It feels like a trap door under the US Stock Market sprang open a couple of weeks ago. What felt like resilience now seems like quicksand. And the usually stirred-but-not-shaken classmate of Daniel Craig, the current James Bond, uttered the C-word this week:

- Simon Hobbs of CNBC – We have a Contagion, whether we choose to accept it or not

Yes, the Contagion that we have been speaking about since October 2014 has finally entered America.

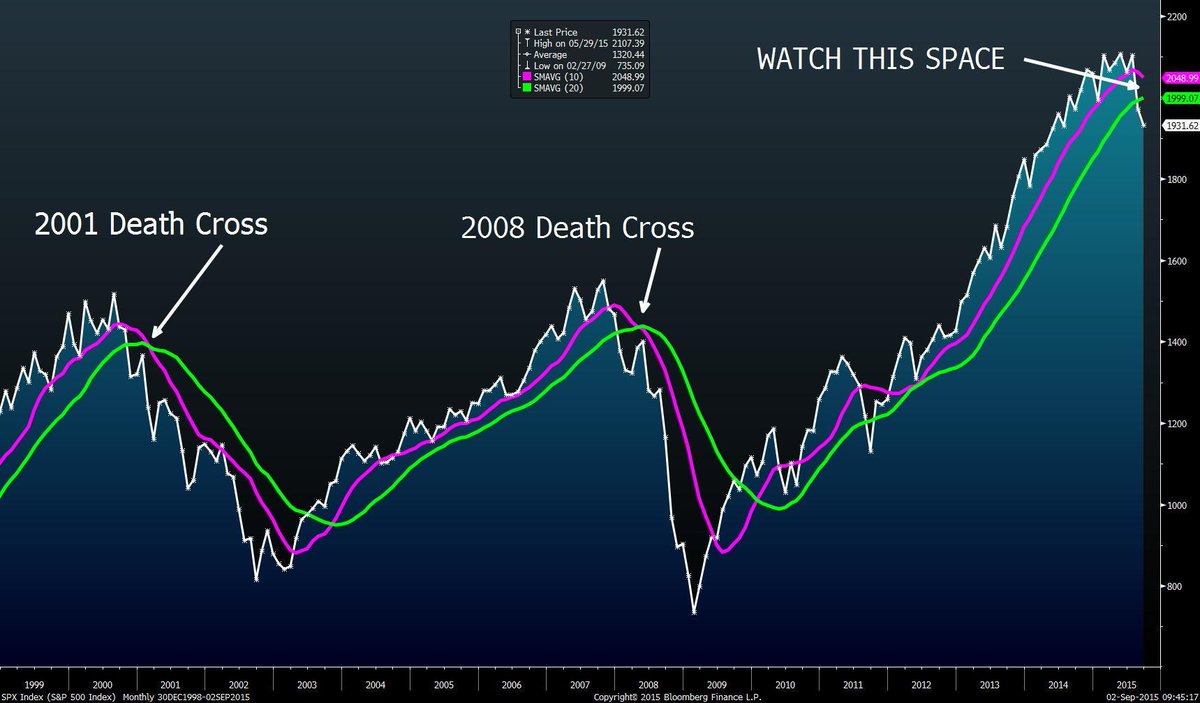

1.Is the US Bull Market Over?

Simon is a lot of things but Jack Hobbs he is not. He is often given to excitement & so you could dismiss his if you choose to. But would you dismiss Louise Yamada, the soft spoken but steely doyen of technical analysts? The “bull market is over“, said Louise this week on CNBC & BTV.

But so what? Stock markets go up & down. Isn’t it healthy for the US Stock market to go down 20% or so after it went up 300% from March 2009 to May 2015? Not quite. This decline is a big deal because it isn’t just about the stock market. It is about a decisive battle in the Great World War of Today.

Look around the World. Major centers of global growth are struggling mightily to restore even a semblance of the old vibrant growth to their economies. The Governments are powerless because they are mired in debt. So the only warriors left are the Central Banks. We discussed this in our article Contagion & Panic among Global Central Banks on November 1, 2014:

- “Therefore, the only way, the central banks argue, is to raise & keep raised the value of the stock markets in the hope that the wealth created by stocks will eventually trickle down into real economies and create consumer demand & some inflation.”

- “Folks, this is the great war of today – a war against encroaching deflation, against weakening demand; a war that is being fought by the only weapon the central banks have – pouring monies into financial markets to raise the prices of stocks & financial assets.”

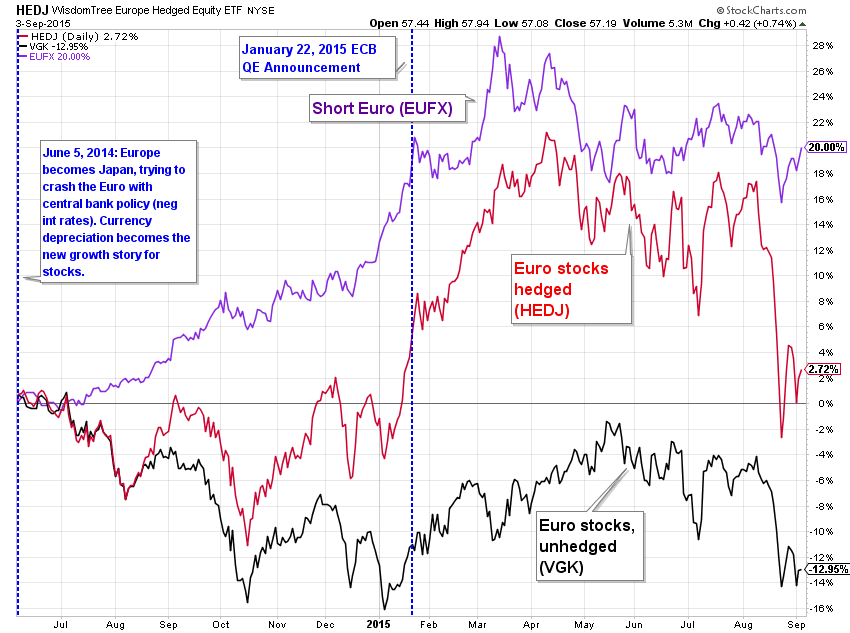

So the Yamada declaration is not just about the Stock Market. It is an announcement that the US Federal Reserve is losing the battle against the deflationary contagion that has been sweeping the world. And the US Fed has been the only warrior standing. Even “whatever it takes” Mario Draghi, the man who catapulted the European & Global stock markets to new highs from August 2012 onwards, cannot sustain his early wins.

- Charlie Bilello, CMT @MktOutperform – European stocks have done nothing under neg rates/QE thus far. Response: dovish Draghi hints at more QE

What if the US stock market gives up all its gains under the massive quantitative easing that was pioneered by the US Federal Reserve? Would that be game over in the war against deflationary contagion?

2.The Fall of the New Maginot Line

Remember the Maginot line built by France after WWI to prevent Germany from attacking it? It was a massive robust structure and it represented safety for much of Europe. Then it fell and disaster ensued. France, Britain & Europe learned the very hard way that robustness is not resilience.

Since 2009, the world has lived complacently under the umbrella of the great growth of the Chinese Economy. The world’s confidence in the omnipotent & omniscient Chinese leadership was as absolute as Europe’s confidence in the Maginot line. Last month, this new Maginot line fell. Like the proverbial emperor, the Chinese leadership revealed to the world that they had no clue.

Bernard Baruch is reputed to have said “The main purpose of the stock market is to make fools of as many men as possible.” The Chinese Government learned that last month as other institutions have over the centuries. A Government can create proverbial Potemkin villages out of real estate and physical commodities. But no one can do it to stock markets in a sustained manner. The stock market has a unique flair for discovering the Achilles Heel and violently attacking it. And the Chinese Stock Market did it to China’s Government last month and destroyed the Maginot Wall of the faith in their capabilities.

3.China, Choose Your Weapon – Currency or Interest Rates?

A basic truth is that a government a relatively open current account cannot control both its currency & its interest rates. The Chinese leadership admitted it last month when they “devalued” their currency by a bit and the earth shook. What has been seen in China in the last decade is entirely unprecedented in human history. And now it seems to be coming apart at the seems.

This week, the CEO of the massive port in Long Beach California said on CNBC Squawk Box that container shipments to China have fallen by 10%. This is another empirical evidence that the Chinese economy is in a major slowdown. Since confidence is based on lack of fear rather than reality, the Chinese Government has been bringing back to China some of its massive Dollar reserves and using that to shore up its economy and the stock market. But bringing back Dollar reserves by converting them to the Remnimbi acts as a tightening and defeats the purpose of stimulating the economy. And China has already lost $200 billion in its vain attempt to shore up its stock market.

Clearly, protecting its currency by bringing back US Dollar reserves has not helped. So why not devalue the Chinese currency, the Remnimbi? Remember the Maginot line? Faith in China’s ability to manage its affairs & its $-pegged currency has resulted in over one trillion dollars to move to China. These monies are borrowed from US & Japan at nearly zero rates and deposited in Chinese currency to earn higher interest. But this trade assume that the Chinese currency remains stable against the US Dollar. If China devalues its currency to the extent it should, then this “carry trade” will instantly turn into a loser from a winner. Then how fast will the trillion dollars fly out of China?

4.Will China follow Europe & Japan?

What is the one tool that global central banks have used to fight deflationary economic slowdown? By undertaking massive quantitative easing. The US Federal Reserve under Ben Bernanke pioneered this aggressive tool by which the Fed buys US Treasury bonds in the open market and thereby adds monies into the financial system. This was the only tool available after they took interest rates to Zero, yes Zero percent.

The last time Central Banks in US, Europe, and Japan were united in fighting deflationary contagion was in the second half of 2012. Europe’s Draghi made his famous declaration to do “whatever it takes” in August 2012. A month later, Bernanke launched his QE3 or QE-forever in September 2012. A few months later, the Bank of Japan launched its own QE. When Draghi launched his verbal QE, the Euro currency was around 130. When Kuroda of Japan launched his real QE, the Yen was around 100. Since then, the Euro and the Yen have fallen by 16% & 18% resp. against the Dollar.

So why shouldn’t China launch its own QE to add much needed stimulus to its economy while keeping its Dollar reserves intact & to depreciate its currency. One problem is that, unlike the Euro & the Yen, the Chinese currency is official pegged to the US Dollar.

Our first contagion article was on October 11, 2014. Three weeks later, on October 31, 2014, Japan announced a major increase in equity allocation in its giant Pension Fund to support the Japanese stock market. Our 3rd contagion article was on January 10, 2015. Two weeks later, on January 22, 2015, Draghi launched his 1.1 trillion Euro QE.

So will this pattern repeat with China? We doubt it. As we said, the Chinese currency is pegged to the US Dollar and that ties China to US monetary policy. Unpegging this is a delicate matter and needs to be handled with caution.

President Xi Jinping is scheduled to visit America later this month and after the Fed announces its decision about hiking US interest rates on September 17. We have no doubt President Xi’s visit will include intense discussions about the path of the Chinese currency.

If the Chinese economy keeps weakening and its financial markets keep selling off, would it be natural for China to launch its own QE later this year or in early 2016? We think so.

5. Desperation at the US Federal Reserve?

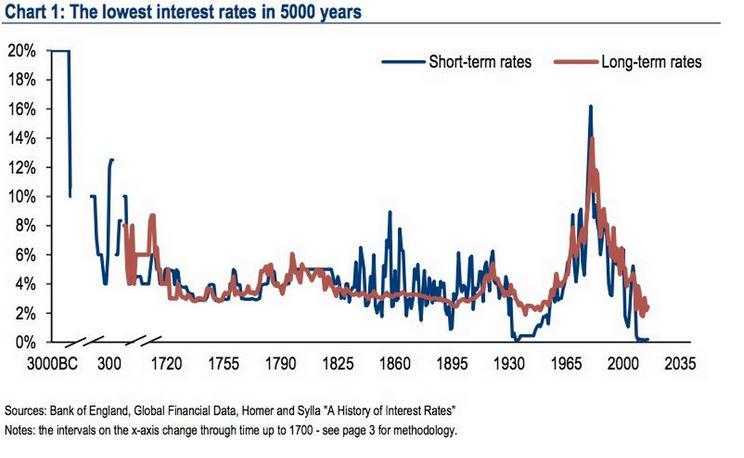

By many accounts, the Fed is “desperate” to raise interest rates, not by a large amount but merely by 0.25% from today’s zero rate. This, by itself, should show you how utterly messed up the world is. The Fed has maintained zero interest rates for the past 9 years. No one, not a single soul, would have predicted this back in 2006. Not only has the interest rate been maintained at zero, the Fed has done at least four large programs to stimulate the US economy – three QEs and one operation TWIST. As a result, the Fed’s balance sheet has increased by an previously unimaginable 4 trillion dollars.

Surely raising interest rates by 0.25%, a mere quarter of one percent, should be an utter triviality. After all, interest rates are at the lowest they have been in human history:

- @fiatcurrency – The lowest interest rates in 5000 years

In contrast, witness the specter of the IMF, the World Bank, and the G20 all politely & discreetly warning the Fed from this measely 0.25% increase.

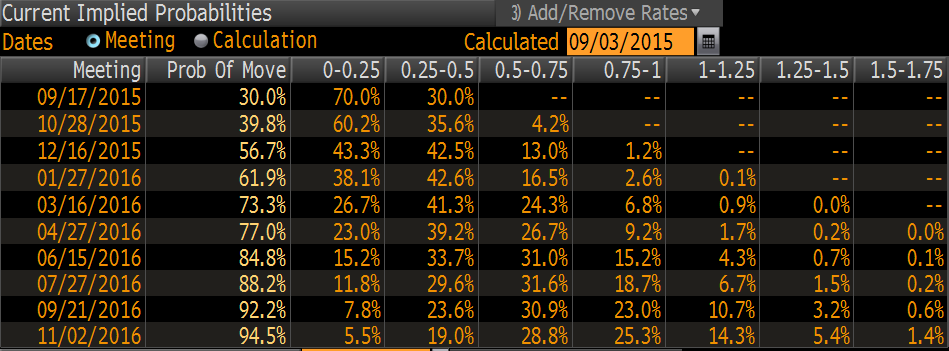

Fed can ignore the above but can they ignore the intensely loud noise coming from the stock market? Does the Fed want to see all the gains in the stock market from its multiple QEs evaporate to merely meet their theoretical and emotional needs of getting off the zero-rate? Does the Fed want to see destruction of the wealth effect they have labored so hard to create? So what will they do?

On one hand, you have a virtual consensus among the talking heads that the Fed will tighten on September 18th. On the other hand, you have the verdict of the Federal Funds market that they won’t.

- Charlie Bilello, CMT @MktOutperform – 2 Weeks until FOMC meeting & hike odds down to 30%. With $VIX spike in Aug, no surprise… http://stks.co/t2nmI

Why is the Stock Market screaming a warning? Is it saying that the contagion is finally entering America and that the Fed could be on the verge of making a major mistake?

6. US Dollar – the Agent of the Contagion?

Look at the graph below from our first article about the contagion on October 11, 2014:

(Screaming rally in the U.S. Dollar – October 2014)

That rally in the summer & fall of 2014 caused turmoil in Emerging Market currencies. Well, things have gotten worse in the past 11 months:

This Dollar rally has caused havoc in global trade, the engine of global prosperity. With Europe, Japan, Russia, Brazil, and now China in deep trouble, the contagion is now entering America via weakness in trade. Earning expectations of US companies have been slashed by about 15% this year and that is one reason for the US stock market to weaken.

Conditions have become so bad that we are seeing China and other Asian countries sell their US Dollar reserves and repatriate monies back to their own countries. This has caused long term interest rates to back up in America causing some more tightening in the US financial system.

If this is happening already, how much more havoc could the Fed add by raising interest rates? But this is merely a cyclical issue and could be addressed in the short term by the Fed standing pat on September 17th & talking down the Dollar.

That would not address the structural problem that is deeper and more intractable. That problem is the unintended consequence of the mega-mega change of our life time – the transformation of America into a potential exporter of oil & gas from being the world’s largest importer. What does this have to do with financial contagion?

The US Dollar is the reserve currency of the World. The world’s trade is denominated in US dollars. That means buyers have to deliver US Dollars to sellers to close a deal. America used to supply massive amounts of Dollars into the global system by buying oil from overseas. This supply of Dollars is now virtually shut down as US has become self-sufficient in oil. This has left the global system with a woeful shortage of Dollars.

So the problem is mot merely the price of the US Dollar in local currencies but also the lack of supply of Dollars. This is another reason why some Emerging market countries are selling their Dollar reserves. Another way the contagion is finally entering America.

So what is the solution? The Fed should launch QE4?

7. Real Solutions

If you are anything like us, you are literally writhing in pain at the thought of more QE from the Fed. Relax; we have been not believers in QE2 or QE3. Let us remind you what we wrote in our first contagion article on October 11, 2014:

- “Monetary measures like Quantitative Easing (QE) only buy time. They don’t cure the disease. Europe’s structural disease will take years to cure. What is needed is an immediate jolt to European economies, especially to the German economy”

In case you haven’t noticed, Europe is in worse trouble than last year. Their first problem, Greece, has been and keeps going from bad to worse. Elga Bartsch, Morgan Stanley co-head of economics, said this week on BTV Surveillance that “Grexit is our base case“. The recent migrant problem is another evidence of Europe’s structural inability to come to any region-wide consensus. Instead of greater integration, the migrant resettlement disputes are making European leaders talk of reintroducing national borders with immigration agents. How bad is this for European consumer confidence or trade?

Europe desperately needs a positive jolt that reduces fear & increases confidence. That is what we suggested back in our first article and what we say now – immediate negotiated end to trade & financial sanctions on Russia followed by a dialog between Russia & Europe about Ukraine et al. An unplanned, unexpected conflict with Russia remains a major worry in Europe and that needs to be taken off the table. Increased trade between Europe & Russia will relieve pressure on Oil and increase consumer confidence.

What about America? The Fed has taken monetary policy as far as it can go & then some. It is time for fiscal policy to step in and remove some of the contraction imposed by the 2013 Sequester. What America needs in early 2016 is an across the board tax cut ideally combined with entitlement reform. The latter is more intractable but a tax cut should be a slam dunk. It will lead to higher consumer after-tax incomes, higher consumer spending and increased capex by corporations. Higher growth in America is a consummation that is devoutly wished by the world and that will be stop the contagion in its tracks and even force it to retreat.

Is there a chance in heck of either of the above happening in 2016? Heck No. So all we can do is to track the spread of contagion and keep protecting ourselves.

PS: Below are the links to the three prior contagion articles:

- October 11, 2014 – A Contagion is Sweeping the World & It is neither Ebola nor ISIS

- November 1, 2014 – Contagion & Panic among Global Central Banks

- January 10, 2015 – Happy New Year To Me – Says the Contagion?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter