move rather than near the beginning.

Bianco then made a major point that has also been made by Gundlach. He said the relationship between stocks & bonds might be changing.

- “The worst thing that could happen to stocks would be rising interest rates on the back of inflation. This is the 1970s-1990s model. We might be transitioning to that. “

In that case, as Bianco said, asset allocation could be the toughest decision ahead of investors & asset managers.

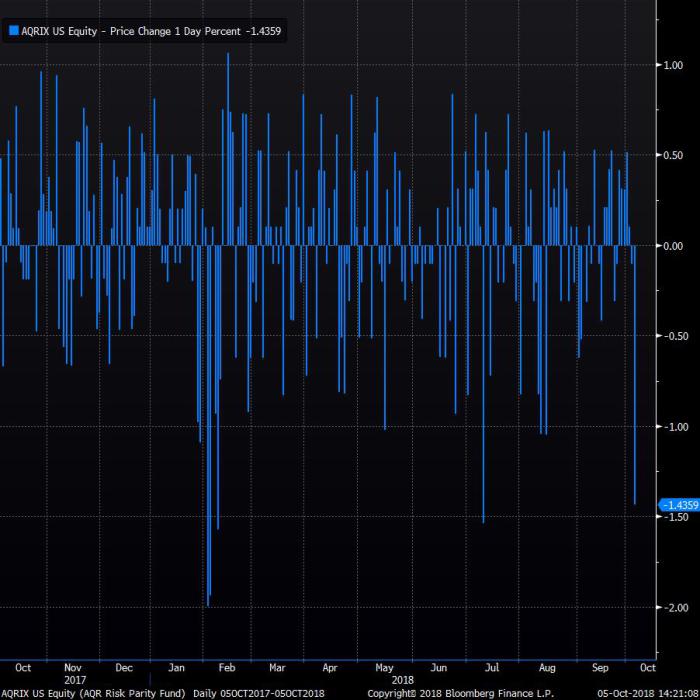

What happens to Risk Parity funds in that case? Look what just one day did:

- Luke Kawa @LJKawa – Yesterday was one of the worst days of the year for the AQR Risk Parity Fund, fwiw

4. Equities

First the good vibes:

- Urban Carmel @ukarlewitz – Equity-only put/call ratio popped to 0.84, the highest since the Feb low in

$SPX. In 19 of last 21 (90%)$SPX closed higher w/in 5 days by avg 1.5%$CPCE

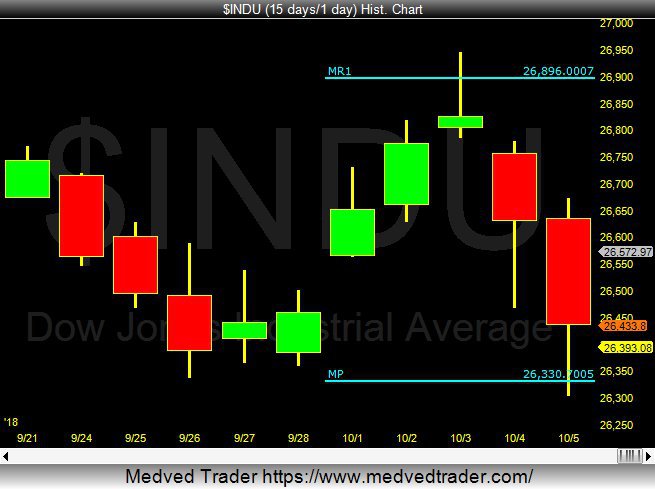

The distance to a monthly pivot is not far:

- Jeff York, PPT @Pivotal_Pivots –

$DJIA this past week, the Monthly R1 to Monthly Pivot(MP).#Pivot2Pivot@PivotalPivots

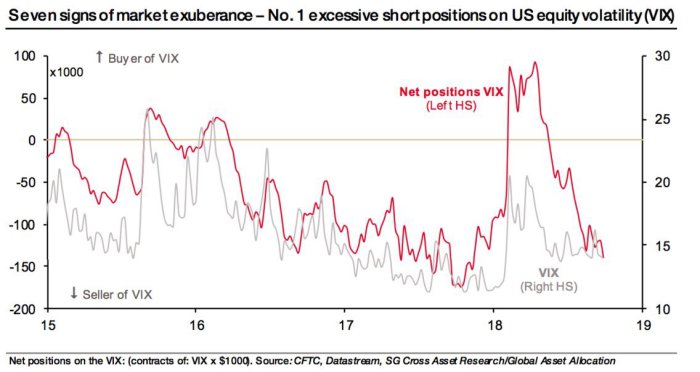

A bad warning comes from:

- Jesse Felder @jessefelder – Hedge funds’ short-VIX positions are once again approaching historic levels. https://www.businessinsider.com/hedge-funds-bets-similar-to-dotcom-bubble-socgen-2018-10 …

And the worst negative:

And the worst negative:

- Chris Kimble @KimbleCharting –Stock Indicator back at 2000 & 2007 levels says Joe Friday https://kimblechartingsolutions.com/2018/10/stock-indicator-back-2000-2007-levels-says-joe-friday/ …

- “This chart compares the spread between the 10-year yield and the 2-year yield to the performance with the S&P 500. Even though this indicator is based up government bond yields, it has proven to help stock investors know when to be overweight and underweight stocks.”

- “When the spread was very low in 2000 & 2007 and turned up, the S&P was very near an important peak in prices.“

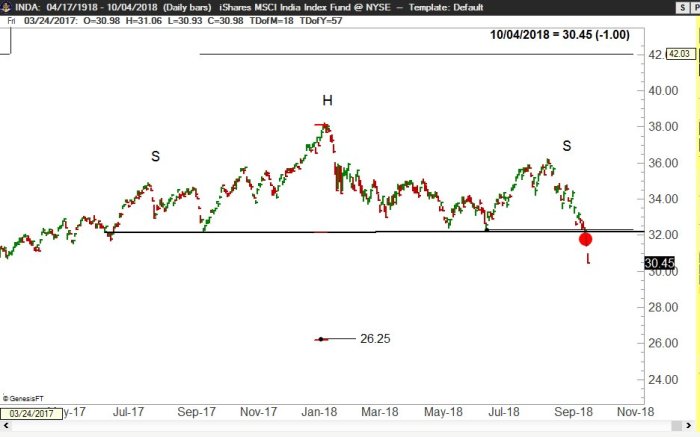

On Friday Tom Keene of BTV almost devoted a segment of his show to India and the Reserve Bank of India deciding to NOT raise rates. Urjit Patel, the governor said, protecting the Rupee was not part of his mandate. The Indian Sensex fell by 1,500 points in the last two days and the Rupee crossed over 74/$. But what about the Bank index?

- Jeff York, PPT @Pivotal_Pivots –To my followers in India, look for support on the BankNifty soon at the Yearly Pivots(YP), since the High this Year was at the Yr1 Pivot.

#TradethePivots@PivotalPivots

On the other hand,

On the other hand,

5. Commodities

And,

And,

- Peter BrandtVerified account @PeterLBrandt – Bottom in Gold. Close above 1215 important $GLD $GC_F

What about Oil?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter