Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.How sweet was it?

From the second stage of Monday morning to Friday afternoon’s propulsion, it has been something. Prior Thursday morning’s reversal sign from UK was indeed the first stage. That was so clear cut & so telling that the extremely rough CPI later that morning didn’t matter. Dow rallied 828 points, S&P up 93, NDX up 248 AND Dollard down 70 bps. Then came Friday’s reversal of Dow down 404 points & NDX down 342 with Dollar up 72 bps. That bothered us a lot.

But then we saw the Bespoke tweet we featured in our last week’s article:

- Bespoke@bespokeinvest – – Today’s was just the 5th time in $SPY‘s history (since ’93) that it closed higher by at least 2% after opening down at least 2%. SPY fell the next day 3 of 4 times, but it was up over the next week and month all 4 times. bespokepremium.com

Yes, the sample size was tiny but the timing was propitious. It was middle of October leading into 3rd & 4th weeks of that historical month. And we had the statistical support of Dan Niles who had said on Thursday, October 13 that

- ” … in the short term I actually believe October will end up being up; .. when you go into October with the market down 15% in the prior 9 months, odds of October being up are about 83% & your average gain is about 3%.. ”

You combine these with the amazing hand of Larry Williams & it was too much to stay bearish coming into this week. The timing was just too propitious to ignore. And Monday morning opened with the maturity of the new UK Chancellor Hunt and with the smart & astute bear Mike Wilson, articulating how momentous the UK reversal of Thursday October 13 was – “ … to be crystal clear … we think a tradable bear market rally began last Thursday … “.

Then noted technician, Ari Wald, came on CNBC to point out that a) the rally began around the very important (50% retracement level) of 3,500; b) the rally began with very deeply oversold market indicators & c) with the signs that downside intensity was abating. These together suggested a textbook opportunity for long term investors. His caveat was a missing piece – the upward action in interest rates that had driven the sell-off.

But the upward force was so strong that it took until Wednesday for the rates message to be heard. By Tuesday evening, the Dow had soared 889 points, SPX up 137 handles & NDX up 455. Then rates woke up again & Treasury rates rose in double digit basis points on Wednesday & Thursday. True to form 3-7 yr yields rose by 23-25 bps in these two days. Stocks wavered as a result with Dow down 190 points SPX down 54 bps & NDX down 91 bps.

So what would Friday bring? A steep decline in stocks as the past 4 Fridays had? Remember how stock market pandits always point out the wisdom of buying before mid-term elections! That’s because nothing is more momentous that the political need for a good market of the mid-term election, especially an election that could change the political power base of America.

Look what the Inside Job article by Bear Traps Report said on Saturday October 22:

- “We believe they put a phone call in to Fed chair Powell seeking important, corroborating support.“

Who were “they”? And what did they need from the Fed? Guess what the Inside Job article said?

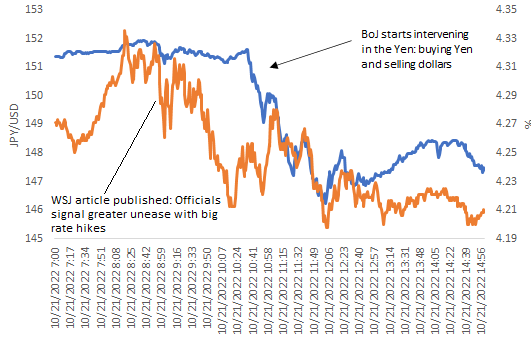

- “At 9 am Friday morning, the WSJ’s Nick Timiraos made a market-moving call from the highest mountain. The talented financial journalist — a classic pawn of the Fed — startled investors from the beaches on Long Island to the skyscrapers of Japan. After talking up extremely aggressive (rate hikes) action from the U.S. central bank for much of the last five weeks – Nick published a piece that pushed back against excessive rate hike expectations and suggested the Fed is not going to overcook the Porter House. An hour later, the BoJ (Bank of Japan) comes in and starts a massive forex intervention, pushing the yen up 3% in the span of an hour. Coincidence?“

The tag lines below the above graphic tell the simple but HUGE story of Friday morning:

- “Always, always… Always connect the dots. There are no coincidences. The Fed, the White House, the Wall Street Journal, and the Bank of Japan – were all working closely together on Friday morning.”

In case the message was not clear, the Inside Job article added a paragraph titled More Dots to Connect:

- “The Fed was put on notice from the highest levels – White House officials were knocking on Fed chair Powell´s door this week. They couldn’t get OPEC´s to help oil prices lower, to support the inflation fight. Now politically – the S&P MUST move higher ahead of the BIG DAY on November 8th. Midterm elections are won and lost in suburbs, where 401Ks are even more important than the price at the pump.”

Since a picture is worth many words:

- Lawrence McDonald@Convertbond – Oct 22 – NO coincidences on Friday – the White House wants equities running HIGHER in the precious 20 days heading into the midterm elections. See the important post above – a must-read.

In case some wonder why this past Friday was so important & timely – the Blackout for comments by the Fed began on Saturday October 22 because of the FOMC meeting on November 2. In other words, the article by the Wall Street journal that broadcast the Fed’s support for the Bank of Japan HAD to be PUBLISHED on Friday.

Of course, we have no clue whether the conjectures published by the Bear Traps Report in their Inside Job article are actually valid or not. We have a high degree of respect for their editor, Larry McDonald, & his sources. And much of what the Inside Job article wrote seems to meet the smell test and the eminently wise dictum about Truth being stranger than Fiction.

With all the above, how sweet was this past Week?

- Dow up 4.9%; S&P up 4.7%; NDX up 5.8%; RUT up 3.6%; DJT up 1.5%; Goldman up 8.5%; BAC up 10.4%; Apple up 6.7%; Amazon up 12.4%; Google up 5%; Microsoft up 6.3%; Netflix up 26.7%; Gold Miners up 7%; OIH up 15.1%; XLE up 8.3%; MOS up 14%; CLF up 13%; FCX up 17.8%; EEM up 2.3%; EWZ up 11.7%; EWY up 3.2%; EWG up 5.4%; Indian ETFs up 3%;

2. Treasury Rates

Remember the inverted yield curve hullabaloo? Yes, it is still inverted but much less so after Friday. With all this news about what the Fed might do, the 30-2 year curve steepened by 25 bps on Friday, the 30-3 yr curve by 26 bps & the 30-5 yr curve by 23 bps. On the week,

- 30-yr yield was up 36 bps; 20-yr yield up 30 bps; 10-yr yield up 21 bps; 7-yr yield up 13 bps; 5-yr up 8 bps; 3-yr up 1.2 bps; 2-yr yield down 2.5 bps; TLT down 4.8% & EDV down 8%.

What does next week bring? Remember the Fed is quiet and it looks like BoE & BoJ are not going to rock their boats. And positioning & liquidity are one-sided:

- Via The Market Ear – US 10 year – the shooting star? Haven’t seen such a big shooting car candle in a big asset in a long time. Let’s see how this develops from here, but these candles usually happen at the end of a strong trend and could be indicating a short term reversal in the making. One thing is sure, liquidity is horrible…

Technician Katie Stockton said on Wednesday October 19 that the 10-yr yield had an unconfirmed breakout on Friday, October 14 & that breakout would be confirmed with a close above 4% on Friday October 21. The 10-yr yield close at 4.21% and guess that breakout was confirmed. But for the near term Ms. Stockton sounded different:

- ” ..yet there are some signs of exhaustion based on our counter-trend signals for DeMark indicators; these are signals we haven’t seen since May-June ; it would suggest some corrective action in yields here in the near term, may be over the coming 2 months … so we do think that TLT trade makes sense; but keep in mind it is a counter-trend & anything counter-trend holds more risk .. “

Technician Mark Newton of FundStrat made an explicit connection between the rally in stocks & Treasury yields on Wednesday October 19 on CNBC:

- “… we also need to see rates starting to peak out before we can really think any sort of rally has some longevity … I am personally hopeful … my own work suggests rates are very close to peaking out … “

Lisa Shalett of Morgan Stanley went much farther on Friday on CNBC :

- “Morgan Stanley strategist Matt Hornbach thinks long rates are at a place where this is genuine value emerging & when you think of asymmetry of risk the idea that you can get coupons of 4%-4.5% in the bond market … if rates are done here, you get 4% coupon plus capital appreciation – that to us looks like a better bet than stocks – we are bond buyers here, that’s where the value is … “

Barry Banister of Stifel, a co-guest on the same CNBC show, is overall “optimistic that the worst is behind us & we could get about a 6-month rally here “. However he is worried about three macro factors – “Fed, Oil & diminishing liquidity in the Treasury market” and said:

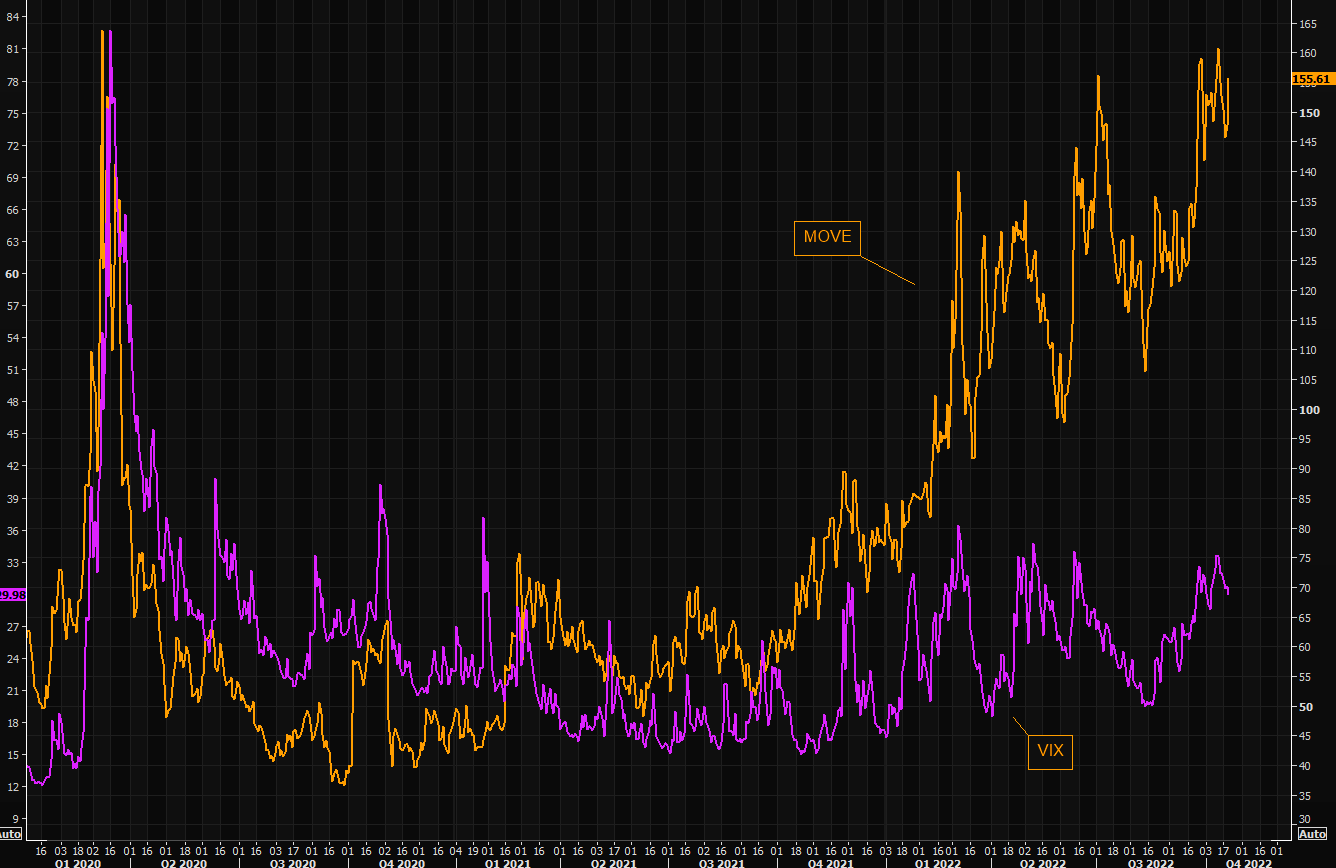

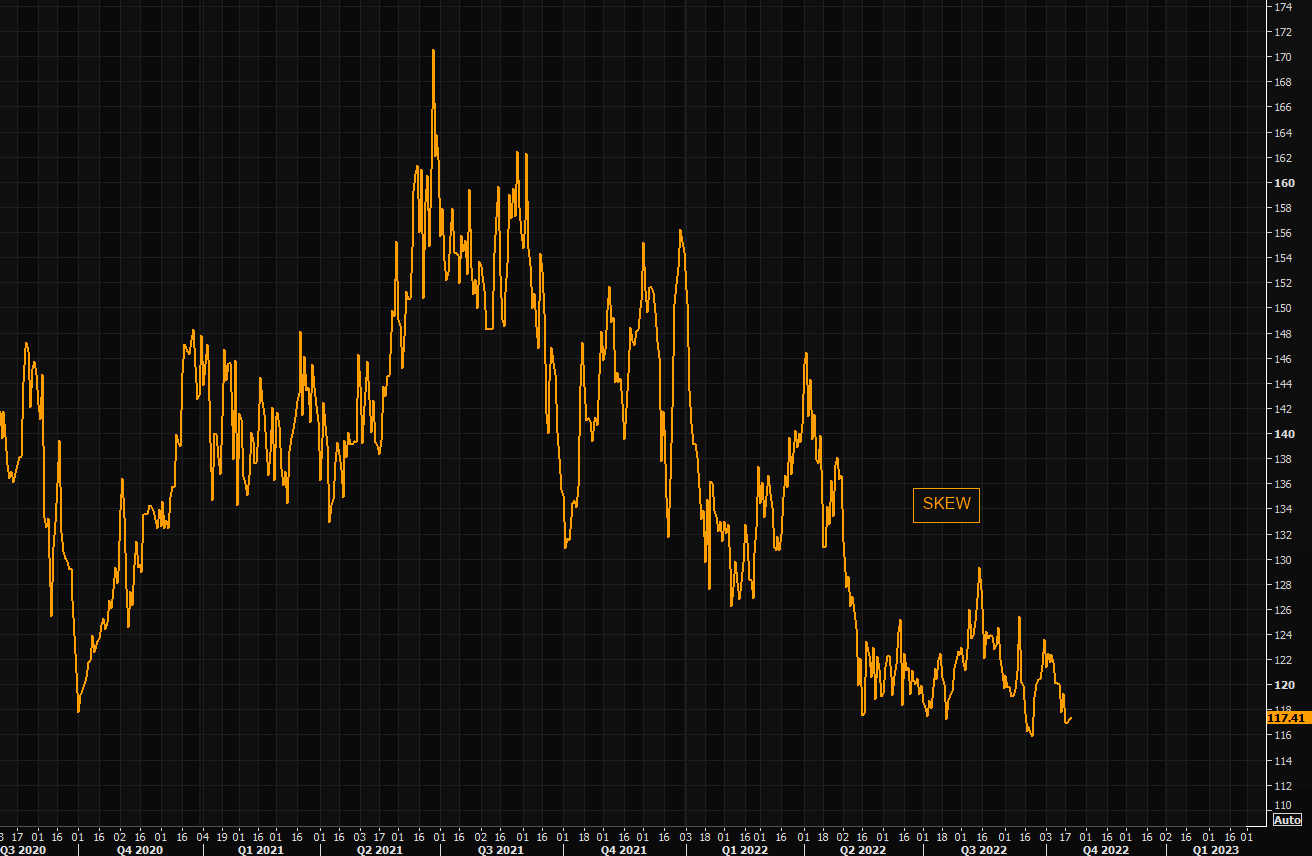

- “MOVE Index is way above VIX index of stock volatility... if that gets problematic, stocks will go down … so we really need a Fed pause; QT is something we are watching … ”

How about a picture?

- Via The Market Ear – Thursday – MOVE moving again – Bond volatility, MOVE, simply refuses moving lower. Will we take out the most recent highs around 160? The “classical” gap vs VIX is huge. At these levels of MOVE the market is pricing approx. 10 bps moves in yields.

But what about QT from Central Banks?

- Via The Market Ear – Wednesday – Hiking stops, QT continues – Even if central banks stop hiking, there might be continued pressure from QT...

3. Stocks

As the lead, we got to go with the one who brung us to this rally:

- Dan Niles@DanielTNiles – – Most important factor for S&P this yr & future GDP growth is actions taken by the Fed to battle inflation. Investors want a reason to believe this is THE bottom & a less aggressive Fed on 11/3 is arguably at the top of that list. Still believe bear mkt rally but long either way.

Here is one estimate of future gains of S&P 500 albeit with a tiny sample:

- SentimenTrader@sentimentrader – – The S&P 500’s minimum gain on an up day over the past month is 2% (rounded). Here is every other occurrence and the S&P’s return a year later: March 18, 2020: +63.3% July 28, 1932: +81.7% April 19, 1932: +40.3% h/t @michaelsantoli

Isn’t it comforting to see fundamental leadership lead a rally despite weak fundamentals?

- Bespoke@bespokeinvest – Oct 21 – Semis $SMH now up 7% on the week vs. +4.3% for $SPY.

Since Nasdaq is usually led by Semis,

- Via The Market Ear – Friday – NASDAQ – will you? NASDAQ is flirting with the negative trend line that has been in place since mid August highs. Note we are above the 21 day moving average. We haven’t closed above it since mid August. A close slightly higher and things could become very squeezy. Note the positive RSI divergence…

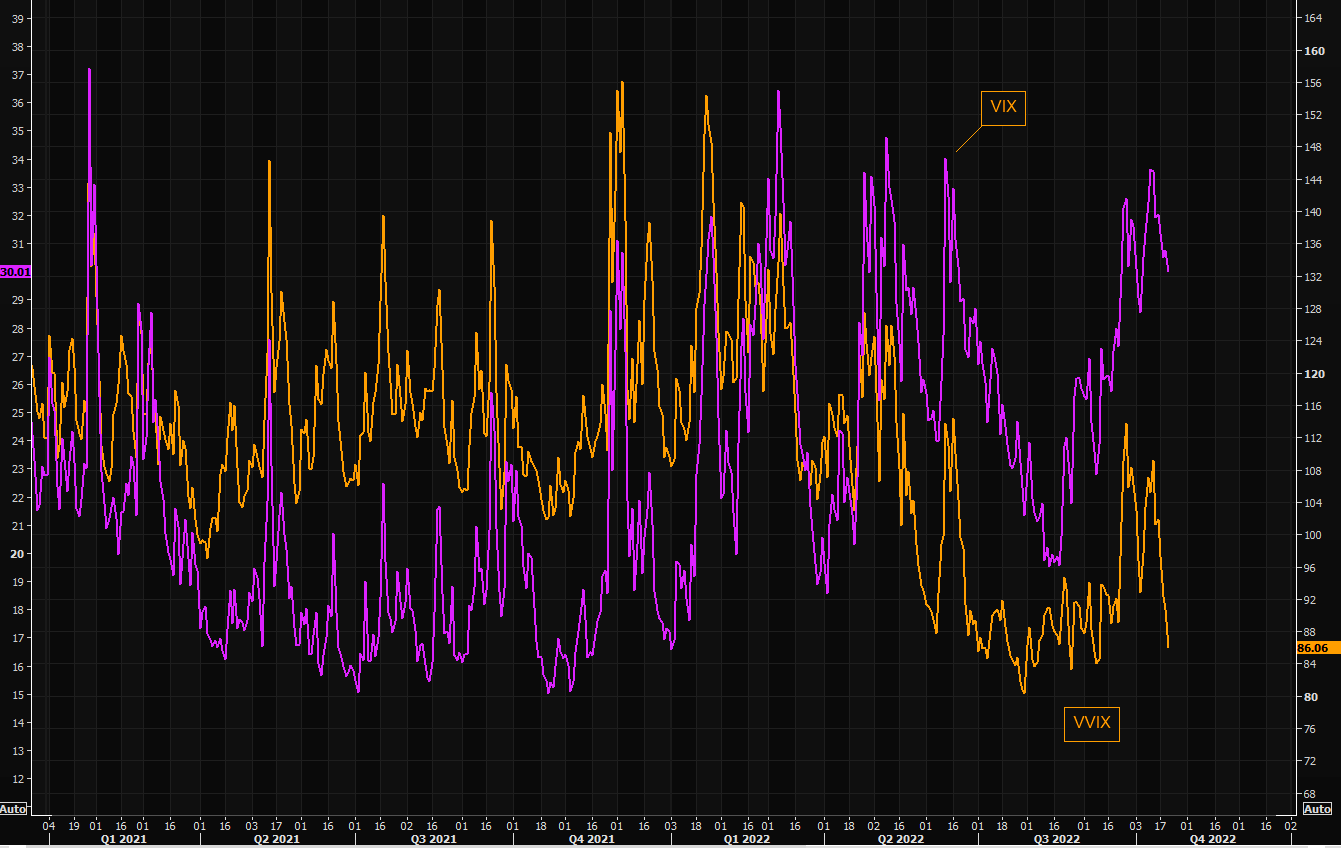

Look at the MOVE vs. VIX chart from Section 2 above. It asks what happens if MOVE dragged VIX up. We can’t help wondering if these Fed rumors are correct or these smart technicians like Newton-Stockton are correct about rates peaking, then wouldn’t MOVE move lower? And in that case, wouldn’t VIX go lower still? On that note, is there anything that might drag VIX lower?

- Via Market Ear – Thursday – Remember VVIX? It has crashed once again. Time to “drag” VIX lower with it?

Man, just imagine if MOVE falls, puts downward pressure on VIX while VVIX drags VIX lower with its power? Could it VIX fall below 25 then or even go to 20? Happy Days would be here again.

But is there a group that might absolutely cry if VIX falls to 25?

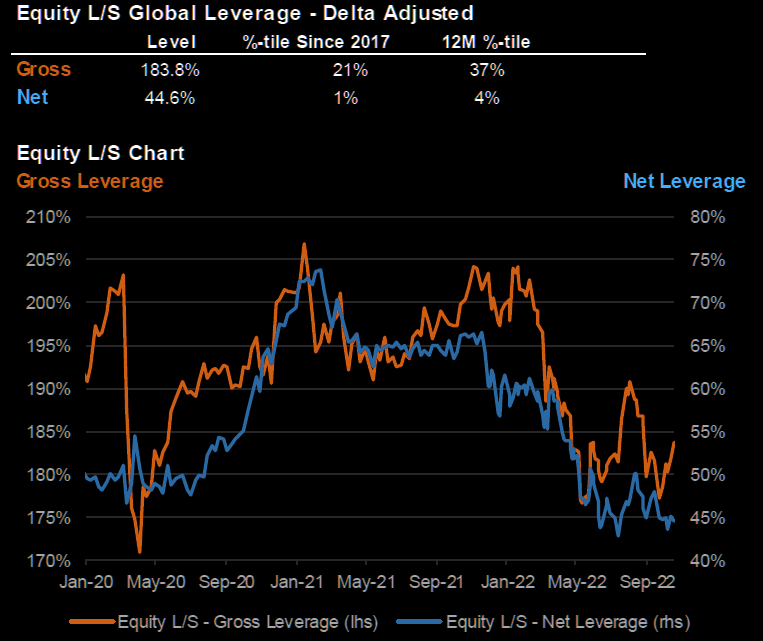

- Via The Market Ear – Thursday – Hedge fund net leverage back at lows – But is has been in the 45-50% range since May. Does it really matter? As someone smart said, the real pain trade is ALWAYS to the downside

Couldn’t they buy upside calls to get longer fast? But are those calls cheap?

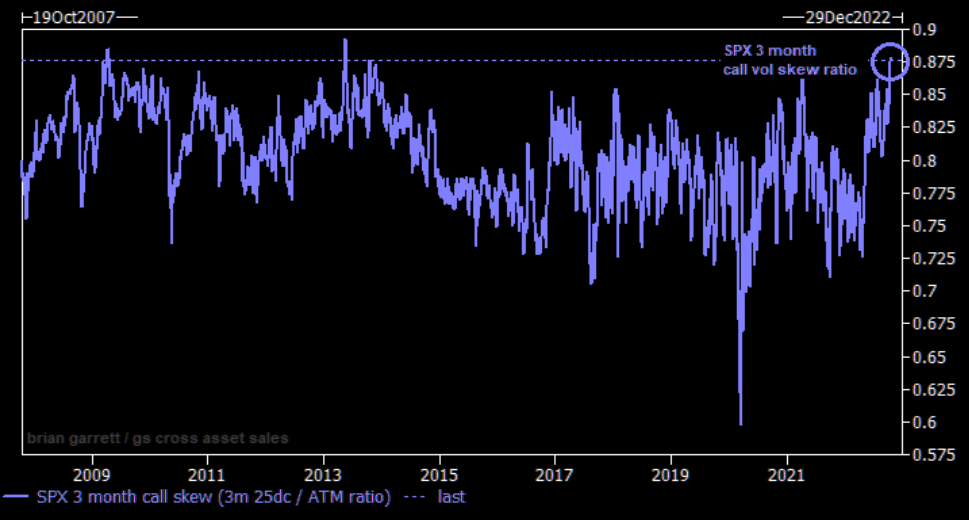

- Via The Market Ear – Friday – The upside crash hedge ain’t cheap – Great chart via Goldman’s derivatives guru Brian Garrett showing just how expensive upside “protection” has become. SPX upside calls have never been more expensive, talking in volatility terms. If you believe in markets being boring for longer, overwriting makes a lot of sense.

But how does “overwriting” make any sense to those who are short? On the other hand, are any shorts left with today’s low VIX?

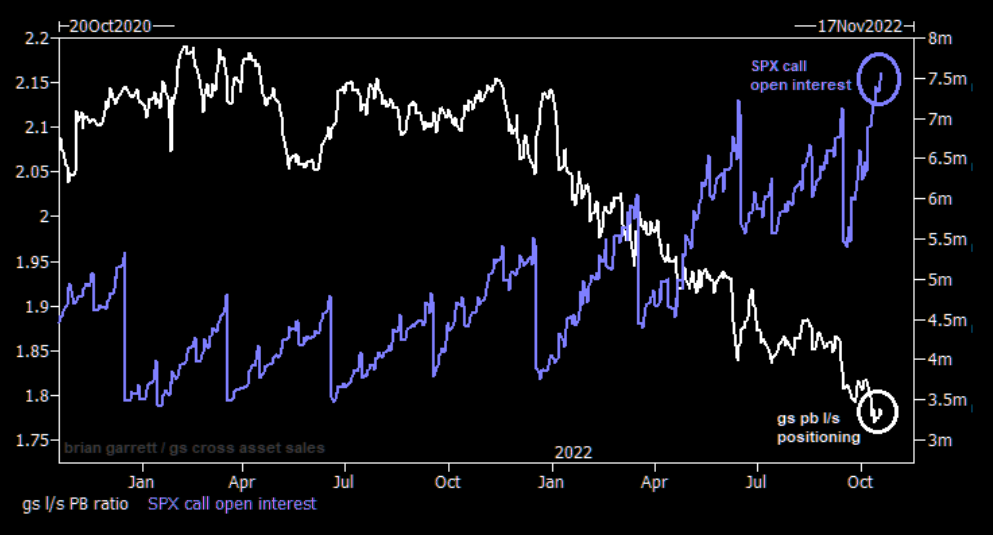

- Via The Market Ear – The crowd is short – Once again, the crowd is short via delta 1 products. This trend has been going on for some time. This is part of the reason SKEW index has continued to decline as people do not buy downside protection. Instead, they have been “forced” to cover the possible upside risks via buying calls. First chart showing GS PB long/short ratio vs SPX open interest (calls). Second shows the crashed SKEW index.

Given the ebullient tone of this section, some might wonder about the amount of single malt imbued while writing it. Without commenting on that, we might point out that we do believe in views seen from shoulders of giants, in this case Micah Wilson, Dan Niles et al.

But note all of the above is at the mercy of BoJ, ECB & of course our esteemed Fed. Fortunately UK seems as if sanity has been regained. But if Monday opens with the BoJ doing something un-BoJ like or ECB-EU torpedoing the Euro, then all the downward positioning might look genius-like at the cost of many who are going with those who brung them. A healthy collection of 50-cent puts is always a low-cost protection.

4. Can love be slimy?

An old poem talks about a beautiful lotus that is born& bred in slime. That simile was used to describe a young woman dressed in rags of leaves. The message was that the really beautiful look that way regardless of their coverings.

We thought of the poem (from about 370 CE) when we began hearing & reading about the outpouring of love for oil stocks this week. First it was a normally prosaic Mark Newton saying on CNBC:

- “OIH, the Oil Services ETF that actually broke out against XLE & XOP, ahead of today’s announcement about Oil; Energy continues to act fantastic; WTI crude declined 10% in 10 days but energy has been outperforming the S&P; its a great sector to be in; shown very little weakness whatsoever; my own cycle suggests crude is bottoming; I think energy is still a great place to be; Services stocks look little more interesting – drilling companies like HAL & SLB ; So I like OIH; energy is still a good bet … “

Then a tweet from Larry McDonald:

- Lawrence McDonald@Convertbond – Oct 22 – % of the S&P 500 – Energy Oil and Gas Sector 2022: near 7% 2020: near 2% *here come the bulls.

On the other hand, are we seeing over-investment sweep into the energy sector? No says Sanford Bernstein:

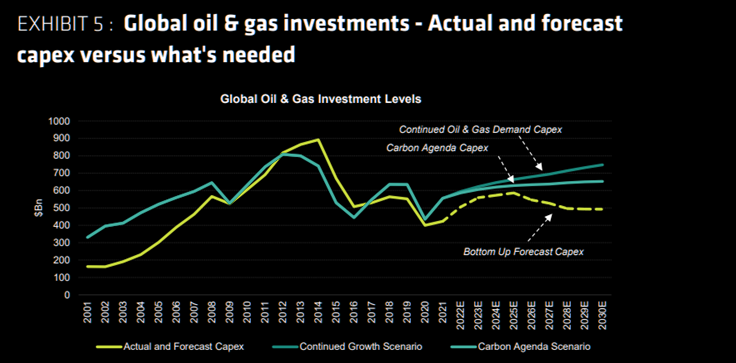

- Via The Market Ear – Friday – Just how much are we underinvesting in oil & gas? – Sanford Bernstein looks at the scale of the problem of underinvestment in energy capex. The conclusion is that we are underinvesting significantly. To meet the reduced Carbon Agenda scenario of managed decline, capex will need to rise by at least 20% on average from here to 2030. To meet 1% CAGR global oil & gas demand to 2030 then capex would need to be 30% higher on average from here to 2030 and 40% in the second half of the decade.

*the poem we referenced above is from Shaakuntal – the exquisite play of Kaalidaas- the greatest poet in the known history of the world. Goethe never read the Sanskrut original but when he read the translation, he reportedly put the book on his head & danced around his reading room in joy.

5. Happy Deepavali to All

The 5-day festival of Deepavali (Diwali – row of lights) began this weekend. And the ancient city of Ayodhya, the city of Bhagvaan Sri Raam’s return, was decked in a wave of lights on both banks of the Saryu River.

A small version of this is & will be seen in every household in the world that celebrates Deepavli & the victory of Good Light over the Darkness Evil.

स्वस्ति अस्तु भवतु – Let Svasti be with You

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter