Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.”How is the Josh?”

Look at Indian Finance Minister Nirmala SithaRaman asking this question in a cinema hall in Bengaluru?

This question was sent all across the Global Indian Diaspora & through out India this morning. The “how is the Josh” line was made famous in the recent film Uri about Indian Army’s special forces teams conducting surgical strikes inside NaPakistan. The term “josh” was used in that film as adrenaline ahead of the attack & the exultation after the successful strike.

On Friday, this question was used to celebrate animal spirits freed after the stunning corporate tax cut announced by Ms. SithaRaman & the Narendra Modi cabinet. This step was taken in the characteristic Modi manner – let the discomfort & criticism about slowing growth build, take the necessary steps in secret & then one day announce it as a fait acccompli. Just like a surgical strike with stunning surprise & operational efficacy.

And how was the josh in India after the news? The Sensex rallied by 1921 points & the broader Nifty by 569 points, both about 5.3%. The NYSE-listed ADRs of Indian private banks, HDFC (HDB) & ICICI (IBN) rallied over 9.3% on the Friday.

But there was a broader & more global angle to this Indian action. And only Alix Steel of BTV, to our knowledge, discussed this global angle on Friday morning. She correctly & smartly pointed out that this was a case of “Government backing up the Central Bank“. How unique was this?

- Charlie Bilello@charliebilello Fed: easing ECB: easing BOE: easing BOJ: easing Denmark: easing Australia: easing Brazil: easing Russia: easing India: easing China: easing Hong Kong: easing Korea: easing Indonesia: easing South Africa: easing Turkey: easing Mexico: easing Philippines: easing Thailand: easing

The need for fiscal stimulus has been discussed on Fin TV since the appointment of Christine Lagarde as the incoming ECB head. The back up in sovereign rates in Europe & then in US was triggered by the speculation about Ms. Lagarde putting pressure on Germany for fiscal action. People like Mohammed El-Erian have been talking on BTV & CNBC about the need for infrastructure program in America and arguing that it was time for fiscal stimulus to act in tandem with monetary stimulus.

But when India actually implemented a large fiscal stimulus, only one anchor on BTV focused on the central reality – the Indian Government was acting in tandem with the Reserve Bank of India to implement a joint fiscal & monetary stimulus to the Indian economy. Kudos to Alix Steel. Strange that the self-proclaimed “first in business worldwide” network was either sleeping or ignorant.

At least CNBC’s Steve Liesman should have thought back to December 2018 when PM Modi managed to put in his chosen people on RBI’s governing committee and created the pressure that led the then Governor Urjit Patel to resign. In came ShashiKant Das, a veteran finance civil servant. Now the Indian Central Bank is working in tandem with the Finance Ministry.

How we wish Fed Chairman Powell could work in tandem with Treasury Secretary Mnuchin & President Trump to create a joint Fed-Treasury plan? How critical is fiscal stimulus in America? Bob Michele, head of Fixed Income at JP Morgan Asset Management told CNBC Fast Money after the FOMC:

- “A recession could be coming fast unless something happens on the fiscal side”

2. FOMC statement & a Yellenified Powell – “It’s really not you, it’s me”

Look what happened on Wednesday afternoon. The FOMC statement was hawkish despite the rate cut & both the stock market and Gold read it as hawkish. The Dow went down about 170 + points between the statement & the start of Powell’s presser.

Thankfully, it was a totally different Powell. He was light, honest & almost apologetic, a performance described by Lale Topcuoglu of J O Hambro as the “It’s not really you, It’s me” line. Not only was the line perfect but Lale’s delivery was also perfect. No wonder the BTV anchor, Alix Steel, just burst out laughing.

But that is what Jay Powell said – he made it clear 25 bps was the best he could do with 2 dissents but added that he would act if data did worsen & he would add reserves if the Repo crisis worsened. It was a Yellenified Powell & markets reacted as if they were listening to Yellen. Like Janet Yellen, Jay Powell sucked the volatility out of the markets & the Dow rallied to close up 36 points. This is visible in this week’s chart of SPY:

Chairman Powell’s Yellen touch lingered into Thursday morning with a nice rally but began tapering in the afternoon. Then it was dealt a body blow by Boston Fed’s Rosengren who explained why he was & remained against rate cuts. And it died around 1:10 when the Chinese delegation cancelled their trip. Look how both Treasuries (TLT) and Gold (GLD) acted after 1:15 pm on Friday.

Chairman Powell’s Yellen touch lingered into Thursday morning with a nice rally but began tapering in the afternoon. Then it was dealt a body blow by Boston Fed’s Rosengren who explained why he was & remained against rate cuts. And it died around 1:10 when the Chinese delegation cancelled their trip. Look how both Treasuries (TLT) and Gold (GLD) acted after 1:15 pm on Friday.

(TLT-Friday) (GLD-Friday)

The Yellen touch was wiped away & we were back to the July 31 post-FOMC set up – a Fed that is unable to act because of zealots & an economy that is about to slip into a slow down because of trade.

What happens in such conditions? Stock markets are weak, Treasuries rally, yield curve flattens & Gold rallied – result of a classic liquidity-constrained economic tightening environment. And what happened to the It’s not you, it’s me routine between Powell & the markets?

3. The US Economy – R & I words

- Richard Bernstein@RBAdvisors – Fundamentals apparently no longer matter to #investors. US Leading Indicator continues to plummet (11 straight months of slowdown), yet consensus favors cyclical #stocks.

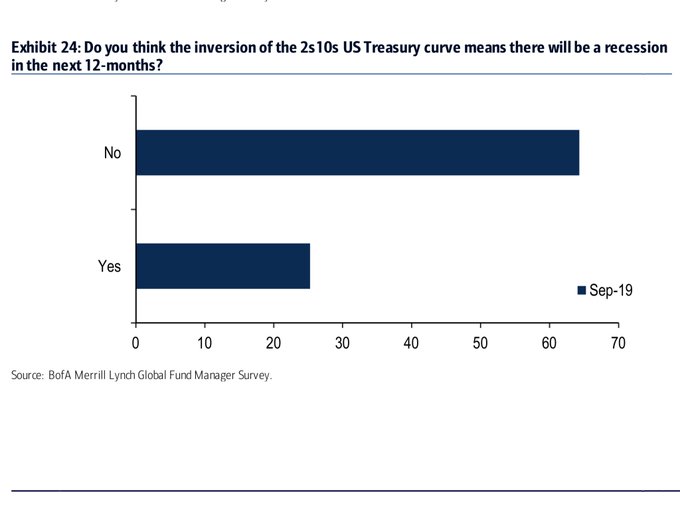

Yet, Rosengren & company don’t get it. They probably don’t even care about yield curve inversion:

- Richard Bernstein@RBAdvisorsTypical reaction. The #YieldCurve inverts and no one cares. (Source:@BofAML Fund Managers Survey)

But Rosengren & company remain focused on the US consumer & on the dangers of a bubble forming in corporate bonds.

- David Rosenberg@EconguyRosie – It’s hard to believe that 5 Fed officials want to raise rates at one of the next two meetings (only 7 of the 17 think we need another cut). Someone needs to buy these folks a Bloomberg terminal for Christmas. It’s not about the solid consumer but about weak exports and capex

We urge all to watch the entire one hour show hosted by Alix Steel on Thursday, September 19. The discussions by & between Peter Fisher (ex-everything & now professor) and Lale Topcuoglu of J O Hambro raise important points. For example, Peter Fisher provided a different way of making the point made by David Rosenberg above and linked the tariffs issue to business confidence:

- Boardroom & Country Club Animal Spirits – Business leaders can lose confidence; feel dangers of tariffs; that’s a reason to lose confidence; so the kind of a recession that is more likely to be in the offing is the 2001 recession which was a business investment recession; the household sector did not roll over; business investment just came way down & given how the corporate sector is now [leveraged], that seems to be the soft spot

Remember why the business sector finally went down in 2000; Greenspan tightened too much & for too long instead of providing liquidity sooner. Rosengren & company are going down the same path & by the time the US consumer shows signs of weakness, the corporate sector recession, so far evident in manufacturing, would be too far set to reverse.

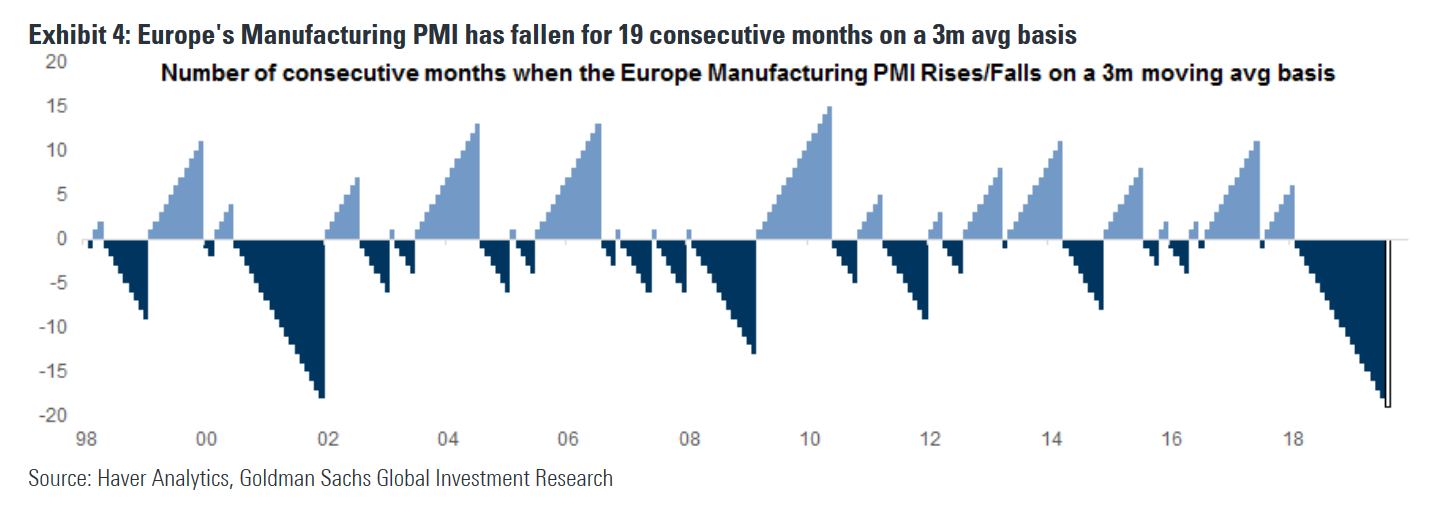

And the gaze of Rosengren & company seems to be focused westwards from Boston. If they were to look east, what would they find?

- Market Ear – The extreme PMI cycle… The longest and deepest PMI cycle during the past 20 years…. Cycles dont die of old age, but……

The resultant damage this time would not be to commercial banks, but it will happen to some one else said Peter Fisher. He pointeds out that the “Banks & Brokerage sector is no longer in the business of warehousing of risk“. So who is left? The corporate sector & the world’s Central Banks, who, according to Peter Fisher, “are going to be the biggest asset managers in the World“?

The resultant damage this time would not be to commercial banks, but it will happen to some one else said Peter Fisher. He pointeds out that the “Banks & Brokerage sector is no longer in the business of warehousing of risk“. So who is left? The corporate sector & the world’s Central Banks, who, according to Peter Fisher, “are going to be the biggest asset managers in the World“?

And so what will come? You guessed it – Volatility.

In this context, Mike Wilson of Morgan Stanley has a different & interestingly morbid view of a coming recession. He pointed out on BTV that Governments have capacity to deliver fiscal stimulus:

- It’s not like Europe doesn’t have the capacity [for fiscal stimulus]; they have tremendous, much more than we do; China may be out ok, but India has it [which India used the next day];. Brazil has it; You just need more pressure that a global recession [would provide]; a US recession in particular is exactly what the Doctor ordered for the political pressure to be used; & we are moving in that direction; So I am optimistic over the next 12-18 months that we are going to get that sequel;

So what is the big picture view Mike Wilson wants us to keep in our sight?

- “We go back to 2016 as beginning of global reflation; we stand firm by this view; that’s why we are still in a secular bull market; …… its a little premature; we may have retesting back & forth; but let us not lose sight of the big picture that global inflation has probably bottomed for years, decades … “

Jeffrey Gundlach also voiced a similar view in explaining why interest rates might actually rise at the long end during the next US recession. And Richard Bernstein, as we recall, is in the inflation is rising camp.

But, getting back to Mike Wilson, that is 12-18 months away & perhaps rates might fall at the long end at least until the recession actually gets here & people accept it.

4. Treasury rates

The slow down risk was relevant on the afternoon of Friday, September 20. That is why Treasury rates fell hard on Friday afternoon even at the long end. And what did they do for the last week?

- 30-year yield down 21 bps; 10-year down 18 bps; 7-year down 16 bps; 5-year down 15 bps; 3-year down 14 bps & 2-year down 11 bps; nice steady bull flattening.

Kudos to Rob Sechan of UBS whose final trade on CNBC Half Time (Friday, September 13) was to buy EDV, the Treasury Zero-coupon ETF. It was up 5.3% this week. The gentler TLT was up 3.9%.

German yields were also down hard with the German 30-year down 15 bps & the German 10-year down 8 bps.

5. Stocks

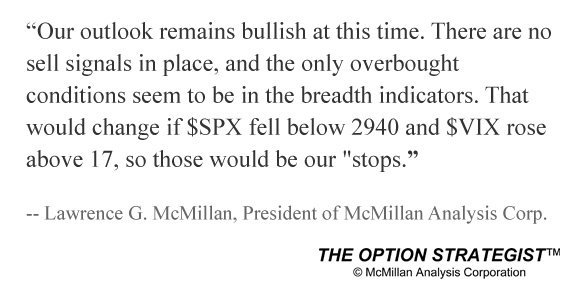

First the cautiously sensible approach:

- Lawrence G. McMillan@optstrategist – Weekly Stock Market Commentary 9/20/2019 optionstrategist.com/blog/2019/09/w $SPX $VIX #options #OptionsTrading

Then not a buy necessarily but don’t short opinion:

Then not a buy necessarily but don’t short opinion:

- Lloyd Blankfein@lloydblankfein – There’s an old adage, “don’t fight the Fed.” Means that if the Fed is on a tightening course, don’t be long. And if the Fed is lowering rates, as now, don’t be short. Doesn’t always hold true, but often enough to ignore. The Fed has a lot of tools to achieve its objectives.

What about positioning?

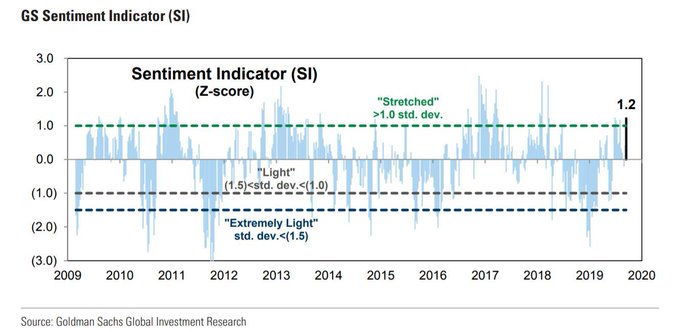

- Babak@TN – Goldman Sachs #Sentiment Indicator 1.2 (z-score) “Hedge fund net exposures are highest since July 2018, passive equity funds inflows last wk were highest since March 2019 (+$21B), & foreign investor equity demand is one standard deviation higher than its avg” Arjun Menon

What about next week?

What about next week?

- Market Ear – Flow picture turning neg next week?

- 1. Buyback black-out starts to kick in next week, and increasing over the next 3 weeks

- 2. month-end rebalancing should see significant equity selling next week, probably culminating

Wednesday or Thursday - 3. HFs have be re-grossing lately; gross now at 18 month high.

- 4. the large gamma long in the dealer community (mainly the 3000 strike) expires today, which on

balance, means that any flow will have larger market impact next week then it would have had this

week….

Emerging Markets were hit hard this week – Chinese ETFs down 3%, Korea down 1.5% & EEM down 1.8%. India was an exception but only because of the 5.3% rally on Friday. Yet,

- Market Ear – Emerging markets “VIX”, VXEEM, approaching “depressed” levels

The question is whether or not Emerging market risks should be priced in a “depressed” way?

6. Gold

Gold & Gold miners had a terrific week, again due to a large part to the cancellation of the Chinese delegation trip on Friday afternoon. Gold was 1.9% while Silver was up 2.9%. Gold miner ETFs, GDX & GDXJ, were up 7.6% & 8.2% resp.

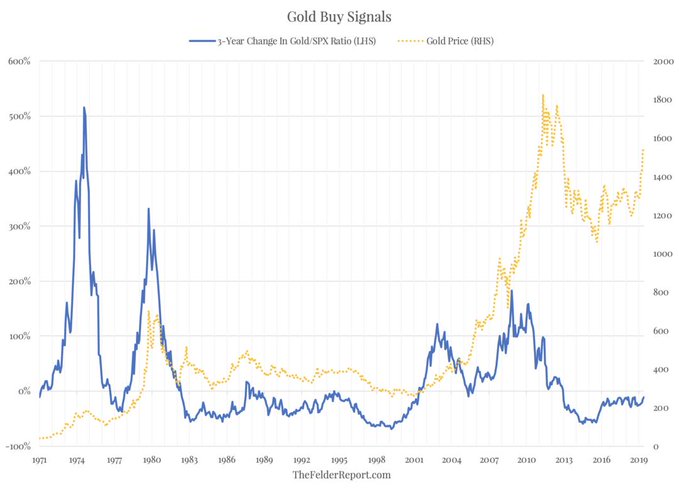

- Jesse Felder@jessefelder Sep 18 – NEW POST: Approaching A Long-Term Buy Signal For Gold Amid Short-Term Crosscurrents thefelderreport.com/2019/09/18/app

How does the channel look? Courtesy of Market Ear;

7. Trump, Modi, CNBC & Its Deep Hate

There is something more to the Modi-Trump show in Houston this weekend that no one talked about on Fin TV. It is a topic more relevant to Fox Business but that network, despite its strengths, doesn’t seem to have any bandwidth for Asian issues. Except Laura Ingraham on Fox who goes out of her way to bring out Asian-related issues on her show. But then, Laura Ingraham is a very smart & accomplished thinker & speaker.

This week, Indian-Americans have organized an event with PM Modi in Houston, TX, a meet titled Howdi Modi. In traditional Indian electioneering style, the sold out event will be a raucous rally with about 50,000 Indian Americans expressing their love & support for PM Modi. Just like a Trump rally, right? And that is the big deal. President Trump is going to attend this meet.

So far, the Trump campaign has not devoted much effort, at least publicly, to Asian Americans & especially to Indian Americans. But Indian Americans & Asian Americans in general are a toss up constituency. And the Indian American community loves Modi. They see, in him, the reflection, realizable reflection of what they know India can become. And like Trump, Modi is first & 100% for India.

It is very smart for President Trump to attend this event for Modi. He gets immediate mind-share not only among the 50,000 attending but among the entire Indian-American community in America & globally. And it is smart for PM Modi. He solidifies his & India’s standing in the Republican Senate & also in the House.

That brings us to the Fin TV network that, we believe, is First in Anti-Hindu, Anti-India hate. And we have first hand experience from 2006 when we began our attempts to build a dialog with CNBC Management. This Friday, CNBC anchors & reporters reverted to their true inner contempt when discussing this Trump-Modi event. It could well be that their deep Anti-Trump feelings combined with Anti-Modi, Anti-Hindu hate & they just couldn’t control themselves.

First it was a new voice. Dominic Chu, a nice guy we used to think. He asked CNBC’s resident BrIndian whether this meet finally legitimizes PM Modi as a true Prime Minister of India. We couldn’t believe our ears. An Indian leader who has won two huge (over 2/3rds majority) elections in India gets legitimized in the eyes of Mr. Chu as India’s Prime Minister because of a rally in Houston, TX!!!

If that conversation was bad, the subsequent conversation on CNBC Closing Bell let loose all their inner bigotry. CNBC’s code-word & the dog-whistle of hate towards Hindus & India in general is the deliberately contemptuous pronunciation of “Modi”. And the guy who led it is CNBC’s prominent Hispanic anchor, Carl Quintannia. He brought back CNBC’s own anti-Modi reporter of Indian origin who went nuts bringing in Kashmir & other anti-Indian fake stuff.

But this in itself is a progress of sorts at CNBC. This time no “white” anchor stepped up to join CNBC’s anti-India outburst. It was a parade of Hispanic & Asian minority anchors & they used, as CNBC often does, their resident India mouthpiece for insulting PM Modi by anglicizing his last name.

Our campaign to point out the anti-Hindu hate within CNBC has continued since 2006 despite the many changes within CNBC. Jeff Immelt & GE are gone & Brian Roberts & Comcast are in; Jeff Zucker no longer runs NBC & NBC has seen a revolving door of presidents. Tyler Mathisen is no longer the Managing Editor & Nik Deogun is gone. But two have remained in place – Mark Hoffman & his trusted sidekick Brian Steel. So the natural question is whether these two are the fountain head of CNBC’s ingrained Anti-Modi, Anti-Hindu hate? We don’t know.

But we do know that Indians are getting tired of the bigotry they see on US & European TV. And the moment is coming when Indians ask why should organizations like CNBC be allowed to function in India. After all Americans don’t allow foreign media organizations to succeed in America. Why should Indians allow BBC, CNBC to broadcast their hate in India & among the global Indian diaspora?

And the first victim of this backlash will be NBC entertainment & NBC Sports that are trying very hard to succeed in India & the second may be Comcast & Brian Roberts & their plans to be a global media entity. And if India acts, then some of the Asean countries might also follow.

Then Mark Hoffman & his US CNBC can keep abusing PM Modi as much as they like via deliberately mispronouncing “Modi” and now by questioning his legitimacy as India’s Prime Minister.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter