Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.All Time Highs & All Around Confidence

What a week? All major US indices at all time highs. That too with rates behaving themselves and Dollar actually softening! It is as if all is right with the Trumpian world. That is the reason for this week’s market rally, opined money manager Kourtney Gibson on CNBC FM 1/2 on Friday. Her reasoning was – the fact that President Trump was implementing what he promised gave certainty to the markets. That is quite possibly part of the story. Part of a deeper reason could be that President Trump is actually consolidating his support among his base:

- Financial Times

@FT – Donald Trump’s supporters see the new president as already delivering on promises made on the campaign trail

Equally important is the realization that he is simultaneously bringing towards him a big & pivotal section that has been the powerbase of the Democrat party – Leaders of Big Unions like James Hoffa of Teamsters

- “I mean, he’s only been in since Friday and look what’s happened,” Hoffa said. “I mean, it’s — he’s done amazing things.”

What amazing things? Renegotiating NAFTA & getting out of TPP. What happens when President Trump gets both the Republican social conservative base AND the Democrat labor union base enthusiastically on his side? He becomes impervious to congressional pressure on his agenda. And that lends a level of certainty to markets about their expectations of growth & reflation.

That may be why reflation trades enjoyed a resurgence this week and prompted even the smart skeptics to ignore the speculator long position:

- Raoul Pal

@RaoulGMI Copper long positions are off the map but the chart sure looks constructive…

2. Trump – Mexico, China & possibly Germany

The big story on Thursday was the mutual cancellation of the meeting between Pres. Trump & Pres. Nieto of Mexico. We could be wrong but we think Pres. Trump played Pres. Nieto. After meeting with the Mexico’s foreign minister, Mr. Trump signed his executive order that essentially laid down his marker & reaffirmed that Mexico will pay for the wall. The Foreign minister was aghast & President Nieto threatened to cancel his meeting. President Trump essentially said OK. Later that afternoon, the Trump team leaked a 20% border tax on imports from Mexico to pay for the wall.

President Trump could ride out the furor but President Nieto could not. After all, continuity of exports to USA is an existential requirement for Mexico. So the next morning, the two leaders spoke for an hour over the phone and discussions were back on track. There is little doubt in our mind that Mexico will essentially pay for the wall but only if it is kept private. President Trump then used his press conference with Theresa May of Britain to restate his core position about Mexico. Thus a lesson was taught we believe. Both the Peso & the Mexican stock market rallied after the announcement of the phone call.

Does that mean the following tweet was merely early? EWW, the Mexico ETF, closed up 5.8% on the week.

- Pension Partners

@pensionpartners Mexico relative to S&P. Has the low been made? http://www.pensionpartners.com/blog

This manufactured confrontation with Mexico’s President is a warning to President Xi Jin Ping of China just as the effusive praise of Brexit with the warm reception to British PM May is a warning to Germany. Perhaps the clearest exposition of this came from Kyle Bass on BTV:

What might precipitate a crisis in Germany, at least a crisis for today’s German attitudes?

- ian bremmer

@ianbremmer – Latest German Election Polls Angela Merkel, CDU: 41%, -2 since last month Martin Schulz, SPD: 41%, +5#GettingInteresting

3. Dollar & Rates

But the Dollar softened a bit this week and rates barely rose. Not only did the Dollar fall about 40 bps, it lost a champion. Rick Santelli said he was “much less bullish on the Dollar for the medium and long term“. Why? Because “it looks like a head & shoulders developing. … Left shoulder has developed & the head has developed … neckline is right around 100 … if you get a big close below 100 [on DXY] then with H&S top, we could be going back to 96-97 level which means Euro goes back to 110-111“.

Santelli does say Dollar might rally a little bit & that could easily happen if Chair Yellen talks hawkish next Wednesday. But what if she does & the resultant Dollar strength fades? Then we could indeed see 96-97. Ditto for rates. Despite the big rally in stocks (S&P up 1%, Nasdaq up 2% & Transports up 2.4%), TLT was only down 30 bps on the week. The reversal from 2.50% of the 10-year yield seemed significant to some:

- David Larew

@ThinkTankCharts – 10 year treasury yield – last gasp up reversal today – 24.89 critical support level. Failure at the swing with price, and RSI – one & done

4. Stocks

First kudos to Ryan Detrick for calling this week’s direction correctly last week:

- Ryan Detrick, CMT

@RyanDetrick – Jan 20 – Could there be a post inauguration sell-off? History says#SPX bounces for two weeks, then the big drop is in Feb. https://lplresearch.com/2017/01/11/could-there-be-a-post-inauguration-sell-off/ …

Now what? More & more voices are advising caution. Tony Dwyer or Cannacord Genuity is warning about a 4-7% correction which should actually be bought.

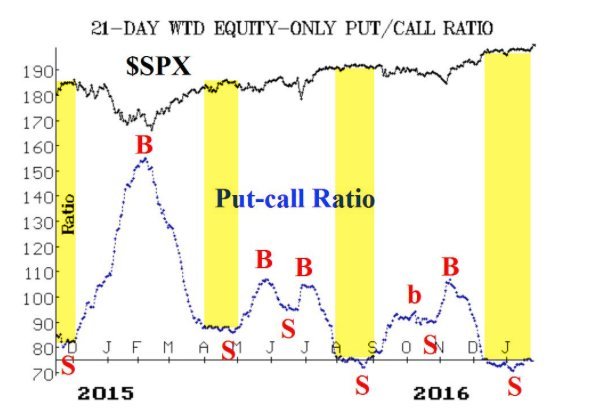

Tom McClellan came on CNBC to state that a correction is due & the top of the current rally will be on February 9.

- Urban Carmel

@ukarlewitz – McMillan: 21-d weighted equity-only put/call ratio$SPX

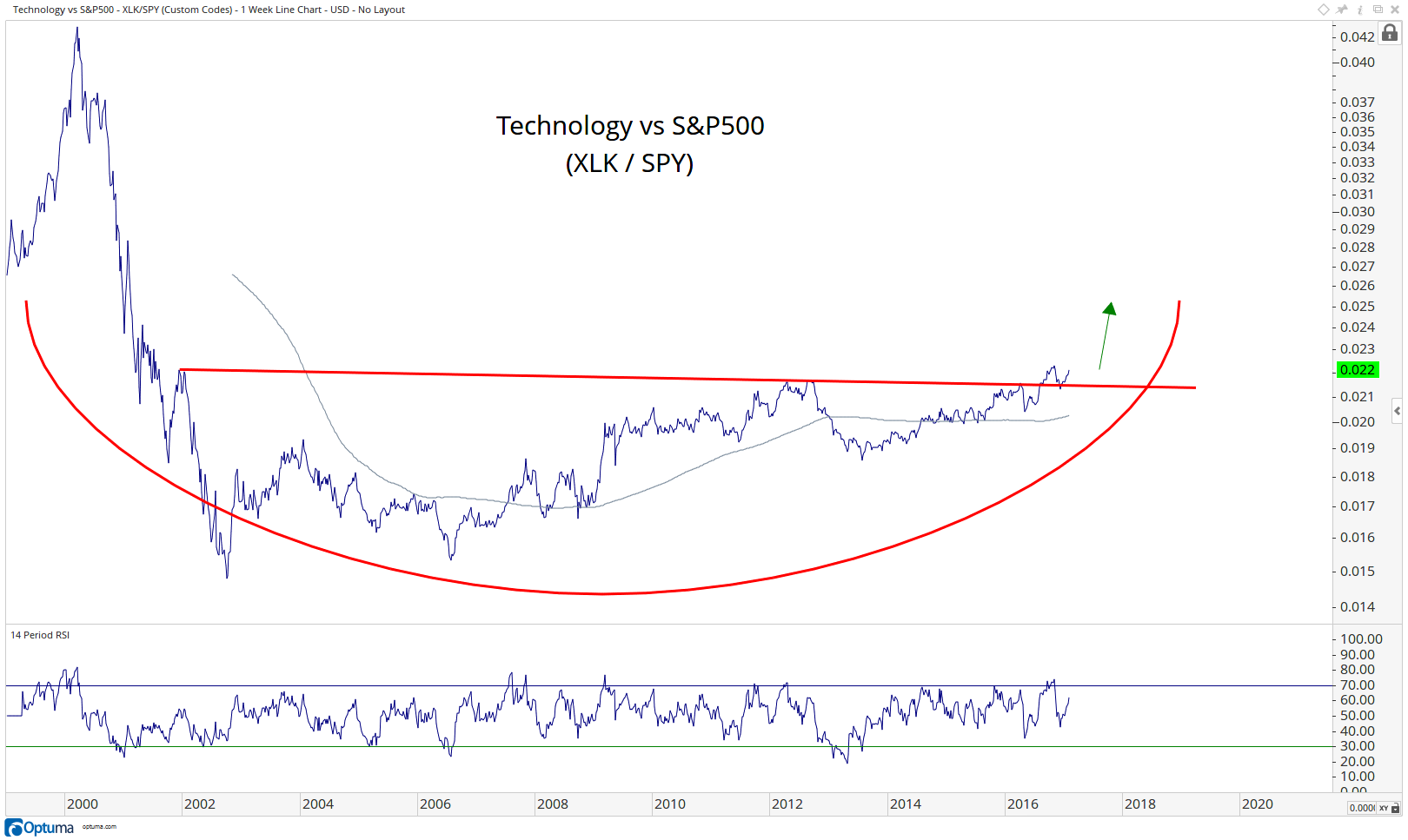

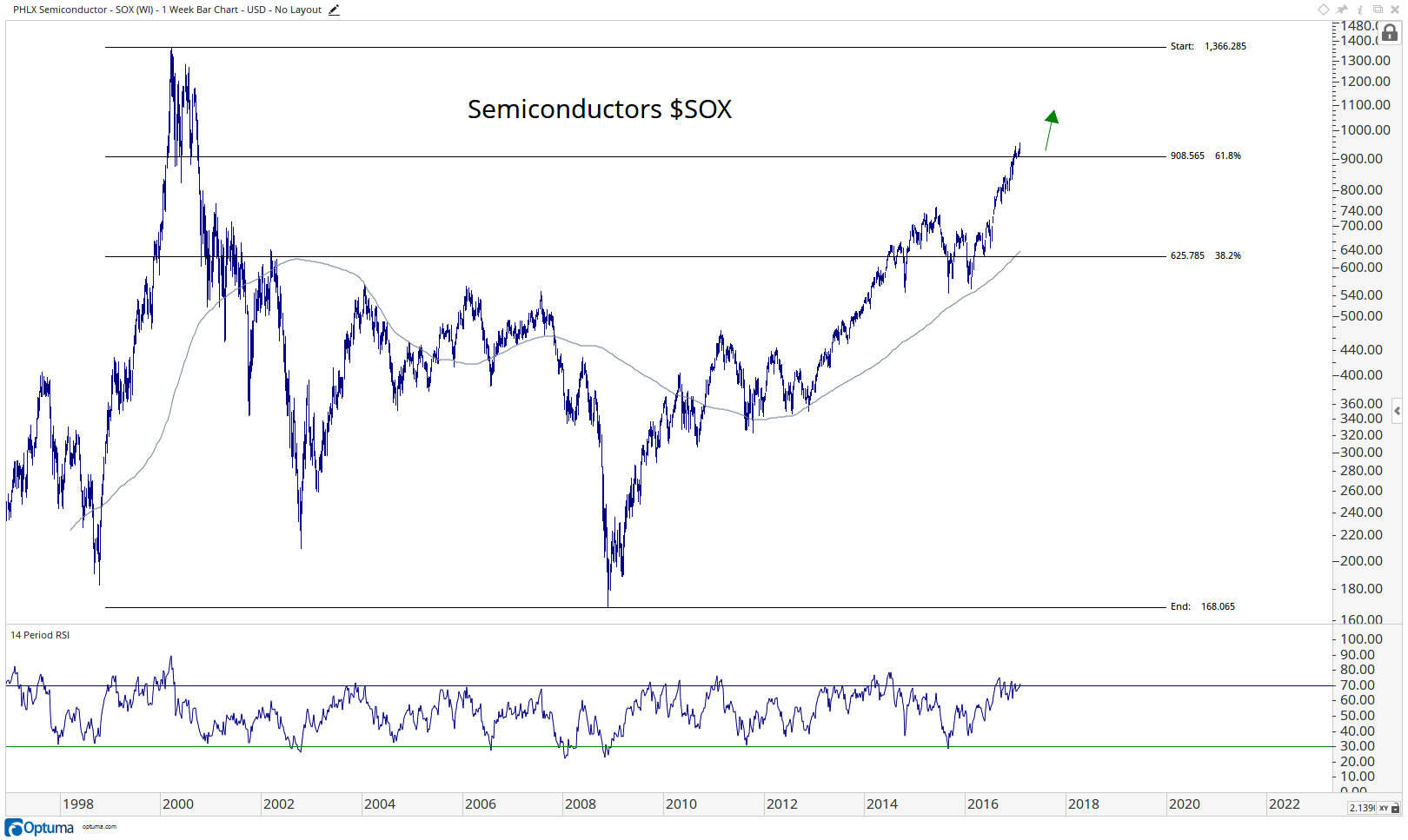

On the other hand, J.C. Parets wrote a bullish piece on Technology stocks, specifically semiconductor stocks. That usually means higher levels in S&P too.

- “This is Technology relative to the S&P500 breaking out of a decade and a half long base. “The bigger the base, the higher in space”, is how I learned it”:

- “Here is the PHLX Semiconductor Index breaking out to new 16-year highs this week. If Tech as a group is going to to retest those all-time highs from March of 2000, I would expect Semi’s to do the same. This is going to continue to be our tell. If we’re above 908 in the Semiconductor Index, we want to continue to err on the long side of chip stocks”:

What sounds almost crazy?

- Pension Partners @pensionpartners – Jan 24 – Make Greece Great Again? Potential early uptrend. $GREKhttp://www.pensionpartners.com

/blog

5. Oil

- Raoul Pal

@RaoulGMI#oil… the US Dollar Broad Trade Weighted Index is suggesting that oil should be at $30.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter