This week the world’s biggest market cap company, the world’s biggest corporate icon, the company that has done more to bring the world together with its smart phone did something unimaginable. They announced a steep fall in their revenues in the past quarter. And they blamed it on China, on weaker Chinese demand for their phones.

This was a body blow for expectations of global growth and interest rates plunged across developed markets because of potentially slower growth. But, by the end of the week, the US stock market was up over 300 points and the tech-heavy Nasdaq 100 (with Apple as its biggest component) rallied 2.2% on the week. This rally had nothing to do with China or Apple. It had everything to do with the dovish US Federal Reserve which finally listened to markets.

So this week was a big win for America and a big warning for China as well as to US companies that depend on China for a large portion of revenues. Kevin Hassett, chief economic advisor to President Trump, warned of more apples falling:

- “There are a heck of a lot of U.S. companies that have a lot of sales in China that are basically going to be watching their earnings be downgraded … until we get a deal with China, … It’s not going to be just Apple.”

Hassett added:

- “I think that puts a lot of pressure on China to make a deal, … Their economy, for them, you might call a ‘recession.’ It’s slowing down in a way that they haven’t seen in a decade.”

This fits, at least partly, with our thesis articulated last week in our article 2019 – A Cycle Change?:

- “Now, we think, a new cycle is beginning. A cycle in which consuming nations/regions will take back wealth and capital from production powerhouse nations/regions.”

1.China’s Response & a Major Shift Underway

What was China’s response? China’s Central Bank, PBOC, cut the Reserve Ratio for China’s Banks by 1% (1/2% on Jan 15 & another 1/2% on Jan 25). This is not a gentle nod. Instead it is taking a 2 x 4 to the economy, to use a favorite expression of veteran strategist Dennis Gartman. It means giving a big surprise or a great shock, kinda like what you would feel after being hit with the 2×4 below from Home Depot:

This aggressive move will release 800 billion Yuan (about $117 billion) of liquidity into Chinese banks to support economic growth. This is a much broader move and is in response to a slowdown from the trade dispute with the Trump Administration.

We have all known that China is slowing and has been slowing for years.

So what is different now?

So what is different now?

- Lisa AbramowiczVerified account @lisaabramowicz1 – Chinese consumers are spending less due to higher costs of living & economic uncertainty, helping to drive the nation’s slowdown. This is different from prior downturns in China. https://www.wsj.com/articles/

chinas-economic-downturn- takes-the-shine-off-its- resilient-consumers- 11546513717

The article says:

- “China’s current economic slowdown differs from previous downturns because this time Chinese consumers are taking a hit. A less-certain economic outlook, the trade fight with the U.S., rising living costs and expectations of slower income growth are weighing on household spending. Meanwhile, slowing sales, rising costs and trade-related uncertaintiesare squeezing businesses’ profit margins, from retailers to manufacturers.”

- “Retail-sales growth—which has been fairly resilient during previous slowdowns—dropped to its lowest level in more than 15 years in November. And the government’s efforts to cut personal income tax has failed to lift spending.”

This is not just a slowdown but a major shift or as we put it – a Cycle Change:

- Jesse Felder @jessefelder – There is a major shift in the Chinese economy that is quietly beginning to upend the global financial system. https://www.wsj.com/articles/

the-china-story-that-is-far- bigger-than-apple-11546598005 …

What is a succinct summary of this shift? Look at a retweet of the above Jesse Felder tweet:

What is a succinct summary of this shift? Look at a retweet of the above Jesse Felder tweet:

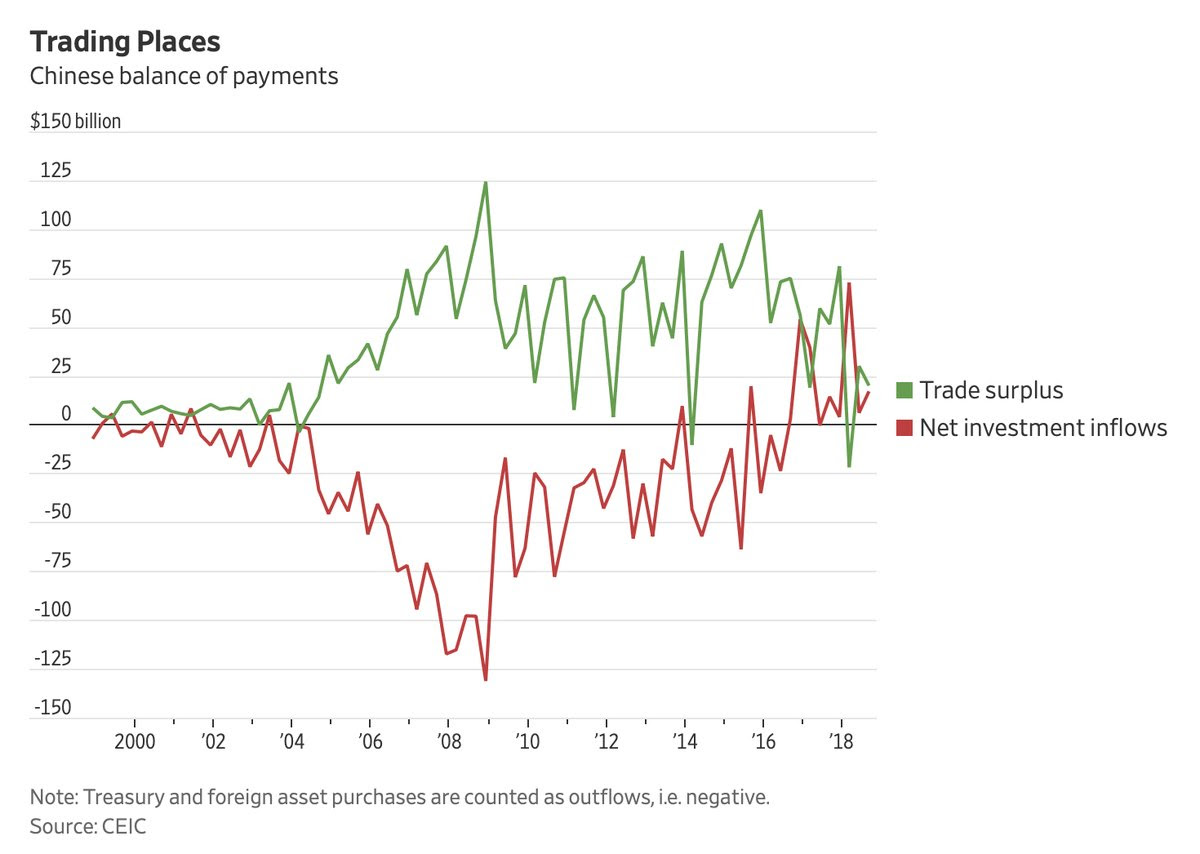

- For What It’s Worth@FWIWmacro – For What It’s Worth Retweeted Jesse Felder – “Over time, what will matter more to global markets is the big rise in Chinese consumer demand, the big fall in Chinese savings, & the big increase in #China’s need for foreign capital.”

This would be a tectonic change indeed. For one, it would upend the One Belt One Road master plan that depends on China’s exporting its capital to invest/buy foreign geostrategic assets. Secondly, it would have major ramifications on the Chinese Currency & its social structure.

Where could you read more about it? In the recent book by George Magnus titled Red Flags – Why Xi’s China Is In Jeopardy.

2. Four Traps of Magnus

We can all talk about a major shift but what does that do to traditional analysis which relies on extrapolating recent history & events. But as George Magnus explains in his Chapter 3 – The End of Extrapolation:

- “China has reached a point we can call the end of extrapolation. It simply cannot continue to develop on the basis of the economic model that has existed until now. More credit-filled investment will risk economic and financial instability, possible leading to an abrupt and painful growth crunch. In the medium to longer term, rising inequalities and environmental degradation risk both significantly slower growth and major social dysfunction. Consequently, China needs to develop a more sustainable growth path and development model. This much, at least is recognized well by Chinese leadership. The question is how to construct and deliver it while keeping the Party in total control.”

These two variant & possibly conflicting objectives lead to 4 different traps that China faces.

2.1 Debt Trap

Chinese consumers of today are not the Chinese consumers of 2002. Magnus tells us that “Household borrowing … may have already reached 60% of GDP and on current trends, it could be on course to reach … 90% of GDP by 2020“. That folks is next year. That means a loss of confidence in the future can affect the Chinese economy more severely than ever before. And what gets affected the most when households shrink on spending? Luxury goods like $1,000 Apple iPhones.

And China has NEVER experienced a significant fall in real estate prices just like Americans had never experienced a significant fall in home prices till 2008.

So what about China’s banks? They include the World’s 4 largest banks just like Japan was home to the World’s 10 largest banks in 1989 just before Japan’s financial crisis and America had the World’s largest three banks in 2007, just before you know what.

If this is not enough, Magnus writes:

- “China’s financial assets and liabilities have exploded in recent years to more than five times its GDP, that a substantial part of this has happened away from the main Chinese banks and that much has occurred in the lightly or weakly regulated shadow banking system.”

Sounds familiar, doesn’t it? But this is unlikely to create a systemic debt crisis. Instead, Magnus opines:

- “It is much more likely that debt will loom over the economy, manifesting itself as lower economic growth than a crisis per se.”

2.2 Renminbi or Currency Trap

How did America manage to survive & prosper in spite of its debt crisis? First & foremost, America has a global currency and America allows foreigners to acquire & accumulate US bonds & other US assets. Secondly, America has the world’s broadest, deepest & most liquid Bond market & other capital markets.

China wants to make its Renminbi a significant global currency. But as Magnus writes:

- “There are, though, only two ways this can happen. One is by running current account deficits, so that foreigners receive more of your currency than they pay for goods and services. The other is by having an open capital account, so that capital flows freely abroad.”

The US does both while the likelihood of China doing either “any time soon is negligible“. In fact, tight controls on outflow of capital is the only way “China can sustain its monetary autonomy and its exchange rate system“.

And capital controls work mainly when there is confidence in the currency. Witness the flight of capital out of China in 2015-2016 & China’s devaluation of its currency. So Magnus opines:

- “In the years ahead, it will not be possible for China to sustain a stable exchange rate and stable reserves, if banking system assets continue to grow significantly faster than reserves and GDP. The Renminbi’s fortunes, then, are inextricably linked to the manner in which China eventually resolves its debt and deleveraging problems”.

2.3 Ageing Trap

The growth rate of a society’s working-age population (WAP) is a major macroeconomic factor. The current 36 year bull market in America began in 1982 as a huge wave of young people (Baby Boomers) were entering the work force. Today, as this large group of Baby Boomers is retiring, an even larger group called Millennials is entering the work force.

China is facing a radically different situation. As Magnus writes,

- “In 2012 China’s WAP fell for the first time, by 3.45 million people, and the rate of decline is going to accelerate significantly after 2020, with the biggest annual losses (around 7 million a year) occurring between 2025 and 2035. From a current level of just over 1 billion people, the WAP is predicted to decline by 213 million by 2050.”

What does this mean for China’s GDP?

- “This … feeds directly into lower trend GDP growth, which may be no higher than 3, possibly 4 per cent“.

So China faces slowing growth due to its huge debt; it cannot attract foreign capital in size because of Capital Controls; and its working age population is shrinking. So what could be a solution? Improve the productivity of workers.

That leads directly to the fourth trap.

2.4 Middle-Income Trap

Middle-Income trap is a term used to describe economies that are squeezed between low-range, poorer competitors and high-wage, richer innovators. Most countries remain trapped in this middle. Only a handful countries have managed to enter the rich echelon – Malaysia, Singapore, South Korea, Hong Kong, Taiwan and Thailand. Others like Brazil are not that different than they were 50 years ago in terms of income per head.

The key seems to be increased productivity of the labor force. China gets it and they are “going all out for technology leadership“. George Magnus discusses a number of factors that might create problems or obstacles for China in this endeavor.

We will restrict ourselves to the most important – Trump Administration. China’s drive to become a technology powerhouse and that too by stealing a great deal of American technology has been identified by the Trump Administration as a fundamental threat to America. The Trump Administration has committed America to preventing President Xi’s 2025 plan and its dependence on stealing American technology.

This will be a slow determined drive to shut down Chinese acquisition of critical technologies from America, a drive that is likely to increase tensions between the world’s two largest economies.

That brings us to the important question.

3. Is China like Europe, Japan of 1990s or Japan of 1930s?

Europe became a big economic challenger to America’s dominance in the early years of this century. Remember how some supermodels & athletes chose to accept payment in Euros instead of Dollars in 2006-2007. That European challenge ended after the 2008 financial crisis. Europe remains mired in systemic slowdown with negative interest rates & trillions of Euro bonds paying negative interest. The EU, launched with fan fare, is about to get cut down after Merkel leaves.

Japan went bust in 1989, four years after signing the Plaza Accord with America and remains mired in low-growth negative interest rate malaise since then.

In any case, neither Europe nor Japan presented a strategic or military challenge to America. Both were beneficiaries of America’s military & strategic protection. That freed economic resources for them to compete with America.

China is radically different. China knows it may have to engage in a military conflict with America and China has been building its military to be able to protect its neighborhood against American military. This reminds us of 1930s Japan. That Japan when faced with increased trade & economic pressures from America chose to go to war with America.

Will the economic pressures get so hard to manage that China feels necessary to take over resources of its neighbors? Will China at that point feel confident or reckless enough to engage America militarily? After all, didn’t a Chinese Admiral recently threaten to sink two US Aircraft Carriers to teach America a lesson?

Or will China, like Japan & EU, slowly & peacefully accept a slower rate of growth & a weakening economy?

That is one question George Magnus does not touch and one that probably no one can answer.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter