Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.“I will do a shot

for every basis point they hike“, said Josh Brown of CNBC FM on Friday. That is an emphatic and noble sentiment. Will he pay up though? After all, CNBC Fast Money has a track record of not paying off their bets, as we know. This may have been the most value added comment we heard this week from “talking heads” this week. We have no interest in discussing what no one can predict apart from Chair Yellen. And this may be the last week when we can defer the will-they-wont-they discussion. Because even if they don’t raise rates this coming week, they will leave open the possibility of a hike in October & beyond.

The Fed Fund market is showing 1/3 rd probability of a Fed hike. That means, as Jim Bianco said last week, the market will quickly price in the next few Fed hikes if they raise rates this week. Bianco laughed last week at the notion of Fed declaring one-and-done. This week, Ken Rogoff provided a more sober but even more disdainful rebuttal of this one-and-done stupidity.

- Thursday – Bloomberg Business @business – Kenneth Rogoff slams one of the most popular theories for what the Fed should do next http://bloom.bg/1FC8Kio

The article states:

- “Market participants have been coalescing around the view that the Federal Reserve’s liftoff from near-zero interest rates will be a “one and done” affair.

- What is the logic of doing it, also?” he said in response to a question on the merits of a rate hike followed by a long pause. “It’s very asymmetric. If we see inflation, they can start raising rates, and if you go in the wrong direction, it’s harder to do something about it.”

- The danger in signaling a long pause, or potentially having to reserve a hike soon thereafter, is that it fosters unnecessary uncertainty, the professor asserted. “You’re trying to create some certainty about what your path is, to have a reaction function people understand,” Rogoff said.

- He drew a comparison to Chinese policymakers’ decision to devalue the yuan; while the depreciation itself was rather marginal, the market is on tenterhooks for what’s coming next and isn’t sure what would merit further action.

- So if monetary policymakers are lifting rates just to prove they can, it doesn’t seem to be worth it, according to the professor. To me it’s not a 50/50 call if you only think you can move once and have to wait,” Rogoff concluded.”

The key is what happens if they do raise rates this week;

- David Rosenberg – If you think the Fed is going to go, keep some powder dry but for the ensuing three to eight weeks

2.Three Rivers or Really Two Big ones?

David Tepper, owner of a part of Pittsburg Steelers, is no stranger to the Three River Stadium. So we weren’t surprised to hear him explain what’s going on in river terms. We like Tepper because he speaks in simple terms that even we can understand. And he has made money for our readers, at least given opinions that would have made money had readers followed them.

Tepper was very simple as always this Thursday. He pointed out that until this year, all the major rivers flowed one way – Fed with accommodative money, Draghi, Japan, China & EM adding to Dollar Reserves. And when “you have the rivers flowing one way, all the rivers flowing one way, every dip should be bought”.

He pointed out that the China & foreign countries reserves river is now flowing the other way; the reserves are being withdrawn from the US. One river flowing one way and another the other way is adding to churn & volatility. No one knows which is bigger, he said. Besides, he has problems both with earnings & valuation:

- I have problems with earnings growth, I have problems with multiples; people have high expectations for next year – $125-$130 for S&P earnings. Won’t get there. May be $120 * 15 PE which gives you 1800 on S&P or 16*$125 = 2,000.

- So flat stocks is not a bad place to be right now; Fed doesn’t tighten and markets rally then may be I can short at higher levels.

- if you invest in the stock market at 1800 & earnings grow a little bit say 5.5% a year, you will make money at the end of 5 years; the market is at a level where it needs to correct; if we get a 20%, 15% correction I would buy; & it doesnt mean we are going back to that 20% either.

Speaking of China, he said:

- “[The Chinese] just keep making policy mistake, after policy mistake, after policy mistake over there, … It’s a learning curve to get onto a market economy. You could say that. And maybe one day they’ll get it.”

- But Tepper said it’s not good when that “learning curve” is playing out in real time in the world’s second-largest economy. “It’s kind of bad when they’re a $10 trillion or $11 trillion economy and they influence more than a third of the world’s economy.”

But what if all rivers begin flowing the other way? Then “every rally should be sold“. But, he doesn’t “know where it is at“. But he opined that if the reserves leaving river turns out to be bigger than the QE river, the Fed might have to do another QE to reverse that flow.

3. China

Paul Richards of UBS said on CNBC FM 1/2 that “China calmed everybody at the G20“. But China wasn’t able to calm Citi’s chief economist who said China is “Financially Out of Control” and that “Corporate debt is the elephant in Beijing’s room“.

- “As for the advanced economies, Buiter said China’s woes could infect them via declines in trade given it accounted for 14.3 percent of global commerce in 2013. China unloading some of its $6 trillion of foreign assets such as U.S. Treasuries could also roil international financial markets, while the dollar could surge as investors seek a safe haven.”

- “A 2016 recession could be avoided if monetary and fiscal policies are eased, yet Buiter sees most rich nations running low on ammunition either because interest rates are at rock bottom or because politicians won’t want to use the tools they have. If the Federal Reserve andBank of England raise rates soon they could be cutting them again by the end of next year, he said.”

Corporate debt is not just China’s problem but a global one, as Larry McDonald said to CNBC’s Brian Sullivan:

- “[Debt is] not a problem when equity prices are rising but when equity prices roll over you have low equity market participation & high debt; we have 9 trillion of equity market cap lost globally & in 2008 we had $12 trillion; but today is particularly bad relative to the debt levels; in 2008 we had a lot of debt on bank balance sheets and today we have a lot of debt on global corporate balance sheets, global sovereigns, emerging markets; because global balance sheets are very very debt heavy; it is just as troubling as in 08 or more so”

Citi is not the only one:

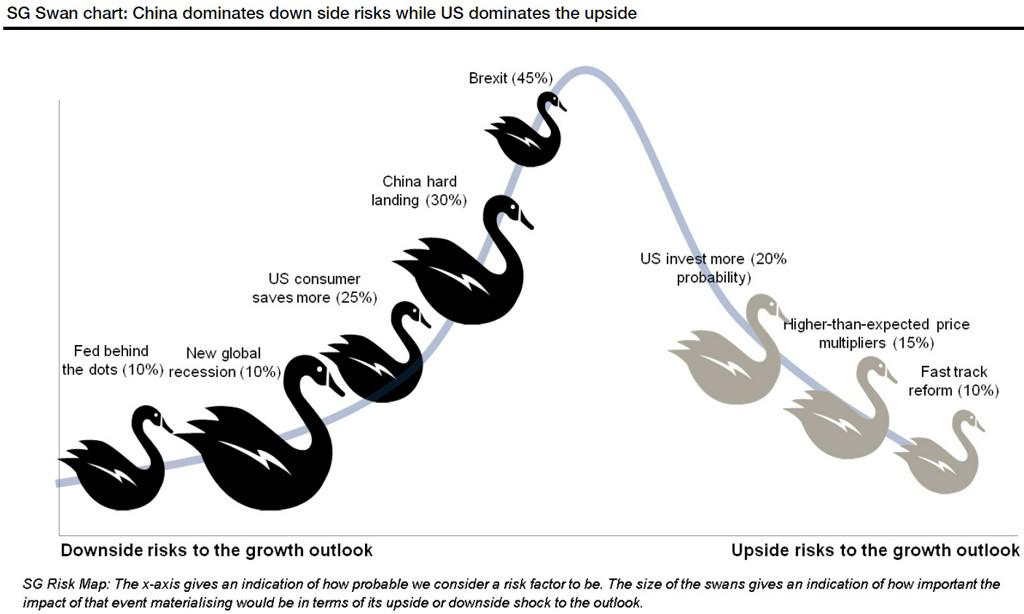

- ValueWalk @valuewalk – 30% Chance Of China Hard Landing; “Black Swan”: Societe Generale http://bit.ly/1Mh5rVv

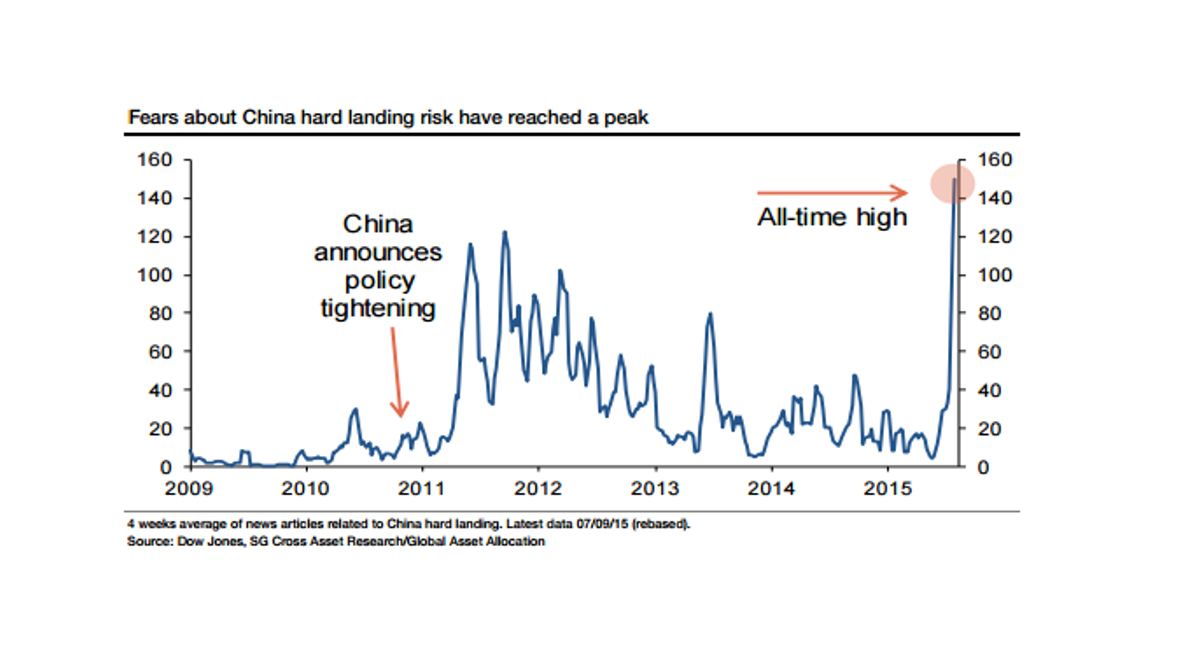

But is there anyone who hasn’t heard of Chinese troubles by now?

- Sara Sjölin @sarasjolin – China jitters are now at an all-time, this chart shows

http://www.marketwatch.com/story/china-jitters-are-at-an-all-time-this-chart-shows-2015-09-10?mod=MW_story_latest_news …

So what if the Fed doesn’t raise rates next week, Dollar goes down, BoJ talks & acts dovish and China demonstrates control of its stock markets? Will that be all rivers flowing the good way at least for a short awhile?

4. Bonds

Treasuries acted badly most of the week despite strong 30-yr & 10-yr auctions. Every rally except for Friday was sold. Was it the EM reserves river or was it uncertainty ahead of the Fed?

- J.C. Parets @allstarcharts – I still think treasury bonds lack any kind of intermediate term trend. I can see $TLT bounce towards 125, but then what? eh

Jeffrey Gundlach on Treasuries in his interview with ETF.com:

- “The more you analyze the markets, the more you realize the message has been crystal clear now, for nearly two years. The long bond wants the Fed to tighten. And I know that a lot of people have a hard time with that notion, but it’s difficult to look at the market data objectively and come to a different conclusion.”

- “People are far too committed to the idea that interest rates are about to explode higher. That’s been the wrong idea for years. And we’ve jumped to the wrong conclusion that the Fed tightening is somehow a disaster for long-term bonds. It’s exactly the opposite.”

5. US Stocks – Next Week

This was a rare good week for stocks with all major US indices up 2%. Why? May be it is as simple as last week’s tweet:

- Friday, September 4 – Jason Goepfert @sentimentrader Small speculators went net short index futures by $2 billion this week, 2nd largest short position in 20 years.

No wonder, Tuesday was so explosive. But did they cover these index futures in this week’s rally?

- Jason Goepfert @sentimentrader – Small speculators in index futures went to $6 billion short this week. New all-time extreme.

How do smart traders view this?

- @Northy – Right in time for OPEX

In the good old days, Options Expiration weeks often became bonfire of the shorts. Will that pattern repeat next week, especially if whatever the Fed does is deemed bullish?

But we must point out that the August 2015 option expiration was very ugly. Not only did Friday, August 21 closed ugly but Monday August 24 opened with the flash crash. But is that likely to repeat next week or will the option expiration pattern revert to normal? Remember the August expiration came two days after the release of the Fed minutes. Next week’s expiration comes the day after the FOMC meeting on Thursday.

What does seasonality indicate?

- Chad Gassaway, CMT @WildcatTrader – Next week (week 37) is the 8th strongest week of the year. The following week is the weakest since 1950

And,

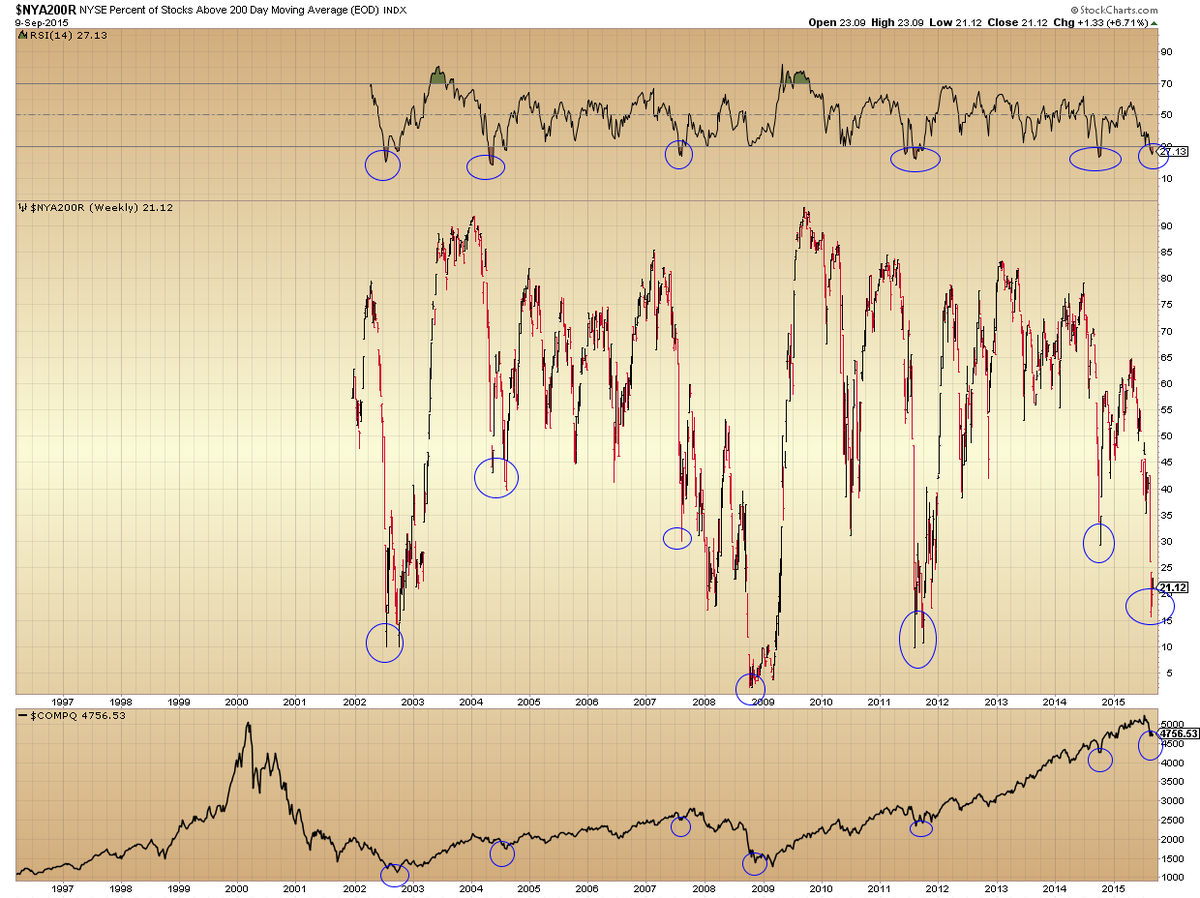

- jesse stine @InsiderBuySS – RSI for % of stocks> 200dma has been oversold 5 other times the past 15 years. Result each time: Enormous rally.

What about sentiment? The Weekly Market Summary from Fat Pitch points out:

- “The Citibank Panic/Euphoria model indicates that investors are at ‘panic’ levels. The most recent comparable times were June 2012 and October 2011, both lows in equities. When ‘panic’ has been at current levels in the past 30 years, equities were higher 12-months later 96% of the time (blue shaded areas).”

Would Chair Yellen kill this lovely set up or will the Market Gods teach us a lesson for our arrogance? Or we could see both as in:

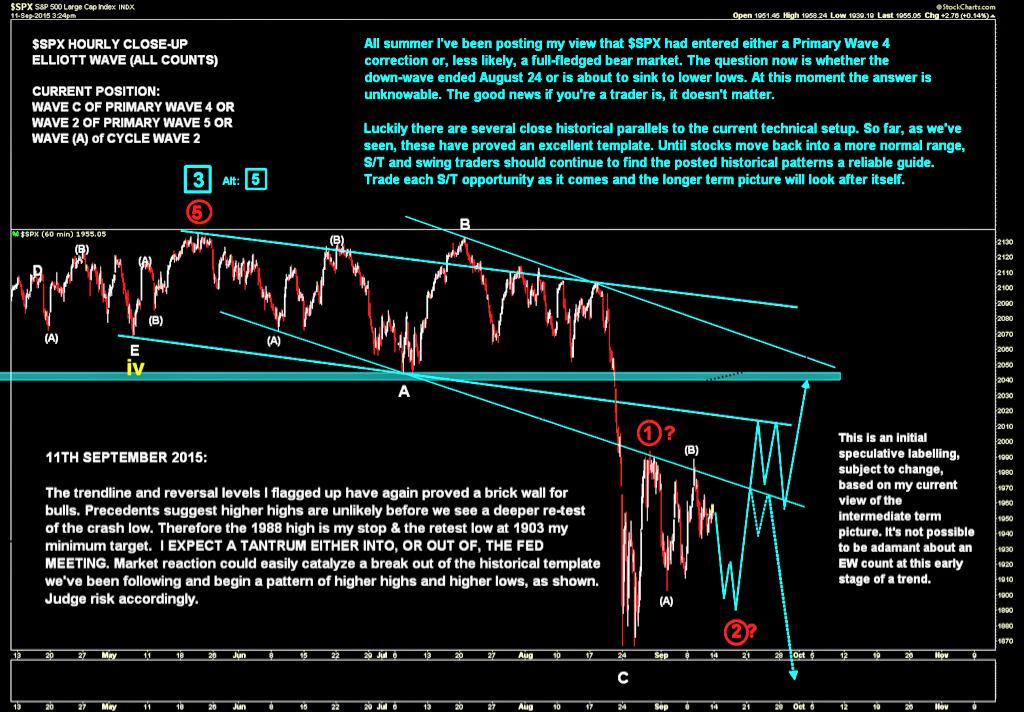

- James Goode @OntheMoneyUK – $SPX Roadmap Update: Historical pattern suggests tantrum into Fed meeting, rally on the way out $SPY $ES_F

6. US Stocks – Intermediate Term

The above is wonderful if it happens. But the bigger question is what happens after this next rally? These two cases were discussed in detail in Navigating the Next Rally at NorthmanTrader.com. This article is a comprehensive analysis with numerous interesting charts. Below are a couple of excerpts:

- Firstly a general observation: The lows in 1998, 2002, 2009 and 2011 all had one common element: A lower price retest with a positive RSI divergence. In all of these cases these retest lows came within a 1-3 month period after the initial low. This suggests that if we are to make a successful long term low another retest is in the offing at some point this year

Their bear case:

- A key trend line has been broken on the $ES. A rally into the weekly 50MA would likely also produce a retest of the broken trend line. This retest also coincides with major overhead resistance …

- This could structurally set up for a massive heads and shoulders pattern and a subsequent break below the neckline would produce a measured move into the 1538 zone which coincides with major support.

- Why is this level major support? Two reasons, it matches the previous highs of 2000 and 2007 and would also coincide with a 38.2% Fib retrace of the 2009 rally

Their bullish case:

- “For one M1 money supply is still at the highs and since 2009 there has been no case where M1 has lost the battle … So we can currently observe a massive divergence between price and M1 money supply. Explaining this divergence is the massive exodus we have witnessed with people dumping stocks. And it is this drastic exodus that may seed the next big rally. Just looking at money flows outlines the risk/reward equation”

On the other hand, Tom McClellan argues the opposite in his article VIX Above All of Its Futures Contracts :

- I am going with the premise that the stock market has indeed had the major top it was supposed to have in 2015, and that it is supposed to be in a downtrend, lasting until April 2016. So the rules of interpretation during downtrending markets should apply, which means that we should not get suckered in by the siren song of a really high spot VIX reading compared to futures

7. Emerging Markets

Gundlach on China & its impact on EM:

- “We’re shunning emerging market equities pretty heavily here. The China aspect of emerging markets is very troubling. And emerging market equities are performing so badly that it just seems like one of these falling knife situations. If you look at the iShares MSCI Emerging Markets ETF (EEM | B-100), it’s at a lower level now than it’s been at any time in 2010 through 2014. That might mean it’s a buying opportunity. But when you look at the chart, it looks really bad. So we’re not really interested in broad emerging market equity exposure“

The big news this week was S&P’s downgrade of Brazil.

- Jason Goepfert @sentimentrader – As usual, S&P downgrades AFTER a major decline. Emerging mkts rallied after prior Brazil neg rating changes

That takes care of B & C in BRIC and R is unmentionable. So that leaves:

- Gluskin Sheff @GluskinSheffInc – David Rosenberg: India is the last BRIC in the wall…the only one left to see anything remotely close to 7-1/2% growth this year

Will the EM correction be over until the last standing BRIC topples or will India bounce from this level?

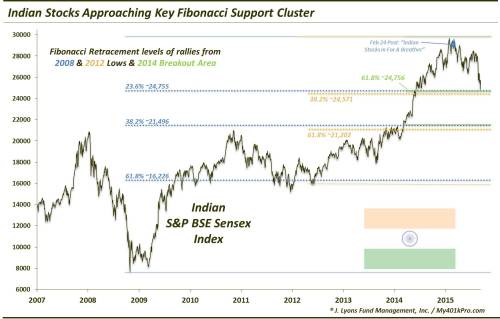

- Dana Lyons @JLyonsFundMgmt – ICYMI>ChOTDs-9/11/15 Indian Stocks Ready To Resume Bull Market? $Sensex $EPI Post: http://tmblr.co/Zyun3q1u0hRYF

He writes that “Sensex is now approaching a potential level of support, based on an assortment of analyses” and adds:.

- First off, we have another one of those Fibonacci clusters. This time, it consists of 3 key Retracement levels from the major lows in 2009 and 2012 as well as from the 2014 breakout level, all lining up in the same vicinity near 24,600:

- 23.6% Fibonacci Retracement of 2009-2015 Rally ~24,755

- 38.2% Fibonacci Retracement of 2012-2015 Rally ~24,571

- 61.8% Fibonacci Retracement of Rally from March 2014 Breakout Level ~24,756

- Here is the chart showing the Sensex approaching this confluence of Fibonacci levels.

- The 2nd piece of potential major support comes from the long UP trendline from the kickoff of the Indian secular bull market in 2003. Using a logarithmic scale, this trendline precisely connects the 2003, 2009 and 2013 lows. And it is fast approaching current price levels now.

His basic opinion – “the Sensex does stand a good chance of bouncing from the nearby area first“.

8. Dollar & Commodities.

David Tepper scoffed at the possibility of a 25 bps hike impacting the US economy. But he did say that currency markets could be impacted by that rate hike. The Dollar closed below its 200-day moving average on Friday and is oversold. If the Fed raises rates next week, the biggest and most immediate impact would be on the Dollar. But is the Dollar sending a signal about Fed staying pat? And if the Fed doesn’t raise rates, what happens to Commodities?

- DK1 @canuck2usa – I’m starting to get a feeling that commodities may get a move higher from this area

Gundlach on ETF.com:

- “Recently, you saw the commodities find a floor. But it remains to be seen whether that’s a floor or whether we’re going to decline again. It seems to me that commodity prices have probably bottomed, over the short term. And so, probably incrementally, the pressure on high-yield bonds in the short term is somewhat lessened”

8.1 Gold

Larry McDonald was explicit in his conversation on CNBC Trading Nation:

- “Anticipating Fed policy is not just about following US economy; it has a US economic component, a global economic component & a risk component … there is a rising chance the Fed has to push off a rate hike; last time Fed pushed off a rate hike, gold miners were up 25% in 3 months“

His segment-mate, Richard Ross, was openly contemptuous of Gold:

- “I have no use for gold at these levels and I would remain a seller here; technicals go from bad to worse; inability to get above the 100-day level; that 100-week moving average it held as a buy signal from 08 from 1000 to 1600; you are a seller on the break below itl inability to get back above that 100-week moving average; I would not buy Gold unless you can get back above that 100-wek at 1236 now; that would be a heroic move; lets be realistic; Gold is going to $1,000 and there is nothing in short term or long term charts that tells me otherwise“

George Gero of RBC was positive on CNBC Trading Nation:

- “Open interest, volume are showing me bottoming action in Gold; After Fed decision will probably rally because all the bulls are gone and only bears are left”

A notable trade this week:

- Wed – Joe Kunkle @OptionsHawk – $GLD trader bought 7,500 Nov. 107 straddles for $6.17, just failed at trend resistance, 95-98 can still be in play

8.2 Oil

The big news of the week is Goldman’s call of $20 price target in oil. As Jeff Currie explained to CNBC’s Brian Sullivan & Melissa Lee, the $20 target is not their base case. Their call is essentially a lower for longer call based on a huge surplus that cannot be closed merely by production cuts in high-yield companies. It has to come from bigger players, Currie said.

Jeffrey Gundlach took a different view in his conversation with ETF.com:

- “I’ve been of the opinion that oil would not rally very much, but it also wasn’t going to go to $20 like you’ve heard a lot of the real mega-bears talk about. And certainly, it seems like it has a hard time staying below $40; even seems to have a hard time staying much below $45.

- Is it going to start rallying? In a certain sense, I think yes, because I don’t think it’s going to fall. But that’s not really what’s important for the oil market. What’s important for the oil market is, will it stay below $60? If oil rallies up to $49, it doesn’t do a lot of good for the oil service companies and the oil producers. It needs to go higher than that.

- I don’t know if the tide has turned. If you define it as oil is going to stop dropping, that’s probably good. If you mean oil is going to rally up to a point where there’s no stress in the commodity economy, I don’t agree with that“

Two opposing views on Goldman’s call:

- A. Gary Shilling @agaryshilling – I’m glad to see Goldman Sachs has finally joined me in forecasting $20 per barrel #crudeoil prices

Shilling’s views were detailed in his article on Bloomberg.com. A dissenting view:

- StockTwits @StockTwits – The last time Goldman Sachs made a huge prediction about oil. The opposite happened: http://stks.co/h37Je $USO

Finally,

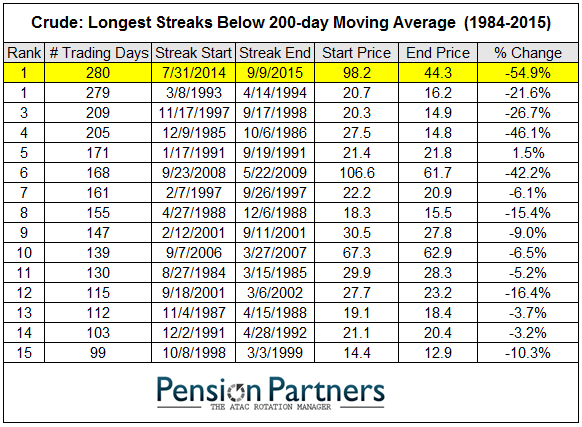

- Charlie Bilello, CMT @MktOutperform – Crude: this is now the longest streak in history below the 200-day moving average. There will be blood. $CL_F

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter