Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Wave!

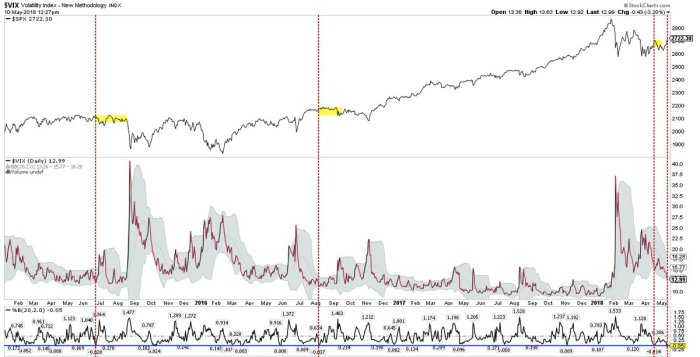

What an amazing week this turned out to be! From the low of 2599 on Thursday, May 3, the S&P rallied 129 handles to close this week at 2728. The Dow closed up on 7 straight days and the VIX closed below 13 on Friday. There was nothing fundamental about this move. Yes, data like NFP or CPI may have soothed some nerves but that data had virtually nothing to do with what happened this week. Based on our previous stays in Texas, we are tempted to call this rally a stampede. But that would be doing injustice to the move.

Smart people who understand Complexity Theory tell us that markets are complex like climate phenomena. We recall Tom McClellan discussing the concept of a rogue wave in the stock market. As we wrote last week, the rally from 2599 to virtually unchanged on Thursday, May 3, was mega-impressive. It was sudden, powerful & engulfing just like a rogue wave. And it reminded us last week of the similar bullish wave that hit around 11:30 am on Friday, September 21, 2001.

That wave carried the SPX from 945 on Thursday, May 3, to 1,071 on October 5, 2001 – a rally of 126 handles. In contrast, this week’s 129 handle wave took only 7 trading days. That should suggest a cresting of this wave fairly soon. Some indicators do suggest such a short term topping condition:

- Urban Carmel? @ukarlewitz Thu May 10 –Urban Carmel Retweeted Steve Deppe –

$Vix lower BB and$SPX upper BB. Within 5 days,$SPX closed lower at least once 81% of instances (chop or retrace).$SPX closed higher on Day 10 or Day 20 in 86% instances (higher high ahead)

The September-November 2001 wave behaved similarly. From 1071 on 10/5/2001, it rose to 1142 on 11/15/2001 & then to 1170 on 12/5/2017, for a total rally of 225 handles. If this wave gives us a rally of 225 handles, that would mean 2824 on SPX in the August time frame, just in time for a pause or decline into the November 2018 election.

We, of course, have no idea what will happen from here but we do think, based on the power of this week’s wave, that higher S&P levels are ahead. That, as we saw last week, is the view of strategists & quants like Mike Wilson, Tony Dwyer & Marko Kolanovic.

Having said that, what indicators are suggesting a short term consolidation or decline?

- Helene Meisler? @hmeisler – Equity put/call ratio 51

And,

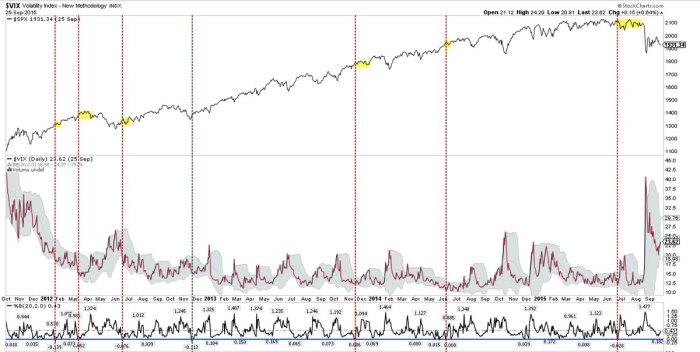

- Urban Carmel? @ukarlewitz – Instances where

$VIX closed under its lower Bollinger, since 2012.$SPX in upper panel

A better visual case was made in:

A better visual case was made in:

- Todd Harrison?Verified account @todd_harrison – I get the whole ‘past performance no guarantee of future results’ thing but Déjà vu.

$SPX

In this spirit, Carter Worth of CNBC Options Action said on Friday that he expects this rally to fail & a possible target was the mid-point of his channel or a decline of 15% in S&P from peak to trough. That fits with:

In this spirit, Carter Worth of CNBC Options Action said on Friday that he expects this rally to fail & a possible target was the mid-point of his channel or a decline of 15% in S&P from peak to trough. That fits with:

- Thomas Thornton? @TommyThornton I’m at my highest net short position since January- Hedge Fund Telemetry

On the other hand,, Tony Dwyer showed an extreme level of 14-week capitulation chart and said the median rally from such a condition measured 14% in 7 months. That fits with:

- Peter Brandt?Verified account @PeterLBrandt – Dear Elliott Wave 3rd of a 3rd of a 3rd crowd: Classical charting principles flashed buy signal in Nasdaq today. Next stop could be 7775.

$NQ_F$QQQ

Wouldn’t it be interesting to see a decline sometime next week just to scare some chasers? A weekly close in VIX below 13 is just the right sort of trigger for that and it is quite common to see one hard down day during Options Expiration week.

2. Rates

The US Stock Market may be seeing massive waves but the Treasury market remains calm & undisturbed. It is as if it has found its perfect level. It doesn’t break out above its big levels of 3.22% on 30-year & 3.03% on 10-year. It doesn’t go much below those levels either.

But it is not unmoved. Instead, the curve is steadily flattening. The 10-year closed the week at 2.97%, 6 bps below its big 3.03% level. But the 30-year closed the week at 3.10%, 12 bps below its 3.22% big level. So the 30-10 year spread closed at 13 bps, a decline of 4 bps on the week.

Actually, the entire curve is being flattened. The 10-5 year spread flattened by 3 bps this week meaning the 30-5 year curve flattened by a whopping 7 bps on the week. And this is after the largest 30-year auction ever, according to Rick Santelli. Where is the concern about the increased supply or the much discussed rise in inflation expectations?

But none of this is shaking the rock hard resolve of Bears who have amassed the largest short position in Treasuries. Read what Gundlach said about this (via Bloomberg):

- “This is kind of mind-blowing that we can’t get a rally off of this type of speculative short in the Treasury bond market,” Gundlach, DoubleLine’s chief investment officer, said in a webcast. “You almost always get a rally,” he said, “but now we’re just going sideways. So for the bulls of the world, this is not really all that corroborative.”

This enabled George Goncalves of Nomura to utter an investment heresy:

- “What makes this time different is that the Fed is far along away from zero and there’s more conviction now that they’re not going to blink, … You also feel better about holding a short when there’s a ton of paper coming in down the road.”

3. Commodities

They are flying, aren’t they? At least a few of them are:

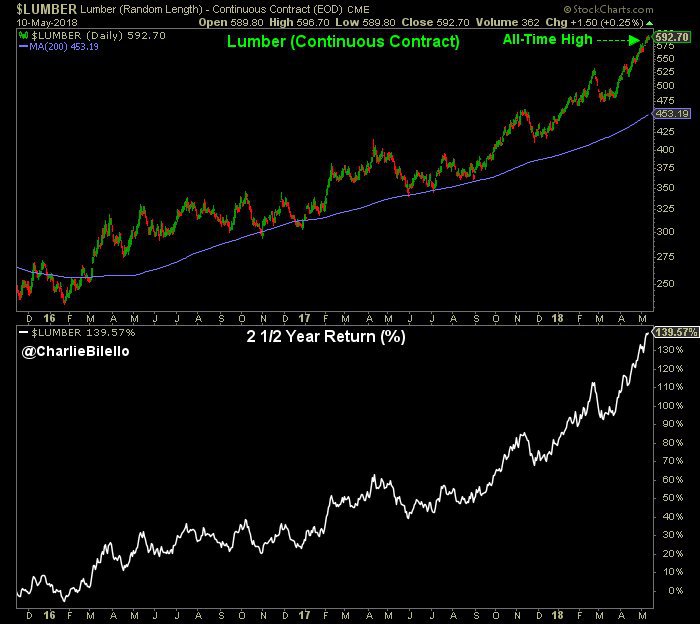

- Charlie Bilello?Verified account @charliebilello – Thu – Lumber continues to hit new all-time highs, up 140% in the last 2 and a half years. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2604248 …

And,

And,

- Charlie Bilello?Verified account @charliebilello – Crude Oil closes at a 41-month high, up 161% from its 2016 low.

$WTIC

Remember the Gundlach tenet? That a big rally in Commodities precedes the onset of recession and, possibly, the commodity rally & the Fed’s efforts to cool it via rate hikes end up triggering a recession. Is that happening before our eyes? Just look at the inexorable rally in the 2-year yield.

Remember the Gundlach tenet? That a big rally in Commodities precedes the onset of recession and, possibly, the commodity rally & the Fed’s efforts to cool it via rate hikes end up triggering a recession. Is that happening before our eyes? Just look at the inexorable rally in the 2-year yield.

In the mean time,

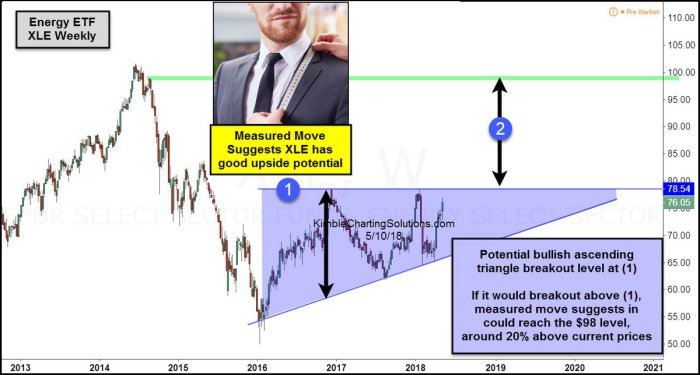

- Chris Kimble? @KimbleCharting Energy ETF has good upside potential breakout from bullish ascending triangle takes place, possible 20% upside.

$XLE$USO$SPY$XOM

4. Gold & Silver

Of course, these are commodities too. But they are behaving very differently than Lumber & Crude. May be, there is a lesson in that:

- J.C. Parets? @allstarcharts – one thing I think is getting ignored about this recent US Dollar snap back rally is how well precious metals held up. To me, that argues for overwhelming strength in Gold & Silver on the next Dollar sell-off

$GLD$SLV$GC_F$SI_F

Above said “overwhelming”, below says “huge”.

- fred hickey? @htsfhickey – One very interesting detail in today’s COT report for gold. Managed Money (mostly hedge funds) longs taken down to 109.5K contracts-lowest since early 2016 when gold bottomed ($1050). At 2016 gold peak over 300K longs ,2017 peak nearly 270K longs. Huge potential buying pressure

Silver was 1.1% vs. Gold being up 35 bps.

- Chris Kimble? @KimbleCharting Silver- The end is near with bullish sentiment near lower levels of the past few years.

5. “stop the fight” or “just where we want them” ?

Walmart pulled out one win this week over Amazon. Amazon, the #2 eCommerce site in India, was trying to buy Flipcart, the #1 eCommerce site (Doesn’t India have Anti-Trust laws?). Walmart beat them to it.

Walmart pulled out one win this week over Amazon. Amazon, the #2 eCommerce site in India, was trying to buy Flipcart, the #1 eCommerce site (Doesn’t India have Anti-Trust laws?). Walmart beat them to it.

- StockTwits?Verified account @StockTwits May 9 – Walmart

$WMT now owns 77% of Flipkart. They paid $16 billion and here’s what they’re getting: – 100 million registered users – 10 mln daily website visits – Catalog of 8 million products sold in India – Controlling stake in India’s biggest eCommerce co

Enough has been written & discussed about this acquisition. The market hated the idea & took more than the $16 billion they paid out of Walmart’s market cap. Were the markets wrong?

Flipcart is already #1 in India. Secondly they have big partners like Microsoft, Softbank & possibly Google in Flipkart. So Walmart doesn’t have to move resources from US to India. Also,

- You can’t be a major media company without a big presence in India. That is one reason both Disney & Comcast are fighting for Star, Fox’s #1 network in India. Netflix & Amazon are furiously adding Indian films & created Indian content to their offerings in India. Very soon, it will become equally obvious to all that a retail company can’t be really global without a big presence in India, a country where people shop more voraciously than America.

- Success in retailing is similar to success in elections in India. The poor are far more committed to voting in India and vote in far larger percentages & numbers than affluent Indians. The entire India story is the increase in disposable incomes of the huge mass of poor & lower middle class. The rich Indian class is too small to register on a global scale.

- Based on our checks, no one we know among the executive or upper middle class professional segment uses Flipkart. If & when they buy online, they buy from Amazon. However, those we know in the lower middle class, cab drivers, household help etc, have not even heard of Amazon. They have been buying from Flipkart & continue to do so. They have the least amount of free time to go out & shop. Their children are web-smart and their families buy everything they can from Flipkart, especially after they added means for recurring payment (a feature offered by FastSpring amongst others). If Flipkart retains this group, then their market share will only increase. They already have the physical distribution to reach villages & small towns.

- This customer base of Flipkart is similar to Walmart’s customer base in America while Amazon’s base in India is similar to Amazon’s customer base in America. The difference is that Amazon’s base is widening demographically in America while Flipkart-Walmart’s customer base India is widening demographically in India.

- If Google joins & throws in the large gmail user base in India behind Flipkart-Walmart, then that would be a big competitive advantage. Customers can see Flipkart-Walmart ads while writing-reading emails &, perhaps, buy seamlessly. Netflix can join this partnership and use that to broaden Flipkart’s offerings to compete effectively with Amazon Prime Videos. Netflix is just beginning to ramp up in India and so, joining with FlipKart & its many partners, may be a fast& cost-effective way to get scale.

We are simple folks & we tend to think simply. The above all are our quick thoughts. We do think Walmart has a great opportunity to beat Amazon in India and with India they also get penetration into the large Indian diaspora in the Middle East. That is if they execute correctly without forcing Flipkart to become Walmart.

6. “give me some reinforcement pls“

Last week we speculated about how President Trump would campaign to maintain & even increase the Republican majorities in the Senate and the House. Now we know. What do we know & did the Kentucky Derby provide an omen? Find out from our adjacent article – Reinforcements Please, American Pharoah & Now Justify.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter