Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.He Gave, But ….

Last week, we began with a succinct “He Giveth & Taketh Away” title. He, of course, being Fed Chairman Powell. His taking away led to an ugly June 6-June 12 week with Dow down 5.5%, Russell 2000 down 7.9%, Transports down 8% and, horror of horrors. TLT up 5% while high yield ETFs fell 2.%.

Then the futures were down by 1,000 points early early morning on this past Monday. Guess the patience wore thin at the Fed. Is that why the Fed announced on Monday afternoon they were going to start buying high yield bonds, not ETFs, but actual credit of some companies?. That was a big deal and the markets promptly began moving up.

We saw the reverse action on Tuesday morning with futures up almost 1,000 points before Tuesday’s open. Stories came out about a Trillion Dollar Infrastructure program to be announced by President Trump and a story broke about an over-the-counter steroid proving effective in preventing deaths of seriously ill CoronaVirus patients. Add these to Monday’s Fed announcement & you can see why futures exploded on Tuesday morning.

But, unlike during prior mega-positive news days, stock indices did not keep going after the morning rally levels. Does that mean the stock market rally is over, resting or simply consolidating before another move up? Carter Worth, the resident technician at CNBC Options Action, simply said “the market is in a no-man’s land“.

On the other hand, Morgan Stanley’s Mike Wilson was clear and said “when risk premium appears, you have to grab it“. And his actually raised his base case year-end S&P target from 3,000 to 3,350. His 8-minute long discussion with BTV’s Jonathan Ferro & Tom Keene is worth watching:

Where is the bubble?

Do you really have to ask? Haven’t you heard that Credit leads stocks?

- David Rosenberg@EconguyRosie – Anyone think it’s been Dave Portnoy driving Ford’s 10-year junk bond to 19 cents above par? Avis (more junk!) at 117 cents on the dollar?? Or Viking Cruise’s five-year issue trading at a 15% premium to par? The bubble in credit makes the stock market look like a little sud.

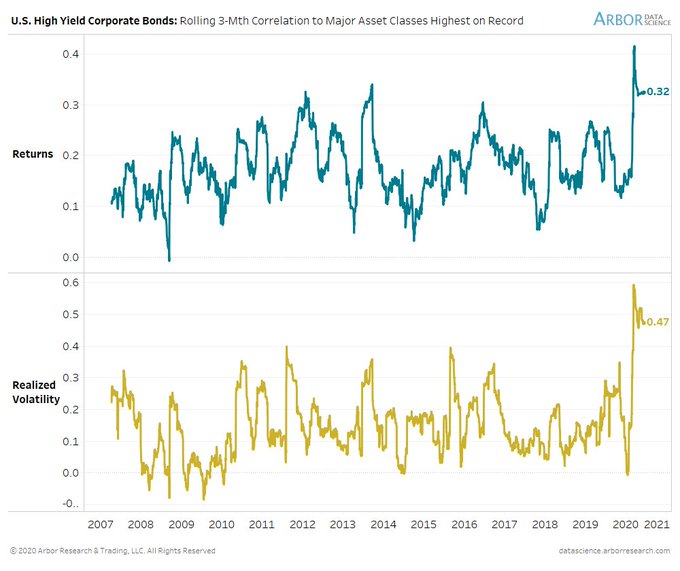

Another pandit preferred to use the fancy “correlation” term:

- Ben Breitholtz@benbreitholtz – Returns and realized vol of US high yield corporates have never been so correlated to major risk assets’.

In case you are tempted to short credit, you may want to read what BAML’s Michael Hartnett wrote this week (courtesy of The Market Ear):

- “summer risk remains to upside driven by central bank repression of credit spreads and big RoW macro surprise to upside via fiscal stimulus“

- “positioning, policy, credit markets all still point to potential for SPX >3250“

- “credit markets are too strong to short stocks – Credit markets all suggest overshoot viable…”

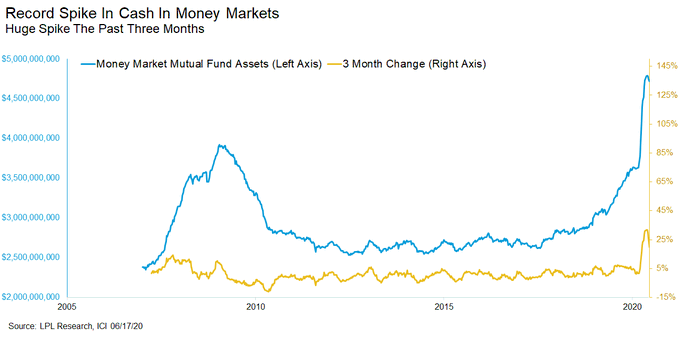

Where could the ammunition come from, you ask? One place is where there might be a real bubble:

- Ryan Detrick, CMT@RyanDetrick – Jun 17 – There is nearly $5 trillion in money markets currently. This is nearly double what it was five years ago. Also, the recent 3 month change was the largest spike ever.

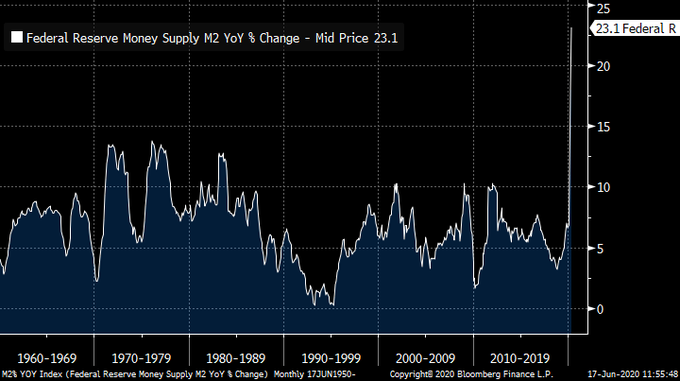

In case you are wondering what the Fed is doing to the money supply?

- Richard Bernstein@RBAdvisors – Jun 17 – HUGE uh oh: Updated US #M2 growth is now 23% y/y!!! Not only the highest in history but 2/3rd faster growth than in the #inflationary 1970s!!!

So Treasury rates should be racing upwards, right? Actually yields along the entire curve fell a bit this week. Heck, you can’t even get the 5-year Treasury to yield 40 bps. It looks as if it might drop to 30 bps or even below that.

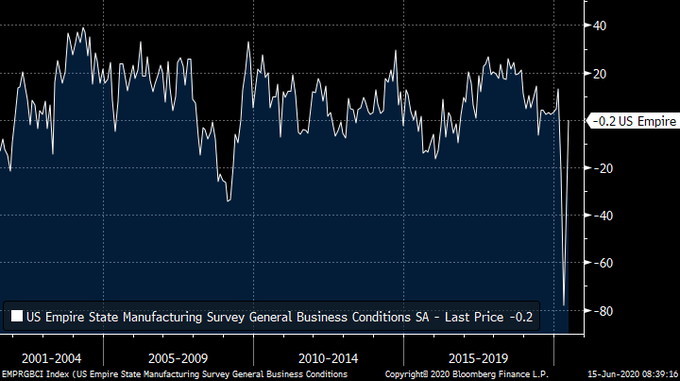

Then why is the stock market up? Mike Wilson said on BTV that the rate of change will remain up this year. Richard Bernstein put it another way:

- Richard Bernstein@RBAdvisors – Jun 15 – #Markets care about better/worse not the absolutes of good/bad. The US #economy is in absolutely miserable shape but is improving. NY #Manufacturing is the latest example.

Then he repeated the absolute vs. relative mantra on Friday morning about Leading Indicators. And this is a man who thinks the what the Fed is doing is dangerous:

- Richard Bernstein@RBAdvisors – Better or Worse? LEADING economic indicators absolutely terrible but relatively better.

But what about the relentless rally in the Nasdaq that is driving ahead of the broader indices? Aswath Daa-Mo-Daran of NYU explained on CNBC on Friday. He pointed out that, unlike in other recessionary markets, Risk capital, Public & Private, has not gone away; they perceive that there are companies that are still doing well and are likely to do even better next year:

*Editor’s PS – Those who wonder why India keeps getting slapped around by China should also wonder why smart “Hindus” like Prof. Daa-mo-daran allow their sacrosanct names to be mispronounced by US Fin TV anchors. It is the same attitude, an attitude that is diametrically opposite to “Don’t Tread on me” attitude of many others.

On the other hand,

- Market Ear- NDX -double top? Rather ugly down candle today.

.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter