Editor’s Note: In this series of articles, we include important or interesting tweets, articles, videoclips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “I think it is nervous time”

So said David Tepper and everybody got nervous. And rightly so. If there is one man who is associated with understanding how Fed QE leads to stock market rallies, it is David Tepper. According to CNBC’s Kate Kelly,

- “he talked about Central Banks in China, the ECB as well, policy too tight in ECB especially. looking for an easing event in he thinks it might be overdue. June – it needs to happen now or risk being ineffective. He thinks U.S. growth has been too slow. He thinks there’s a risk of falling into deflation, much more so than inflation, and he thinks in general too much leverage in the system. speaking of sort of earnings and the stock market climate in the u.s., he said growth is slower. you’re going to have lower profits.

But as Kate Kelly pointed out, Tepper has positioned his fund to take quick advantage of a major move, either up or down. His simple statement is “I’m not saying go short, just don’t be too freaking long“. Absolutely straight sound talk, the kind we like. While CNBC did a decent job summarizing Tepper, a more detailed and interesting read about him is The Apotheosis of David Tepper by Joshua Brown, a CNBC FM trader.

2. Meltdown in Treasury Yields

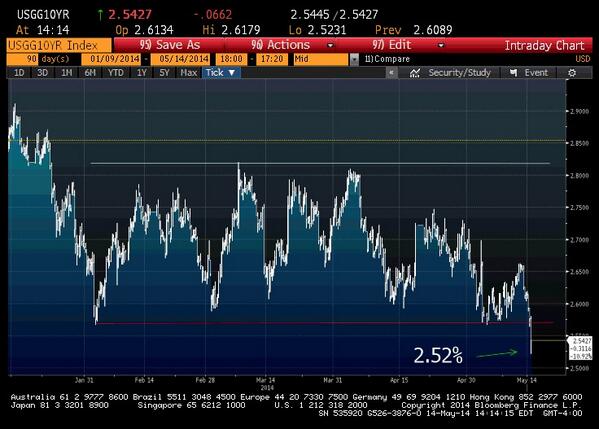

It began on Tuesday, accelerated hard on Wednesday and continued on Thursday morning. The “It” was the waterfall in Treasury yields. Everybody began talking about it on Wednesday,

- Bespoke @bespokeinvest – At 3%, everyone thought the 10-year was going to 3.5%. Now that it’s at 2.5%, everyone seems to think it’s going to 2%.

It absolutely smelled like a panicked liquidation of Treasury shorts. That persuaded a few Treasury bulls to sell some,

- Thursday – Michael A. Gayed,CFA @pensionpartners – “Treasuries now may finally be vulnerable“.

- Thursday – Keith McCullough @KeithMcCullough – “If you’re mucho long $TLT $TIP $BND alongside our Early Look product, book some here“

- Wednesday – Lawrence McDonald @Convertbond – “US 10s got down to 2.52%, feels like a short term capitulation washout for shorts, good place for longs to lighten” pic.twitter.com/n0o2ObLtOG

Larry McDonald elaborated on Wednesday afternoon on CNBC Closing Bell:

- “I think it’s a capitulation moment for people that are short treasuries. … Now now is the time to go the other way, Sell bonds. Everybody that’s caught short is getting carted out; TBT for example; we have a capitulation model that measures pain, really, and the amount of pain that’s in the TBT, … the amount of shorts getting carted out in trades is very, very high right now“

He emphasized this call in his Bear Traps report on Thursday morning. Others like Jim Bianco expressed the opposite opinion on CNBC Closing Bell on Wednesday afternoon:

- “I think that this capitulation trade we’re going to see now is a lot larger than people think. bonds, yields can fall a lot more before this is over with.”

When asked by CNBC’s Bill Griffeth, Bianco said the 10-year yield can drop to low 2s. Rick Santelli thought this was too timid and gave his target on Thursday afternoon:

- “I think there is a 60% chance that we could see low 2s. I think there is 40% chance we could see 1.60%“

- “I think look no further than Europe. They’ve managed to put rates for countries whose economies are still highly questionable well below levels of true value. … We saw the Southern European yields pop up 16, 18 basis points against a six-basis point drop in Bunds. That means those spreads widen close to 25 basis points. That is risk.”

What Santelli was alluding to was echoed in a way by Market Anthropology on Friday:

- “This week, 10-year yields continued to move lower against the consensus, although we did notice anecdotally that many participants were quick to comment and weigh its context that the move was already over-extended. While from a short-term perspective this may well be true, with respect to what we see across our own research – it has considerable room to run and its effects are just beginning to influence other markets. Moreover, the very real risk of creating a negative feedback loop in yields is present“

And what David Tepper articulated as a question, Rick Santelli said as a statement – It all depends on Draghi. If he doesn’t act soon and hard, it may be too late. Santelli called his actions as “temporary stability leading to longer-term volatility” – a different way of saying “Serenity now, Insanity later“. An

d if that insanity hits, then Santelli & Gundlach could be right and the 10-year could make a new all-time low in yield.

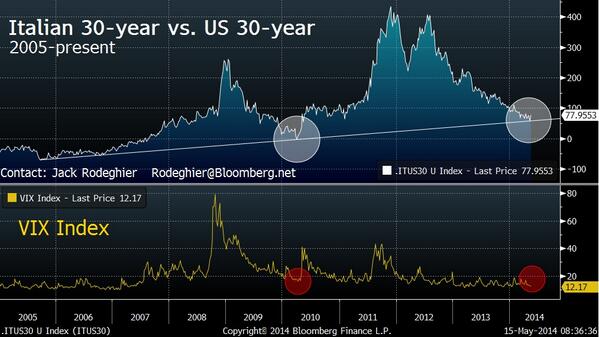

A similar point was made graphically in:

- Thursday – Jack Rodeghier @glarustrading – Italy vs USA 30yr spd (&VIX), held ’06-’10 trend-line, mean reversion commencing? # of known unknowns on the horizon pic.twitter.com/VOCPZgewi1

But what about simple trend line resistance?

- Thursday – Helene Meisler @hmeisler: Watching this line $TLT pic.twitter.com/jC3D9uCH4l

What happens when a major trend line gets crossed? And what yield level on 10-year is important? A fixed income guest (unnamed & unquoted in the CNBC Closing Bell clip) said, as we recall, that “2.40% is a huge level for the 10-year and if that breaks, the next support is 2.10%-2.05%. “.

But where can Treasury yields go over the intermediate term? The most important determinant of that is the neutral Federal Funds rate in the next up cycle. If that rate is 5.25%, as it was in 2006, then the 10-year yield could go much higher than where it is now. This brings us to Bill Gross and Tony Crescenzi of Pimco:

- Gross on BTV Market Makers on Wednesday – “the new neutral policy rate is not 4%; it is about 2%; … the 2% rate is a cap not a target”

- Crescenzi on CNBC Street Signs on Friday – “the policy rate, the Fed Funds rate, the rate the Fed controls will go to 2% in the future rather than the old 4%. In England, the Bank of England governor, Mark Carney, is saying it will go to 3% vs. the old 5%; it [FF rate] went to 5.25% in 2006 & 6.5% in 1995. expect nothing like it. Markets, though, still are expecting something like it, and that’s part of the thesis that markets can be more stable as a result”

This is huge if it turns out to be true. Speaking strictly from our usually unreliable recollection, the 10-2 year spread is normally at 100 bps and the 30-10 year spread ranges between 50-100 bps at extremes. So if the 2-year rate is 2% (at cap, the 2 year usually sits atop the FF rate), then the normal or higher range of the 10-year would be 3% and the 30-year between 3.5%-4%.

In other words, the top of the yield ranges near the high of the next up cycle would be where yields were already on December 31, 2013? That would change the risk-reward calculations of holding long maturity Treasuries from here into the top of the next cycle, wouldn’t it? And what would it say about the intermediate term growth prospects of the U.S. economy? Wouldn’t Draghi have to make a major mistake and push Europe into deflation for that to happen? Of course, Pimco could prove to be terribly wrong and we could all enjoy a resumption of growth in the second half of 2014 and well into 2015-2016 with peak yields near 5% as in 2006.

Had the RS-DS combo (Ruhle-Schatzker of BTV & Drury-Sullivan of CNBC) asked these questions of Gross-Crescenzi, we wouldn’t have been caught in the tailspin of our own imagination, would we?

3. U.S Equities – Guru Clips

Thanks to CNBC’s coverage of the SALT conference, we heard from several hedge fund managers this week:

3.1 Leon Cooperman on Thursday on CNBC FM 1/2 –

- “the entire debate about the market centers around what is the right multiple for the earnings we’re seeing, because earnings are growing very modestly and the leverage is in the multiple. … you take 16 times 1 $117 earnings estimate — sorry if i sound like a statistician, which I’m not — 16 times $117 is 1,872. the market ended 2013 at 1,848, a fair evaluation“

- “conditions that would lead to a bear market are just not present and that the market’s in its own fair evaluation … I don’t believe it will go below 1,700 and I don’t think we get above 2,000“

- “because we have about 15%-20% of our portfolio in structured credit. My structured credit team is doing a fabulous job. they’re doing better than i am in the equity market. they’re up about 6% todate. they’re adding to our portfolio returns. we’re paying our brokers 70 basis points a year for money, and we’re ending 1% a month in structured credit. We don’t have much cash. we’re reasonably fully invested but we have a lot of borrowing capacity, because we have no leverage“

3.2 Steve Kuhn on Thursday on CNBC FM 1/2 –

- “I think it’s interesting when markets don’t actually talk to each other. and today, I think if you look at the fixed income market versus the equity market, it’s as if they live in two different worlds. the 10-year treasury with a yield below 2.50, you could put that into stocks and say it’s trading within a p/e of 40. That’s a little too low. the contrast is we love stocks that are incredibly boring. I can give you portfolio stocks where the earnings are so stable they might as well be bonds that have PE of 12-14. compare that to the 10 year Treasury of pe of 40 and I think you will win on that trade the vast majority of time. You might lose in a week or month or year but not over five or ten years. Those stocks will outperform. “

3.3 Ralph Acampora on CNBC Futures Now on Thursday –

- On “Futures Now,” Acampora predicted that the S&P 500 would drop “10, maybe 15 percent between now and maybe October,” but said it would be much worse for small caps, mid-caps and tech stocks.

- “If you ask me about the Russell and the Nasdaq Composite and the S&P MidCap, I think you’re talking about 20, 25 percent. And I call it a stealth bear market going on.“

- “The last time I saw anything like this was in 1994, when the Dow and the S&P were in

a 10 percent trading range all year, and then under the surface they were just ripping them apart. I have a sick feeling that we might be doing that again,”. - That said, after equities decline into fall, Acampora believes the fourth quarter “will be very, very strong.”

3.4 Lawrence McMillan on Friday:

- “It is hard to imagine a market any more perverse than this one. … In summary, the market is back within its trading range, awaiting a breakout. I can’t really imagine a less overbought condition than there was when $SPX made new highs last Monday, and yet there was no follow-through. So, the trading range appears to be the order of the day for the foreseeable future“

3.5 Tom McClellan in Crude Oil Says DJIA Should Trend Higher

- “Four years ago I wrote about crude oil’s 10-year leading indication for the movements of the DJIA. … I do not have a good enough explanation for why the two should have this relationship, but after 120 years of data, I figure it is a solid enough phenomenon to trust somewhat, even if I cannot understand its basis.”

- “10 years ago in 2004, crude oil prices were engaged in a steady and exceedingly linear uptrend. The DJIA appears now to be replicating that action, thanks in part to the liquidity supplied by the Fed, and thanks also to investors’ fading memories of the ugliness of the 2007-09 bear market”

4. U.S. Equities – Interesting Tweets

Generally speaking, the tweets & article excerpts below follow a bearish to bullish progression. Remember these are simply a random collection of tweets & articles that caught our eye. So, Caveat Reader

- “Although still low by historical standards, we continue to work from the perspective that by the end of 2013, 10-year yields became stretched to a relative extreme and were marking the top of a prospective long-term range between 1.5% and 3.0%“.

- “Unlike its secular exhaustion peak in 1981 characterized by a relatively swift pivot lower, 10-year yields have been making a process top with the broader equity market structure expressed in the SPX. While higher beta indexes as well as the yield dependent financial sector have been more closely correlated with the eroding yield backdrop in the market, we still expect the SPX to eventually follow suit and complete a cyclical top this year.

Michael Gayed in MarketWatch

- “In a paper I recently co-authored with my colleague Charlie Bilello, we show that going back to 1977, strengthening long-duration Treasurys tend to precede periods of higher volatility for the stock market. We have not seen that yet, but are we about to?”

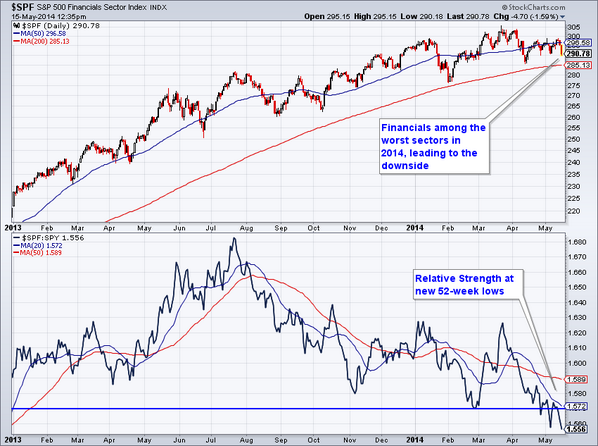

Charlie Bilello, CMT @MktOutperform on Friday –

- Financials don’t have to lead for the market to go higher, but you never want to see them among the worst sectors. pic.twitter.com/aMWYF1BRk8

Charlie Bilello, CMT @MktOutperform on Friday

- The $SPX was able to make a marginal new high, but high yield spreads could not make a new low this week, red flag. pic.twitter.com/MK0priDW5K

Traderxaspen @traderxaspen on Thursday

- “Remember in last five years of this bull mkt the end of May June and August have been the weakest times in the equities mkt“

J.C. Parets @allstarcharts on Wednesday

- “I think the stock market is about to get destroyed. I m a weight of the evidence guy. We’ll see“

Nick @NicholasOC Protected Tweets on Friday

- “$NDX Bollinger’s tightening, triangle terminating. Next week is decision time” pic.twitter.com/ECVN85kl2U

Urban Carmel @ukarlewitz on Friday

- The consensus equity short is at a 7-mo high today. $EEM pic.twitter.com/UwK10LXHMl

Vconomics @Vconomics on Thursday

- “Keep an eye on $IWM (versus the S&P). It could rally 6% if today’s support (yellow trendline) holds“. pic.twitter.com/LVuK4X6Cpd

5. Indian Stock Market

“Mama Mia” is how a Bollywood song would describe this week’s rally in the Indian Stock market. Yes, Bollywood did produce a movie called “Nadaan Ladkiyaan” (“Wild & Crazy Girls”) that has a song that goes Mama Mia . And of course, the American musical Mama Mia was described as America’s First Bollywood Musical in a Huffington Post article.

Whatever you call it, it was a crazy rally and those who presumably called it in March celebrated on Friday morning:

- Charlie Bilello, CMT @MktOutperform – The breakout no one was talking about in March (India) is starting to catch people’s attention investorplace.com/2014/03/india-icn-ifn-spy-xbi/#.U3YZqPldWyg … pic.twitter.com/aeLDYR5hUz

Mr. Biello’s article in investorplace.com is bullish on India and discusses the chart below of IFN, an India closed end fund.

And amazingly, IFN still trades at a 9% discount to its NAV. But IFN is also up 9% this week and up 24% ytd. It’s more popular cousin EPI is up 10% this week with a 81 RSI. Its ytd chart below seems to suggest an intensely overbought condition.

This seems like a classic buying panic prompted by the fear of being left behind as the train is accelerates out of the station. The question is does one buy or sell a buying panic like this? Our own preference is the latter.

The one caveat is a new ytd high in the Indian Rupee. It could be a sign that the global Indian diaspora is once again sending investment capital into India. Or it could be the first signal that Indian capital hidden illegally in tax havens around the world is running back into India because the new Prime Minister Narendra Modi has publicly vowed to bring back such monies. And how large are these sums? Reportedly around $1.5 trillion or nearly 75% of India’s GDP.

Longer term we are absolutely bullish on India. We have always been bullish on Indian micro. Now we have turned mahaa bullish on Indian macro. The team of Prime Minister Modi and RBI Governor Rajan does suggest comparison to the President Reagan & Fed Chairman Volcker team. A steady inflow pf capital returning to India and a rising Rupee will allow Governor Rajan to hold on to a tight monetary policy while an India open to foreign investment (as Mr. Modi’s Gujarat state has been for the past several years) would lead to higher growth & infrastructure development.

The major prospective projects include connecting North Indian rivers via canals to Central & South Indian rivers to improve agriculture and provide construction jobs. If these canals are covered with solar panels, it will simultaneously prevent water evaporation and provide electricity to local areas. This has already been very successful in the state of Gujarat. Another project is to build a long massive business corridor from Mumbai to Delhi.

Net net, we are extremely bullish on the next 10 years but we would argue that taking some chips off the table after this week’s vertical move is choosing discretion over valor.

6. “like sort of frightening”?

These were the words David Einhorn used on BTV Market Makers to describe his feelings as he listened to Ex-Chair Bernanke. There is a world of difference between Einhorn and us in intellect, experience and insight. Still we follow in his footsteps and describe what we thought was “like sort of frightening” this week. They were the following words of Leon Cooperman in his comments on CNBC Fast Money on Thursday (see 3.1 above):

- “we have about 15%-20% of our portfolio in structured credit. …

they’re up about 6% todate. … we’re paying our brokers 70 basis points a year for money, and we’re ending 1% a month in structured credit. We don’t have much cash. we’re reasonably fully invested but we have a lot of borrowing capacity, because we have no leverage”

As we heard Mr. Cooperman, we remembered the London Whale of JP Morgan & Jamie Dimon. JPM paid us depositors 60 bps annually on our deposits and their London Whale traded on it, sorry hedged JPM’s exposure. Borrowing money from depositors and generating returns for JPM’s portfolio is what the London Whale did, to our understanding at least. We know how that turned out for JP Morgan.

This is the age of ZIRP or zero interest rate policy. How does a team generate 1% a month in fixed income related products? How much leverage do you need to achieve that? Of course, there are ways to get there – you could go leveraged long emerging market debt & short treasuries, for example. We recall how easy it was to make double digit returns before 2008 by going leveraged long Muni bonds & short Treasuries against them. The latter blew up in 2008 when Treasuries rallied big while Munis cratered and the former – well, wasn’t that 1998? Clearly, you can possibly deploy structured credit portfolios that might avoid such risks. But isn’t volatility the main enemy of structured credit portfolios, especially when liquidity dries up & fixed income volatility spikes up?

The most “frightening” of Mr. Cooperman’s comments were the combination of “we don’t have much cash” and “we have no leverage“. We wish Scott Wapner had asked serious questions of Mr. Cooperman, perhaps questions like,

- under what conditions could your structured credit portfolios lose money?

- how much leverage is embedded in your structured credit portfolios?

- how are your structured credit portfolios hedged against spikes in volatility and any attendant loss of liquidity?

- how much of your borrowing capacity would you lose if your structured credit portfolios become liquidity hogs instead of liquidity generators?

- are your equity portfolios hedged against problems that might crop up in your structured credit portfolio?

Scott Wapner could have easily asked such questions because Mr. Cooperman himself opened the door by talking about their returns achieved without leverage.

We have simple minds and we think simply, very simply. One way to think simply is to remember that credit portfolios can get unglued when credit bubbles burst and those credit problems can create contagion in equity markets. We have no doubt that Mr. Cooperman’s firm is well hedged. But we think Scott Wapner and the CNBC Fast Money team ignored their own journalistic mandate by not asking penetrating questions of Mr. Cooperman. CNBC Fast Money has a tradition of being cheerleaders for hedge fund managers rather than being reporters. We find that disturbing and a bit frightening.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter