Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Way to go!

Chairman Powell succeeded this week.

- Lisa AbramowiczVerified account @lisaabramowicz1 – Fed Chair Jay Powell has succeeded in dampening market fears of a near-term downturn. Aside from the rally in risk assets, yield curves are widening, with the gap between 2-year and 10-year Treasury yields increasing by the most for a two-day period since February 2018.

The 3 major stock indices in the US went to new all-time highs and the Dollar weakened a bit. And all this while keeping his “credibility” vs. the President intact. And emerging markets went down as US indices rallied hard.

The 3 major stock indices in the US went to new all-time highs and the Dollar weakened a bit. And all this while keeping his “credibility” vs. the President intact. And emerging markets went down as US indices rallied hard.

For once, Powell’s delivery was perfect. He was confident & he was happy. And he also created a triumvirate and a bipartisan one at that. This was the week in which our early 2019 prediction* came true. Which prediction – the one about the left of the Democrat party joining President Trump’s cause of lower rates to help the workers of America. The big surprise was the happy alacrity with which Chairman Powell joined ACO in this cause that President Trump has led for over a year.

It was clear that Powell knew that the Congress, especially the House, is his boss. And he knows where his risk lies – not with Speaker Pelosi but with the new insurgents led by ACO & her merry band. If they can accuse Pelosi of racism, they can easily & truthfully accuse Powell & the Fed of being truly responsible for the income-wealth inequality in America. And ACO has already begun:

- Alexandria Ocasio-CortezVerified account @AOC – “Ocasio-Cortez’s implication is that, by raising interest rates out of a fear of illusory inflation, the Fed may have needlessly hurt American workers. Powell’s concession on that point is significant.” http://nymag.com/intelligencer/2019/07/aoc-is-making-monetary-policy-cool-and-political-again.html

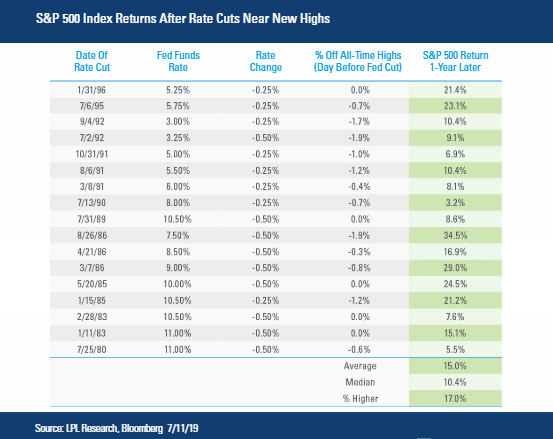

So if the economy does indeed keep slowing the way it is doing now, expect Chairman Powell & his FOMC to get more dovish as both President Trump & ACO want. And what happened in the past when the Fed cut rates near all time highs in the S&P 500?

Take a look at the top two cases in the table above – those are precisely the rate cuts of Greenspan that Chairman Powell had praised. No wonder Lawrence McMillan wrote in his Friday summary:

- “In summary, the indicators are bullish and thus so are we. While there are some overbought conditions, and there is some lagging in breadth, those things don’t really matter as long as $SPX remains above support.”

If all this is not enough, look at the new angle introduced this week.

- Bloomberg TVVerified account @BloombergTV – The chances of direct intervention by the U.S. to weaken the dollar is “low risk, but it’s growing,” says Nick Bennenbroek of Wells Fargo Securities http://bloom.bg/2XYm3gB

And don’t we know what happens to a country’s stock market when that country’s currency gets devalued? And isn’t a potential devaluation of the Dollar a viable reason to ignore the profits recession that Morgan Stanley, Rich Bernstein are predicting?

Think what we might see in the months ahead – a not-hot economy, a committed dovish Fed & a President committed to lower the Dollar! No wonder Jon Najarian pointed out a large trade in September S&P 325 calls and Scott Minerd of Guggenheim used 3,500 as a potential target for S&P on CNBC Closing Bell.

What could go wrong?

2. D & R words

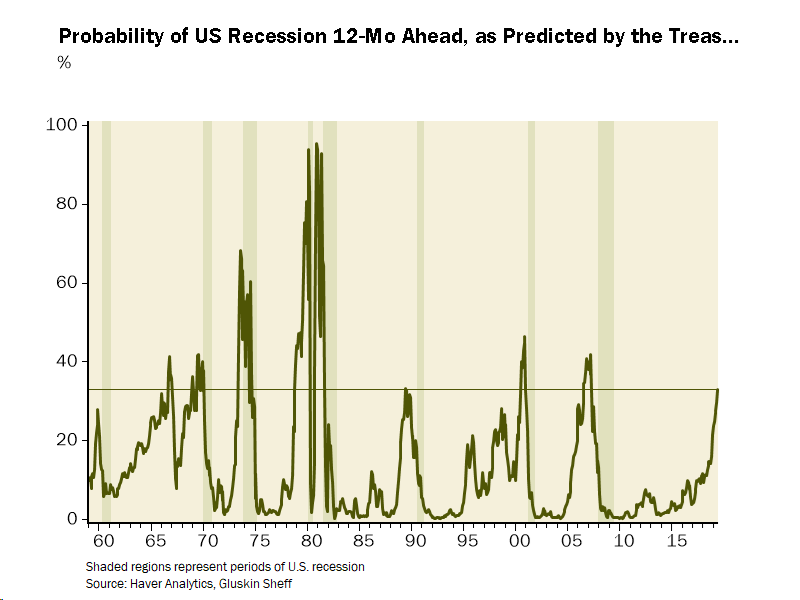

- David Rosenberg @EconguyRosie – For those who “can’t see the recession”, it’s illustrated for you in this chart. The NY Fed model now pegs recession risk at 32.9%, a 12-year high. History shows there’s no turning back at this level.

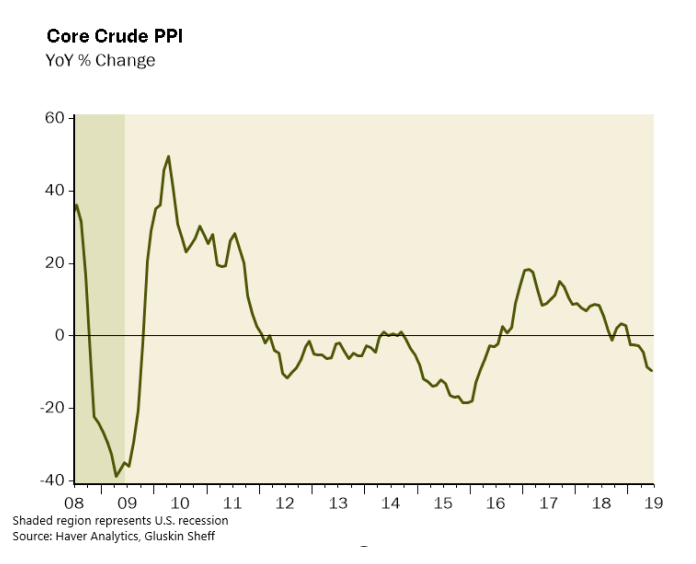

- David Rosenberg @EconguyRosie – Core crude PPI (the earliest stage of the production process) fell 0.5% after declining 4.5% in May and 1.2% in April. The YoY trend, which was already firmly in negative terrain, melted further – to -9.6% in June from -8.6% previously. Deflation risks dominate.

Last week, we highlighted the impending decline in world trade. What might that suggest? That mostly closed economies would fare much better than economies dependent on global trade? Is that already happening?

- jeroen bloklandVerified account @jsblokland – Stimulus waning? #China‘s economic surprise index is down to its lowest level in four years.

And,

And,

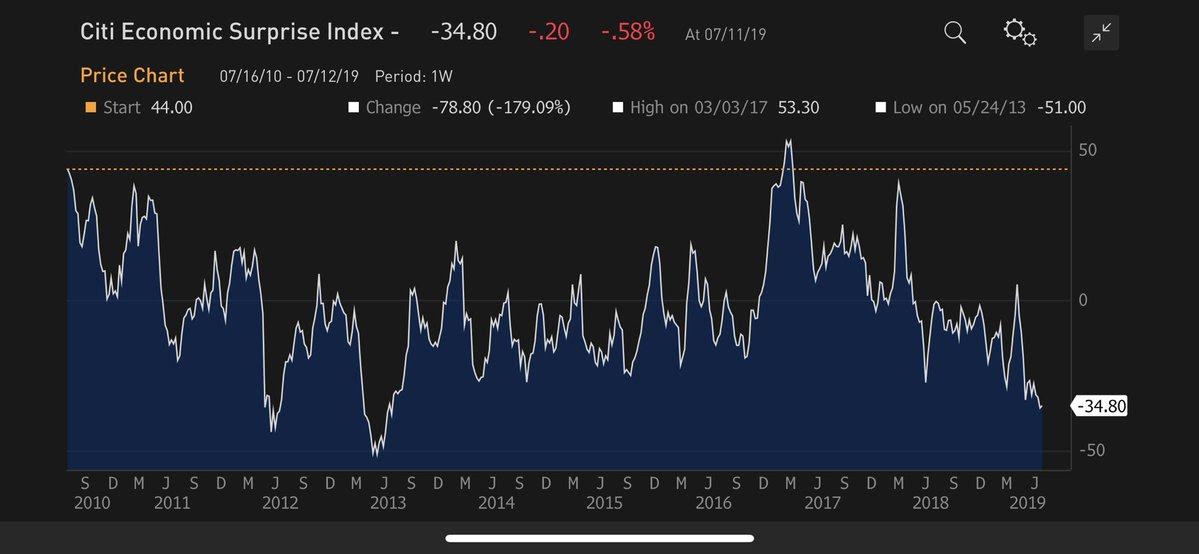

- jeroen bloklandVerified account @jsblokland – Uh-oh! The Citi Economic Surprise Index for Emerging Countries has dropped to the lowest level in more than six years.

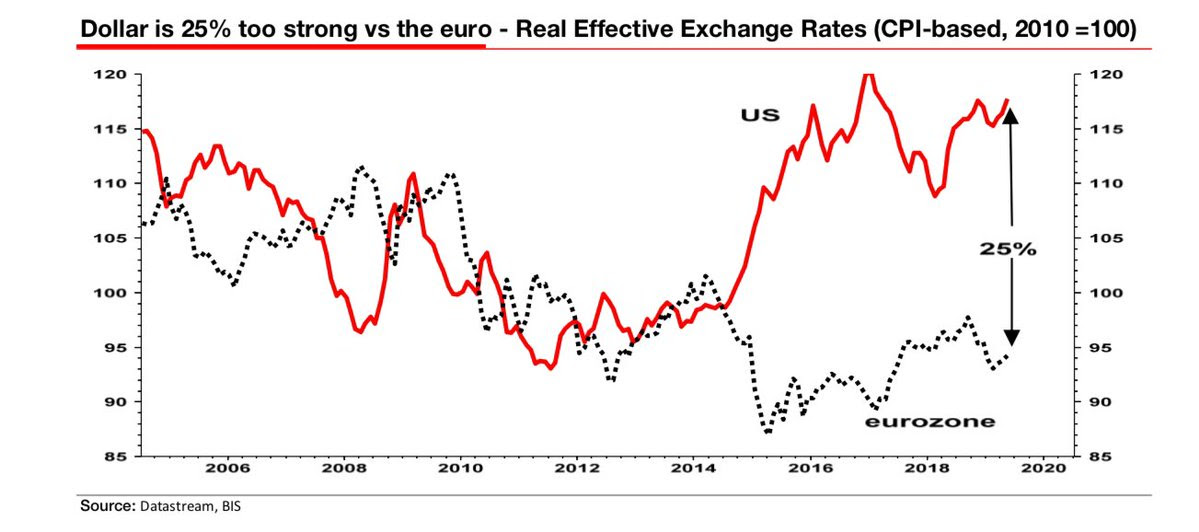

Notice how President Trump has been relatively quiet or even passive about China & other EM countries. Is that because he has decided the real problem for the US is the EU as Paul Richards of Medley Global said last week on BTV?

- Albert Edwards @albertedwards99 – The eurozone is now President Trump’’s very clear target. Any further ECB easing will be likely to cause an explosion of anger. And you know what? I think Trump has a point. He is going to drive the dollar way lower as the global currency war intensifies. https://www.zerohedge.com/

news/2019-07-11/albert- edwards-us-about-take-global- currency-war-whole-new-level …

Could we see a competition between ECB & the Fed to see who can deliver more easing from here? Don’t laugh at us for asking the question. Scout’s honor, we heard Scott Thiel of BlackRock say on BTV Surveillance that the ECB has more room than the Fed to deliver easing while Matt Horbach of Morgan Stanley said on BTV Real Yield that the Fed has more room than the ECB.

Who would have thought that we could see big time strategists actually discuss a potential competition between the ECB & the Fed to lower rates more than the other? After all, isn’t QE another name for currency devaluation?

3. “… rally has been unbelievable“

Which rally? The unbelievable rally in peripheral European credit, as Kathy Jones of Schwab said on BTV Real Yield. What happened in the past 48 hours has been stunning. Money flushed out of German Bunds & other high quality Sovereigns to go into European peripheral debt in search for yield. As Market Ear posted on Friday early morning:

- GERMAN 10 YEAR YIELD HAS GONE FROM -0.4% TO -0.24%, FRENCH 10 YEAR YIELD HAS GONE FROM -0.14% TO +0.06%…BIG MOVES IN PERCENTAGE TERMS….

Since a picture is worth 1,000 words,

- jeroen bloklandVerified account @jsblokland – #YIELD! German 10-year bond yield in one chart.

As we had written last week, “Nothing would move US Treasury yields higher & faster than a rise in German Bund rates.” Naturally, the US Treasury curve steepened bigly this week with the 2-year yield DOWN 2.4 bps and the 30-year (10-year yield) up 10 bps (8 bps).

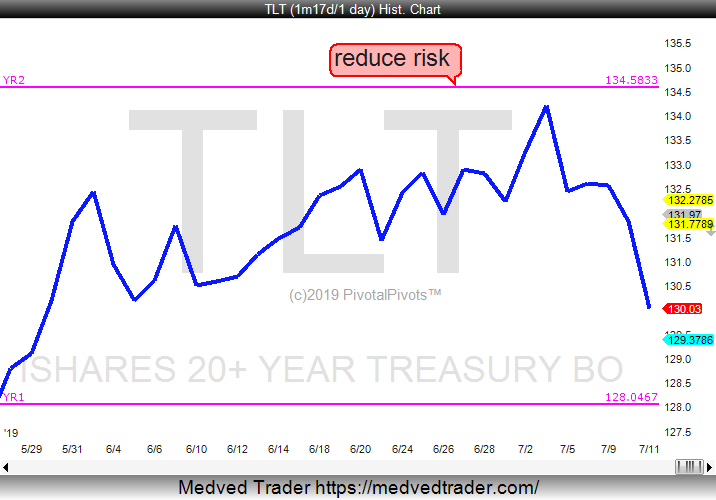

So where could TLT go in this correction?

- Jeff York, PPT @Pivotal_Pivots – $TLT could go back to Yr1, since Yr2 was strong resistance! #TradethePivots @PivotalPivots

What does the man who said “Buy Bonds, Wear Diamonds” say now?

- Raoul PalVerified account @RaoulGMI – I closed every single fixed income position globally, except one, a couple of weeks ago and I’m frothing at the mouth to get back in but a tad more patience is required for all the charts to fill their gaps and repair weekly DeMarks and over bought indicators. Nearly there…

Jim Caron of Morgan Stanley said on Friday on BTV that the most crowded trade is high quality duration. And the majority of gurus we heard on BTV said fade duration now instead of fading credit. The one exception was Matt Hornbach, also of Morgan Stanley, who said buy duration. Also, of course you know who!

- David Rosenberg @EconguyRosie – I see a lot of noise in these latest CPI and PPI reports. The US economy is slowing and the latest JOLTS data showed hefty pullbacks in job openings and hirings. The backup in bond yields is going to present a nice buying opportunity in Treasuries.

Note Rosenberg uses the future tense in the above tweet. Perhaps because he, like his ex-colleague Jim Caron, knows the pain trade right now is both stocks & interest rates going up.

*For a detailed discussion of monetary-politico ramifications of ACO-Kudlow, see our adjacent article The Game Just Got More Momentous & Much More Interesting.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter