Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. “Not strong“

answered Alan Greenspan clearly and succinctly when asked on CNBC whether US data is strong or not. “In fact”, he said, “effective demand is extraordinarily weak“. He added:

- “The way I measure it, it’s probably tantamount to what we saw in the later stages of the Great Depression … it’s not anywhere near what the problems were back then but we haven’t seen anything like that since then. … While the jobs growth has been very significant, there is evidence of weakened productivity. That is a key statistic which tells how the economy is functioning. Capital investment is key to productivity growth. That has slowed down quite dramatically and productivity has followed right along.”

Supportive of this conclusion is:

- Friday – Lakshman Achuthan @businesscycle – 25 years of history adds context to recent decline in US Weekly Leading Index growth. #economy http://goo.gl/UyXkQg

The decline points to “slower overall growth in coming months“, states the article. The decline in regional PMI data was summarized in:

The decline in regional PMI data was summarized in:

- Charlie Bilello, CMT @MktOutperform – Regional Manu data in Feb – Empire: 9 => 7, Philly: 6 => 5, Dallas: -4 => -11, Richmond: 6 => 0, KC: 3 => 1, Milwaukee: 54 => 50, Chicago: 58 => 45

That raises the obvious question:

- Ashraf Laidi @alaidi – Lowest since JUL 2009 — Biggest drop since Oct 2008; Feb Chicago PMI at 45.8 — ISM next week = contraction?

David Rosenberg termed Thursday’s Durable Goods report “a mixed bag overall” and added:

- “This was a case of nice headline but shame about the details – orders are actually lower today than they were in June 2013. … Demand for labor is firming up & that is finally leading to a much-needed wage pickup … The residential real estate activity seems at risk of losing whatever momentum was in place but there is still plenty of reason to expect that housing will be a source of upside surprise over the near-term”.

The most important question for the markets is whether US is poised for a meaningful step up in the economy. That, above all, is going to decide what the Fed does in 2015 or more importantly how much the Fed does and what impact it has on the U.S. Dollar.

2. “its about time“

said Fed Vice Chairman Stanley Fisher to CNBC’s Steve Liesman about raising rates in 2015. He said “high probability this is the year” for raising rates. He added that their goals were inflation of 2% and full employment of 5 -5.5%. So they are “very close on unemployment” and he said inflation is mainly due to lower oil prices & expects inflation to rise when oil price recovers. So “its about time” to consider tightening but tightening is not likely to be successive, he hinted. That is consistent with the comments of NY Fed president Bill Dudley who argued on Friday that the risks of raising rates early were higher than those of raising rates late. According to Rick Rieder of BlackRock, this means the destination rate will be 3.5% instead of the old 5-5.5%. Rieder thought Chair Yellen was “bit more dovish” in her testimony while David Rosenberg wrote on Wednesday morning:

- “I feel that Yellen was very dovish at yesterday’s congressional testimony; she is bullish on growth and yet shows no sign of moving off zero”.

As Greece has settled down and Europe fears have subsided, Fed comments have become the primary forces moving rates. For example, a dovish Yellen caused treasury yields to fall hard across the curve while hawkish comments from Fisher, Bullard and Mester caused treasury yields to spike just hard on Thursday. This sounds sort of dumb because Fisher/Bullard/Mester are not voters this year while Chair Yellen is the “decider”. Unless the incoming data turns decisively in one direction, this circus of she said, he said type Fed comments should continue.

3. Interest Rates & Positioning

Yields fell across the curve this week thanks mainly to Chair Yellen. Kudos to Larry McDonald who predicted that on CNBC FM on Monday:

- “We have a model that measures capitulation & the last time I saw a score this good was last November with the gold miners. You have a high amount of capitulation in the Utility stocks as well as in Treasuries & TLT. … The way you got to look at TLT is time to time, the market gets offsides, the last couple of months we have had hawkish comments coming in from some Fed governors, Chair Yellen is going to talk down yields & Dollar tomorrow. If she creates a public perception of a dovish fed, that creates the bid of bonds, bid for utilities.”

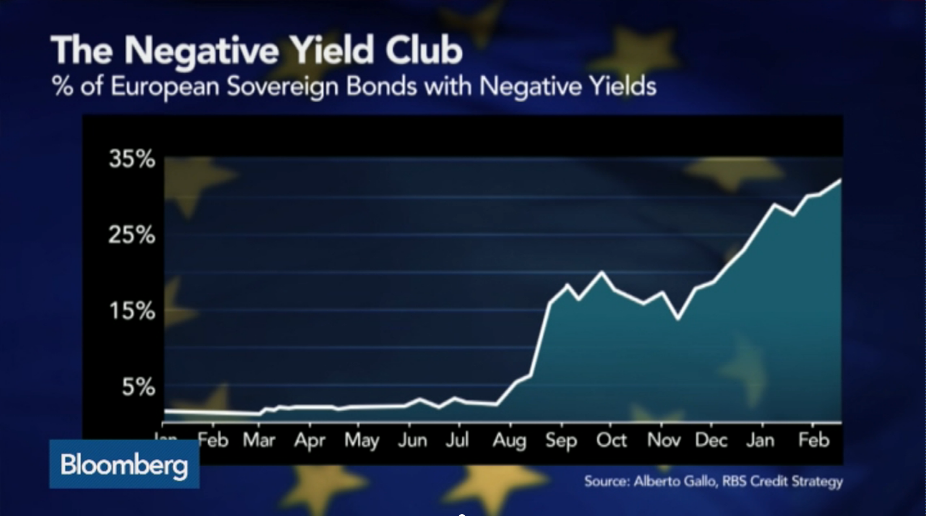

McDonald reiterated the buy on TLT on Wednesday on CNBC Closing Bell by pointing out “2 trillion of European bonds have negative yields” and so buy Treasuries. His point was made graphically by BTV’s Scarlett Fu on Friday:

- Scarlet Fu @scarletfu – Fastest-growing asset class in Europe? Bonds w/ negative yields: http://bloom.bg/1wvjFLS #negativeyieldclub @business

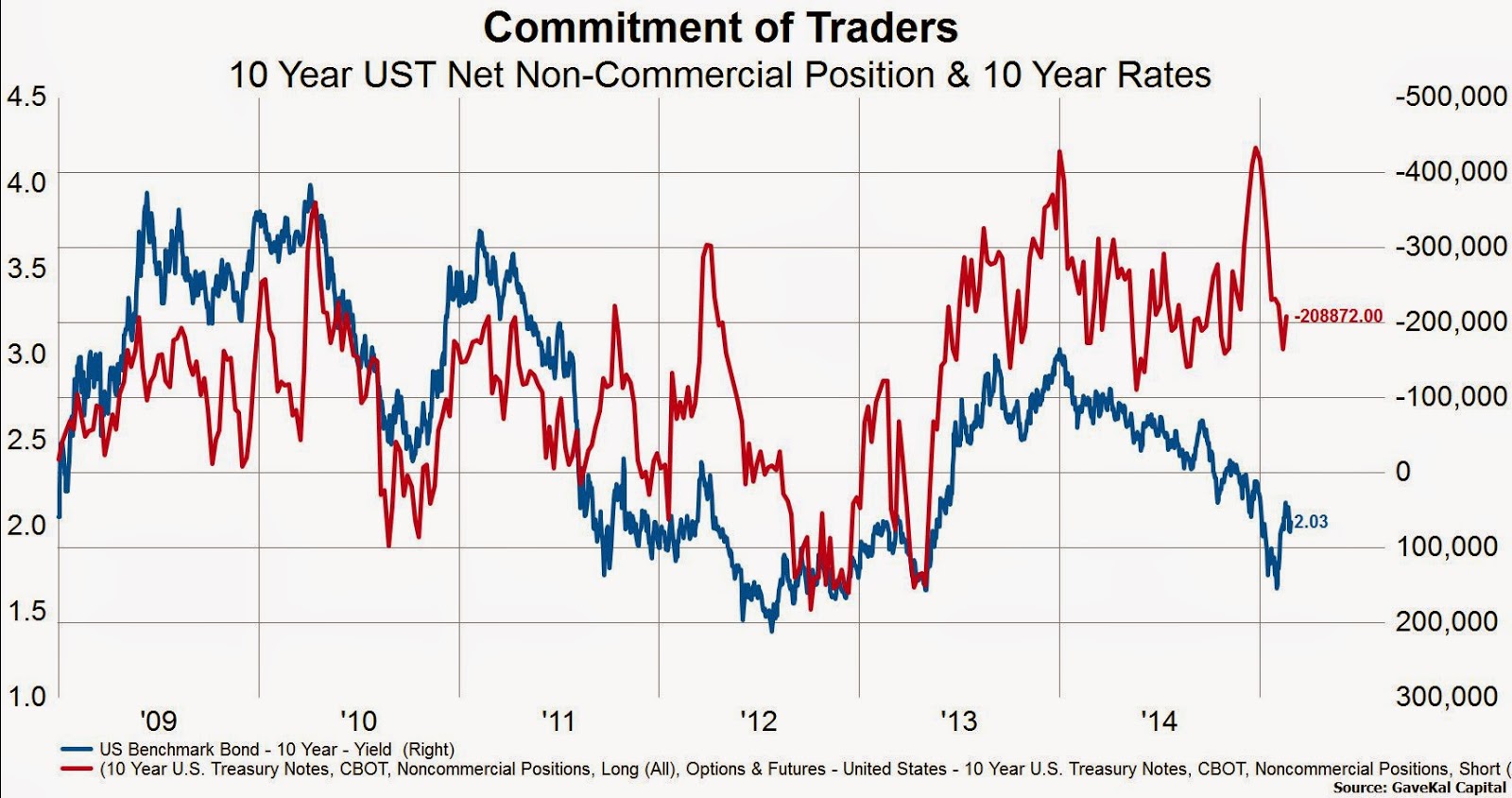

On Friday, GaveKal wrote an article about the 30-year bond titled On the Long Bond and Why the Widow Maker is Alive and Well. An apt title for shorting the long bond trade, history shows. This is a well-argued article with several charts. To us the most interesting point in that article is:

- “Despite the move higher in yields, investor positioning still shows that speculative traders carry an historically large short position in treasury bond futures and options. Traders’ net short position is indicated by the red line on the right axis and shows that speculators are net short about 208K contracts on the 10-year bond. This is an improvement to the record short position of more than 400K contracts at the beginning of 2014, but it is still far from levels consistent with a cyclical low in yields. Since 2009, lows in yields have not taken place while speculators were net short the long bond. “

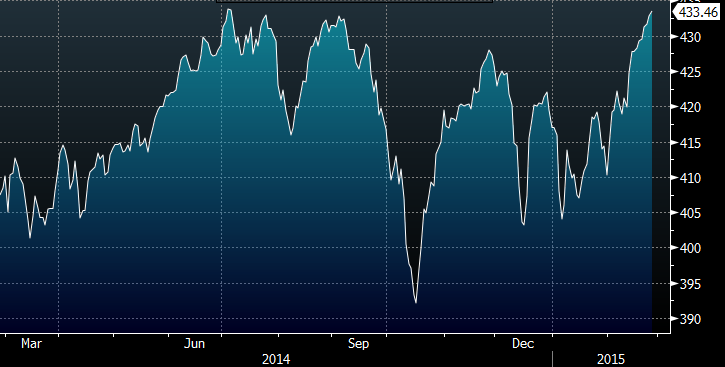

4. U.S. Equities.

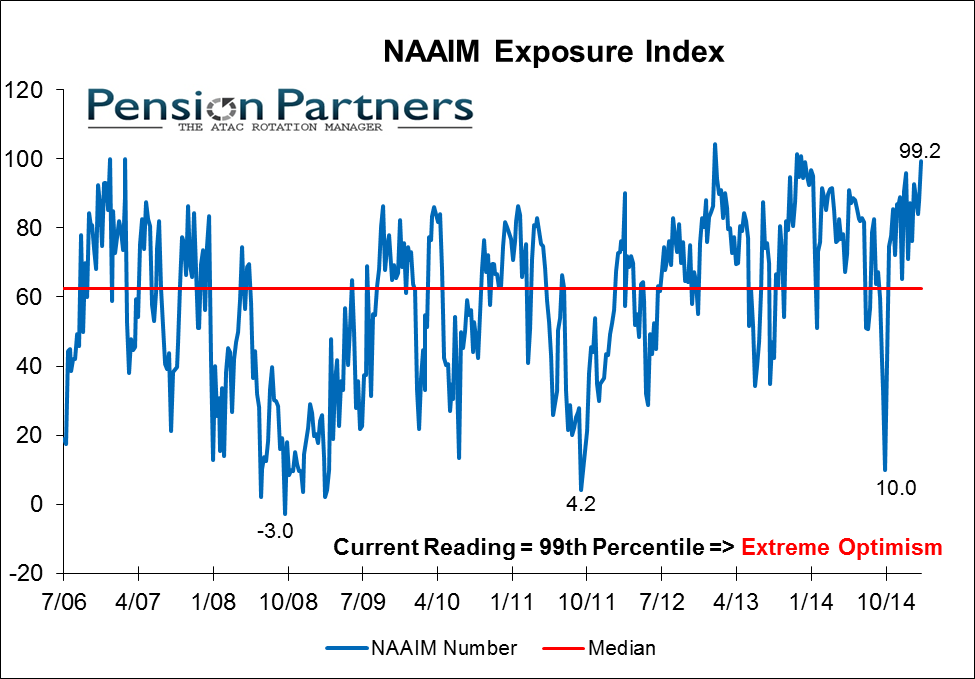

February was a perfect month to be on sabbatical as we were. The Nasdaq rose by 7% and the S&P rose by 5%. So you got to expect everybody to be in, right?

- Charlie Bilello, CMT @MktOutperform – Active Managers just about all-in now, average equity exposure up to 99.2% this week.

Not just U.S stocks but global stocks:

- Bloomberg Business @business – Global stocks reached a record high this morning http://bloom.bg/1ANR0A6

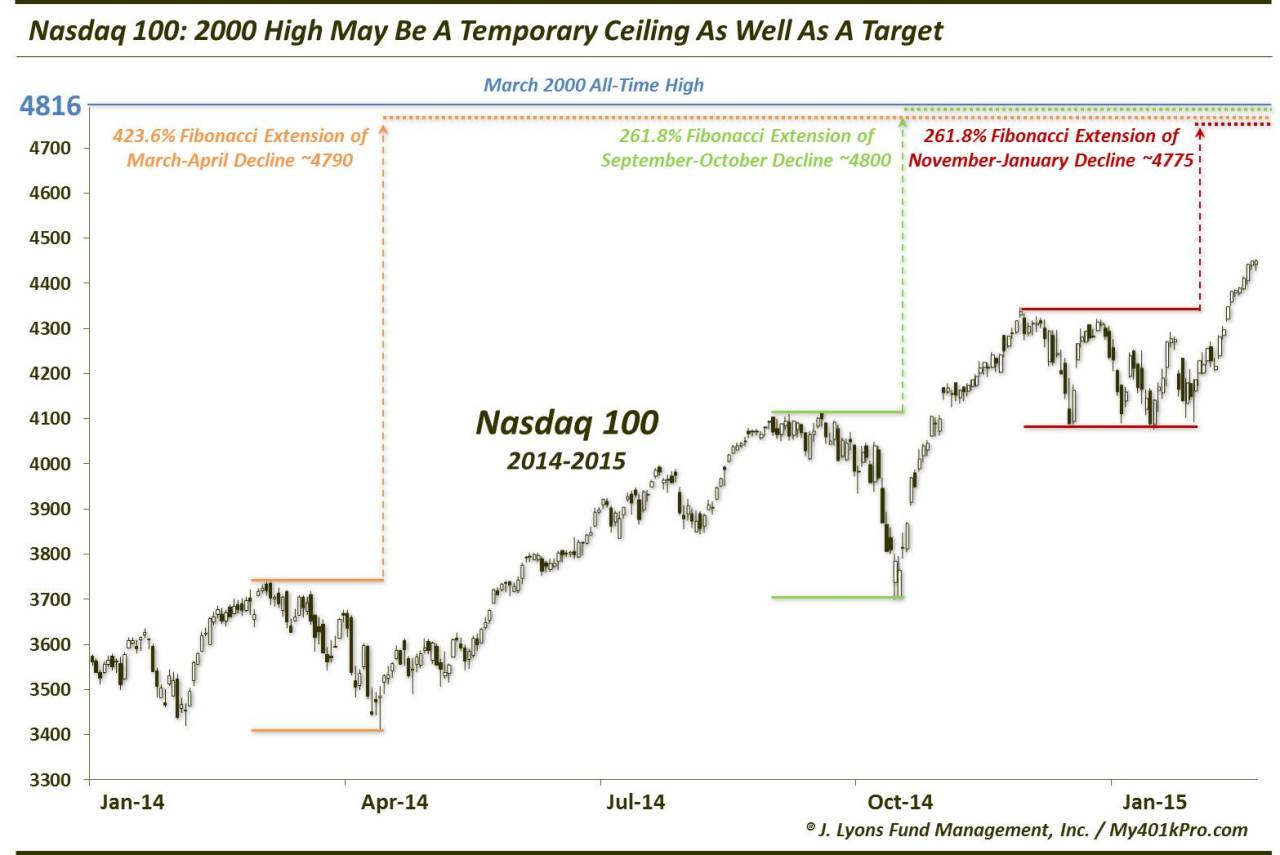

But all eyes have been on the Nasdaq which is so close to its 2000 high. The corresponding intra-day high for Nasdaq 100 was 4816. Will it break thru and make a new high as its peer indices have? And what if it does? Dana Lyons answers in his article:

- “It turns out that key Fibonacci Extensions based on the last 3 pullbacks in the NDX all align near the 2000 high in the index around 4800. Specifically, here are those levels:

- 423.6% Fibonacci Extension of March-April Decline ~4790;

- 261.8% Fibonacci Extension of September-October Decline ~4800;

- 261.8% Fibonacci Extension of November-January Decline ~4775″

So, he writes:

- should the Nasdaq 100 finally hit the target at its 2000 high, this cluster of Fibonacci Extensions may conspire to act as a ceiling for the index as well, at least temporarily.

Steve Grasso of CNBC FM expressed a similar sentiment on Friday:

- “I don’t like how the market is topping here. Guys are looking to sell, taking a lot of money off the table. Next week is a big week for directionality“.

On the other hand, Lawrence McMillan writes in his Friday summary:

- “In summary, the intermediate-term outlook is bullish, in line with the strength of the most important indicator — the chart of $SPX. The fact that breadth has not really confirmed the rally is a minor nuisance, but as long as $SPX support is not violated, breadth doesn’t matter”

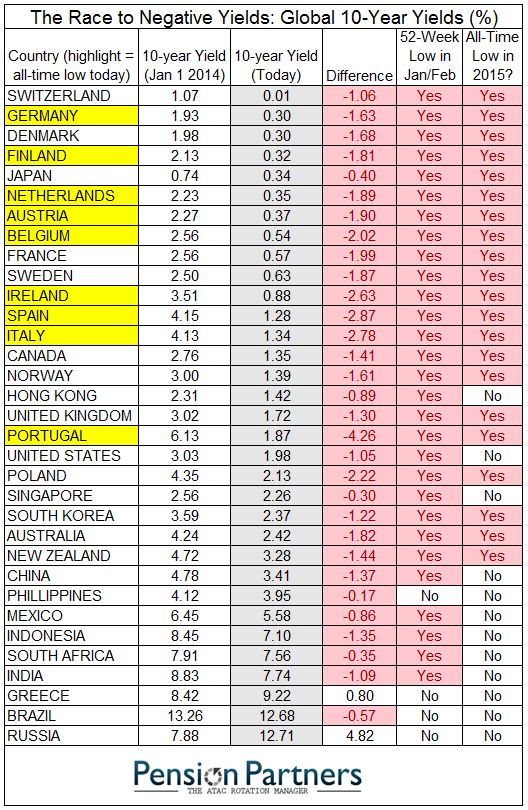

5. Europe vs. US

European markets have outperformed US markets so far in 2014. Is that sustainable? Simply put, equity markets do well when central banks are easing monetary conditions. Europe is expected to be easing monetary conditions going forward while the Fed is poised to tighten rates in the US.

- Thursday – Charlie Bilello, CMT @MktOutperform – New all-time yield lows (10-yr) today in:

Germany, Italy, Spain, Portugal, Ireland, Netherlands, Austria, Belgium, Finland

Whether this does anything for the European economy is less important than whether European QE will be a tail wind for European corporations. And European exporters will benefit from a weaker Euro. This is just a restatement of the famous “Don’t fight the Fed” rule of Marty Zweig.

Jim O’Neill came to favoring Europe over US from another angle:

- “The U.S. may not be as strong as investors think because it is growing overly dependent on the consumer for economic growth … When the U.S. consumer is starting to be more than 70 percent of GDP, as it’s threatening to do again, the U.S. structural story is not as powerful as so many people seem to now believe it is… It was, but it’s weakening.”

Another way to look at this is that the US stock market has had its run. So,

- Friday – Lawrence McDonald @Convertbond – Sell Mortimer, Sell RT “@NickatFP: US equities now account for more than half of the global market

On the other hand, resistance might be at looming in Europe as well:

- Friday – Northy @NorthmanTrader #DAX

6. Oil & Gold

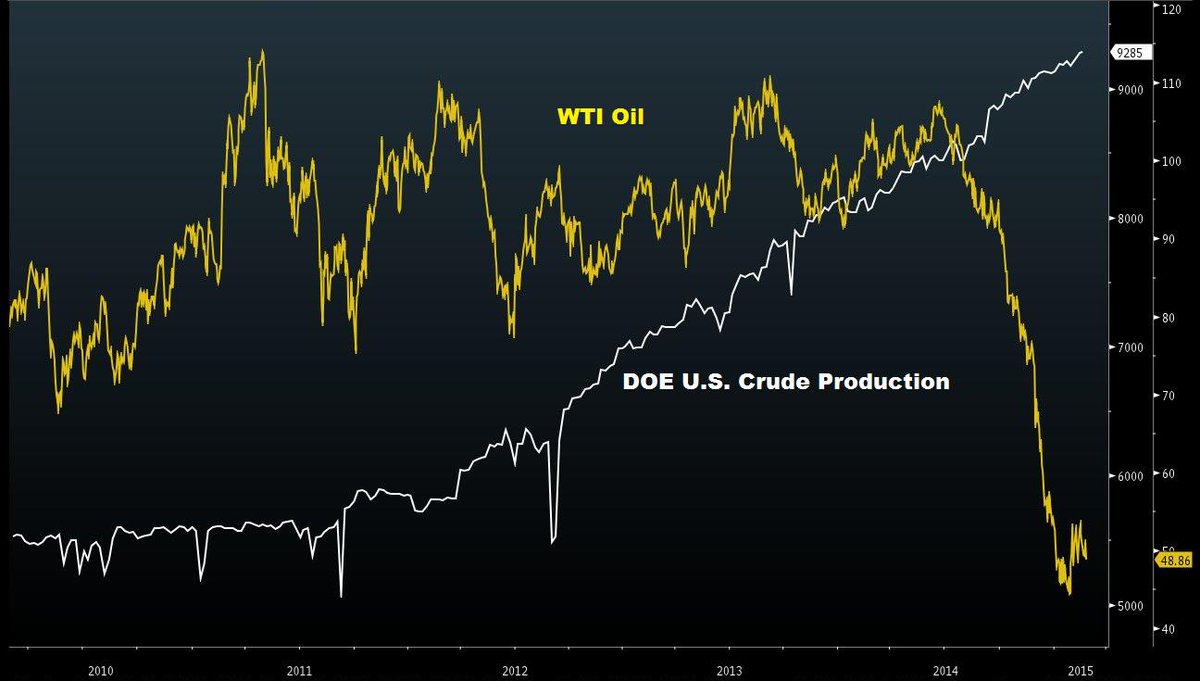

Wasn’t oil production in the US supposed to fall with the drop in the price of oil?

- Antony Filippo @Vconomics – Still waiting for that big drop in U.S. oil production (production from Alaska even increased 1% WoW).

But oil that is produced has to be sold or stored somewhere. So how much storage is left in the US? Not much is the answer Franciso Blanch of BAC-Merrill Lynch gave CNBC’s Brian Sullivan on Friday:

- “We are really close.” said Blanch noting that storage could run out by the end of March or early April. … The only option for oil producers will be to sell and therefore prices can’t hold up. “For WTI, we see those pressures being very pronounced over the next few weeks“.

If Blanch is right, then the basing in WTI over February could be a prelude to a leg lower, perhaps steeply lower. That doesn’t necessarily mean that Brent will go lower because of turmoil in Libya & Iraq.

- Lawrence McDonald retweeted JH @joshh031 – Brent/WTI spread continues to widen, now at 12.4..widest in over a year

Blanch doesn’t think this Brent-WTI spread will continue for long because, in his view, running out of storage in US could also lead to Brent prices falling.

Those who are or want to be bullish on Gold should check out the Gold Special article in Futures Magazine. Their conclusion:

- “with the EU finally on board, Gold has some bullish fundamentals on its side of the see-saw. In our opinion, those should be enough to keep a fairly solid floor under gold prices, at least in the first half of 2015 and maybe more.”

- “Our preferred strategy is selling the puts. While gold prices rallied in January, recent volatility in global currency markets (i.e.: Swiss Franc) have also surged volatility levels and thus Gold option values. This has created attractively prices strikes for put sellers. We suggest using any February weakness in Gold prices as opportunities for selling out of the money put premium – preferably well below November’s price lows”

7. Indian Stock Market

For a more detailed fundamental & technical discussion, see our adjacent article There is a party going on – In the Indian Stock Market.

8. @Interesting Laws

We came across this handle and can’t resist listing a few choice laws on the books proving that legislative facts are funnier than Jon Stewart’s comedy:

- A special cleaning ordinance bans housewives from hiding dirt and dust under a rug in a dwelling. (Pennsylvania)

- You may not sing in the bathtub. (Pennsylvania).

- In Florida, it is illegal to fart in a public place after 6 P.M. on Thursdays.

- Gay men are not allowed into public bars unless accompanied by a child. (Florida)

- Fights between cats and dogs are prohibited. (Barber, NC)

- You may not wear blue jeans down Noble Street in Anniston, Alabama.

- It is a park rule violation to be in a public park with a sleeveless shirt (Baltimore, Maryland).

- It is against the law for a man to wear his wife’s panties on a Sunday unless he has prior permission from the Bishop (Oblong, IL).

- It is illegal to be drunk on licensed premises (UK). No woman is allowed to be taller than her husband – if necessary she must chop off a section of her legs. (Indonesia)

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter