Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Does it matter?

By it we mean the economy & its direction. On Thursday, the strength of the job market stunned the market via the ADP jobs number of 253,000. The major stock indices rallied hard & closed at new all time highs. On Friday the weakness in the job market stunned the market via the Non-Farm payroll number of 138,000 with April revised downwards from 211,000 to 174,000. Treasury rates fell off the proverbial cliff but the major stock indices rallied hard and closed at new all time highs again.

Yes, different sectors rallied on Thursday & Friday but the indices couldn’t care less. Perhaps that is due to the Treasury market that seems to have the bit within its teeth. Yes, rates did move up a bit on Thursday after the big ADP number but that up move didn’t seem to have any vigor to it. And there was no doubting the strength of Friday’s down move in rates after the weak NFP number. The 10-year yield broke the 2.17% level and the 10-year yield, 30-year yield and TLT all broke through their 200-day moving averages. If this break is sustained next week, it could presage a serious move.

And a serious down move in rates would stay FOMC’s hand and wouldn’t that be great for small cap stocks, FANGs, Utilities? Is that why IWM rallied so hard in the last couple of days?

- Mark Arbeter, CMT @MarkArbeter – Very nice

$RUT consolidation after massive move. Never got oversold during pause, sign of strength. Ready to go topside once again?

And if the FOMC does stay the course and raise rates on June 14 as the market probability suggests, then wouldn’t that be taken as evidence of economic strength & propel resource & cyclical stocks higher?

Doesn’t the above discussion say something about sentiment about stocks?

- Babak @TN – Daily

#Sentiment Index S&P 500 87%, Nasdaq 86%,$VIX 10% starting to inch into extreme bullish territory$SPX$NDX$QQQ$SPY

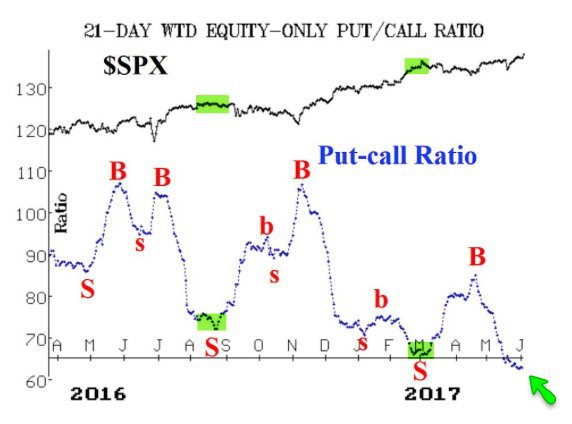

Given how resilient stocks have been, who needs protection, right?

- Urban Carmel @ukarlewitz – Weighted one-month equity-only put/call is at > 2-yr low (from McMillan)

$SPX

Perhaps exhaustion is what it would take to get a slowdown in the stock indices?

- Andy NyquistVerified account @andrewnyquist – June 1 –

$SPX – S&P 500 on bar 7 of a demark sell setup. If it continues, could see new highs Fri/Mon before Turnaround Tuesday…

2. Treasuries

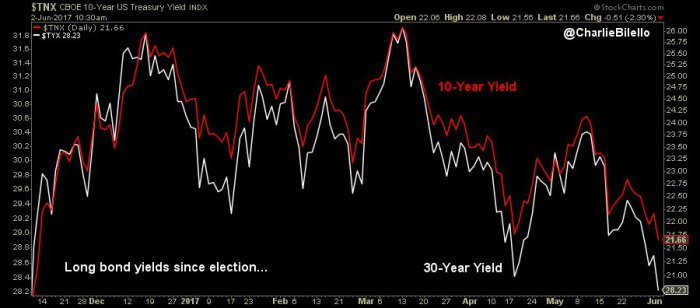

The entire Treasury curve melted down this week and flattened as well. The 30-year yield fell almost 11 bps, the 10-year yield fell 10 bps, the 5-year fell 7 bps while the 2-year only fell by 1.2 bps. As we wrote earlier, both the 30-year & 10-year yields broke through their 200-day moving averages.

- Charlie BilelloVerified account @charliebilello – US 10-Year and 30-Year yields move down to their lowest levels since the election.

$TNX$TYX

One way to look at this week’s rate action is:

- Alex Gurevich @agurevich23 22 minutes ago – I love that bonds are rallying while stocks are making new highs. Imagine $TLT when equities DO have a correction. #TheOneTrade

If Treasuries keep rallying, they would make a lot of people happy:

- Lawrence McDonald @Convertbond Short bets against US Treasuries climb to new record – FT on January 6, 2017 Today investors are net LONG 365k contracts – CFTC

One reason Treasuries are rallying could be:

- Chris Kimble @KimbleCharting – Inflation indicator continues weak and breaking support. Suggesting softness ahead?

$TLT$SPY$GLD$TNX

What might be one way to get higher inflation expectations & steepen the yield curve? For the FOMC to NOT raise rates on June 14. Because we know what will happen if they raise rates – the yield curve will flatten & the 10-year might go to 2% especially if the NFP number in July comes in weak as well. Already:

- TF Metals Report @TFMetals – If the Fed hikes again this month, they’ll have jacked short rates 75 bps while long rates have remained flat. #gold #recession

The above chart might be the best visual reason why the FOMC should not raise rates on June 14. They don’t have to sound dovish; they can simply dismiss the recent weakness in data with their new favorite word – “transitory“.

For us, it is pretty simple. If Friday’s break of 200-day moving average by the 10-year & 30-year yields is sustained, then yields will begin a new down leg. If they bounce back, then the range can be maintained. It might take a lot though to get the 10-year yield back to 2.40% let alone 2.60%.

3. Upsetting the carts?

Last week we broached the topic of an unexpected Dollar rally. Lo & behold, Jim Cramer on this Tuesday devoted s segment to the case of a serious Dollar rally via the opinions of his colleague @fibonacciqueen Carolyn Boroden. Best to hear the reasons from him:

The big event next week is the election in Britain. That might create some volatility in currencies. And then if the FOMC stays its hand the following week, that might be Dollar positive.

We don’t have a clue what might trigger a Dollar rally but if we do get one then that might just be what creates some volatility in stocks & rates.

4. Stocks

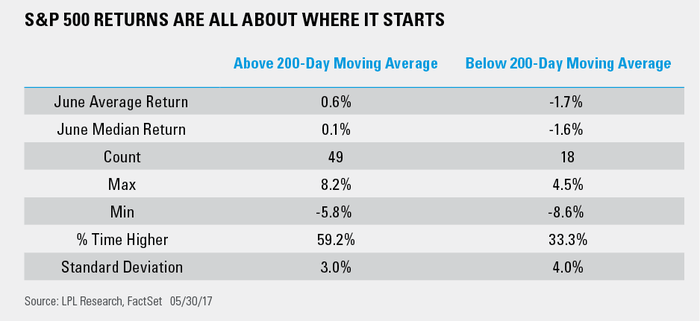

Getting back to US Stocks, what about a June Swoon?

- Ryan Detrick, CMT @RyanDetrick Time for a

#JuneSwoon? Depends where you start, if#SPX starts above the 200-day MA it is higher 59% of the time … https://lplresearch.com/2017/05/31/lets-talk-june-swoon/ …

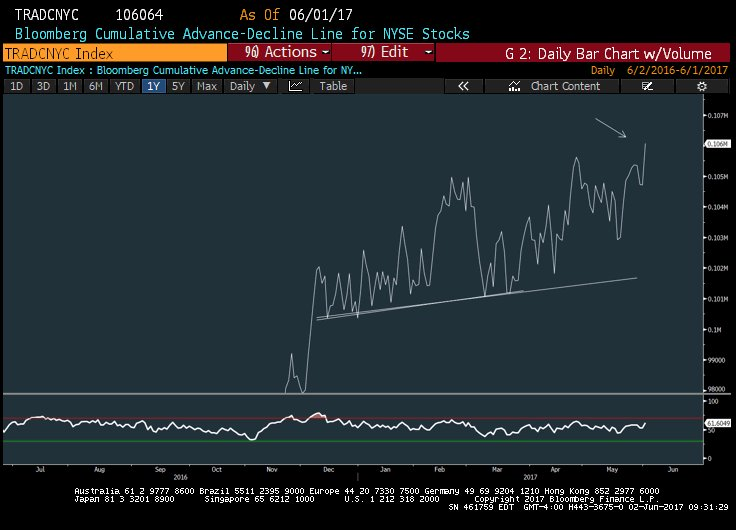

And do stocks top out when the Advance-Decline line is making new highs?

- Mark Newton @MarkNewtonCMT – Advance/Decline A/D (All Stocks) back to new all-time highs as of this week

On the other hand,

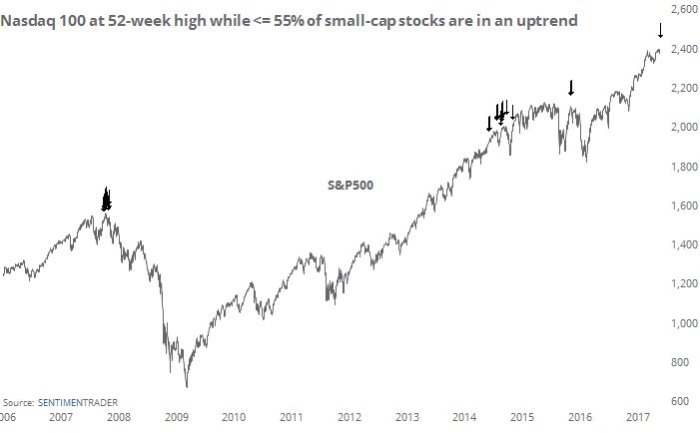

- SentimenTraderVerified account @sentimentrader – Here is every time in past decade when big-cap tech reached a new high and barely half of small-cap stocks were in a bull mkt.

5. Gold

Gold and Silver both rallied by about 1% but Gold Miners fell. Is that a bearish divergence? Carter Worth, resident technician at CNBC Options Action and a new bull (as of last week) on Gold said on Friday that there was “plenty more to go” in Gold. And,

- Chris Kimble @KimbleCharting – Gold indicator, nears first buy signal in 6-years https://www.kimblechartingsolu

tions.com/2017/06/gold-indicat or-nears-first-buy-signal-6-ye ars/ …

Not every one is bullish on Gold:

- See It Market @seeitmarket NEW Blog: “3 Reasons Why I’m Neutral On Gold Prices” – https://www.seeitmarket.com/3-reasons-why-im-neutral-on-gold-prices-gld-16913/ … by

@MarkArbeter$GLD$EURUSD$TLT

6. Oil

Oil fell by 4% this week and Oil ETFs fell hard as well. Carter Worth who has been clearly contemptuous of oil remained so this week. On the other hand, strategist Tom Lee reiterated his bullishness on Oil & Energy stocks:

- Trading NationVerified account @TradingNation – Last 4 times #oil did this, huge rallies occurred, & it’s very close to doing it again: Tom Lee http://cnb.cx/2rIjW0x via (@stephlandsman)

- “We’re approaching a flip back into backwardation, meaning the spot price is approaching and may soon exceed the 24-month contract. That’s normally a market imbalance,”

- The last four times oil moved into backwardation, the commodity rallied between 25 percent and 72 percent in the next nine months, according to Lee.

Send your feedback to editor@macroviewpoints.com Or @Macro Viewpoints on Twitter