Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Tariffilocks

The week’s message was very clear. Monday was a down 95 points day because of fear of President Trump’s decision due that evening. The tariffs announced were 10% on the first tranche of exports from China. The next morning, the feared retaliation from China was dovish. So the big & feared US-China event risk turned out to be Tariffilocks, a lame term for Goldilocks version of the feared tariffs.

Look what the Dow Jones Industrial Average did the next four days – up 185, up 159, up 251 & up 86.5 points on Friday to close up 2.3% on the week to a new all-time high. The Dow blew away the 86 bps rise in the S&P. All other major averages, Nasdaq, Nasdaq 100, Russell 2000 & Dow Transports were down on the week.

This action made perfect sense to Mohamed El-Erian who tweeted:

- Mohamed A. El-ErianVerified account @elerianm – Tue Sept 18 – With the #Dow up 200 points post #China #trade retaliation, many attribute this to lower than expected #tariff rates (10% vs 25%). While this is true, there’s also a bigger issue here. #Markets believe that the tit-for-tat will ultimately result in a still free but fairer system.

This Tariffilocks rally was even more evident in Chinese market ETFs which closed up 6% on the week with, EEM, the broad EM ETF, up 3% on the week.

- John KicklighterVerified account@JohnKicklighter – This will be quite the technical position for the

$EEM to start off next week. How much enthusiasm do we have for risk taking?

But isn’t this 10% on $200B of exports only the first step? What about the second step of tariffs on $267 B of Chinese exports? That was forgotten by most this week with the exception of Larry McDonald of ACG Analytics. Based on what he heard from the DC leadership, he said on Friday:

- “the situation with China has deteriorated to really atrocious levels; even in areas like intellectual property where US has China dead to rights, an area in which they can at least admit they can move towards the US to an agreement, they are NOT working on anything. So I think tariffs on $267 B – we are going to get that probably in next 10 days & many of those tariffs affect technology, supply chain of semiconductors; there is more pain to come; President Trump is using the market as dry powder; we are making new highs here; he is going to push China harder & harder ..”.

But that is ten days away, right? So at least for that period, 3 of the 4 event risks we identified two weeks ago, China-US tariffs, EM liquidation & conflict in Idlib, Syria seem dormant at least in the very near term. That leaves the No. 1 event risk we had identified.

2. FOMC meeting & Interest Rates

This meeting might prove to be an important one. A rate hike is likely to put the Federal Funds rate above the inflation rate, meaning the real FF rate will finally become positive. And if Fed affirms their previous dots to suggest 3 more rate hikes in 2019, then the real FF rate will get to 100 bps in 2019.

Why is this important? On Wednesday, September 19, Ruchir Sharma of Morgan Stanley Investment Management said clearly both in his NYT Op-Ed and in his clip below that a FF rate at or above 100 bps has always created market turmoil. And given that markets are now 3X the size of the global GDP, a severe turmoil in global markets is likely to create blowback on the global economy.

In more detail, excerpts from Sharma’s NYT Op-Ed titled How the Next Downturn Will Surprise Us:

- By the eve of the 2008 crisis, global financial markets dwarfed the global economy. Those markets had tripled over the previous three decades to 347 percent of the world’s gross economic output, driven up by easy money pouring out of central banks. That is one major reason that the ripple effects of Lehman’s fall were large enough to cause the worst downturn since the Great Depression.

- Today the markets are even larger, having grown to 360 percent of global G.D.P., a record high … Now, the markets are so large it is hard to see how policymakers can lower the risks they pose without precipitating a sharp decline that is bound to damage the economy. It’s a familiar problem: Like the big banks in 2008, the global markets have grown “too big to fail.”

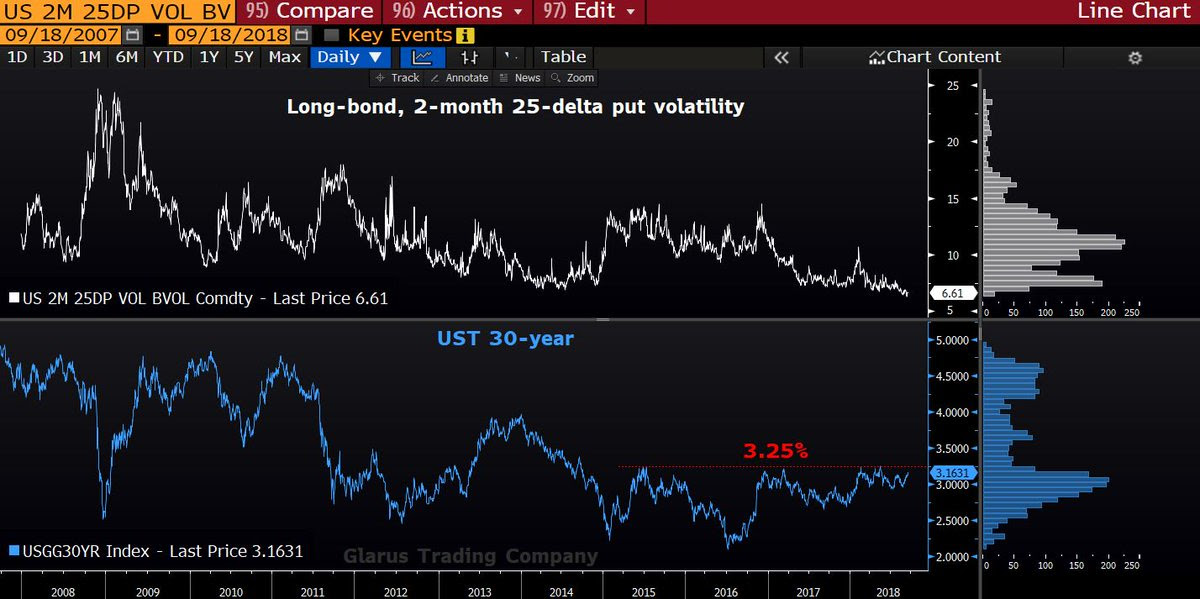

How quickly can markets move? Look what happened to interest rates on Tuesday & Wednesday? In a vicious bear-steepening of the Treasury curve, the 30-year yield jumped 8.2 bps in 2 days, the 10-year yield jumped 7.7 bps while the 2-year yield rose by only 1.7 bps. The 10-year yield went through 3% like a hot knife through butter and the 30-year yield closed on Wednesday at 3.23%, perilously close to the 3.25% level:

- Jeffrey GundlachVerified account@TruthGundlachYields: On the march! 10’s above 3% again, this time without financial media concern. Watch 3.25% on 30’s. Two closes above = game changer.

But is this a storm brewing?

- Jack Rodeghier@glarustrading – Keep a close eye on 3.25% in bonds. Perfect storm brewing whereby higher issuance, trade-war dynamics (impacting China Tsy demand) and inflation are in a delicate equilibrium. Put volatility in the deepest post-GFC tail, that’s apt to change QUICKLY if/as bonds breach 3.25%.

The fever of the up move in rates on Tuesday & Wednesday was interesting. Some, like CNBC Options Action, talked about rumors of Chinese selling Treasuries. But the fever seemed to pass on Thursday when a portion of the move was reversed.

The fever of the up move in rates on Tuesday & Wednesday was interesting. Some, like CNBC Options Action, talked about rumors of Chinese selling Treasuries. But the fever seemed to pass on Thursday when a portion of the move was reversed.

But these rumors of Chinese selling and the harsh reaction in rates may be unsettling to the Fed. While the Fed does want to raise rates, we wonder whether they are somewhat concerned about abetting an unstable condition in interest rate markets. And the move has opened a divergence between inflation expectations & the 10-year yield:

- Holger Zschaepitz @Schuldensuehner – US 10y yields rise to 3.08%, have totally decoupled from inflation expectations.

Remember Greg Harmon of Dragonfly Capital who warned on August 31 about Bonds Hanging on by the Fingertips. He has correctly warned about Treasuries twice already. So what did he say this Wednesday?

- Greg Harmon, CMTVerified account @harmongreg Sept 19 – Dragonfly Capital – Bonds approaching Death Zone…..again http://dragonflycap.com/bonds-

approaching-death-zone-again/ … $TLT

- The death zone is the name used by mountain climbers for high altitude where there is not enough available oxygen for humans to breathe. This is usually above 8,000 meters (26,247 feet). Most of the 200+ climbers who have died on Mount Everest have died in the death zone. For Bonds that level is a price of 115.25 in the 20+ year Bond ETF, $TLT. … Since the beginning of September prices have been moving lower in that range and are now approaching the bottom at 116. Below that there is a little room to the Death Zone at 115.25 from July 2015.

- Momentum is making new lows as the price continues to fall. The RSI is nearing oversold territory but the MACD is only barely negative, with lots of room to move lower. As I write in the pre-market the price is off further and. It is outside of its Bollinger Bands® so there may be an oversold bounce in the short run. What happens after that will be telling and may bring forward the long talked about Bond correction.

By Friday, some others were willing to bet on a bounce. Specifically, the trading team at CNBC Options Action recommended a November 117-122 call spread in TLT.

.

Frankly, we can’t wait for FOMC statement & presser on Wednesday September 26.

3. Stocks

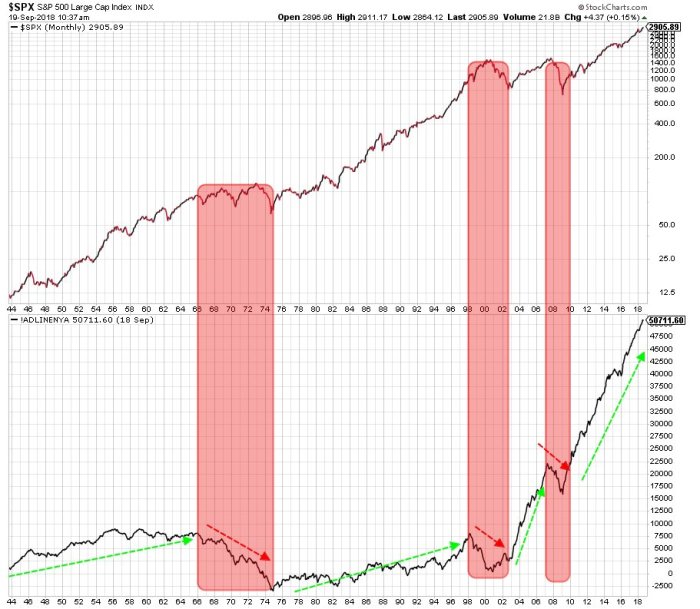

- Ryan Detrick, CMT @RyanDetrick – Ei mate, arrrrrren’t you glad the NYSE AD line continues to suggest the bull market is alive and well?! This is a broad based advance that isn’t just on a peg leg, plenty of support under the surface.

#TalkLikeAPirateDay

What about institutional cash levels?

- Ryan Detrick, CMT @RyanDetrick The BAML/MER Global Fund Manager Survey has cash at an 18-month high. If you were looking for what could drive stocks higher, there it is.

And optimism?

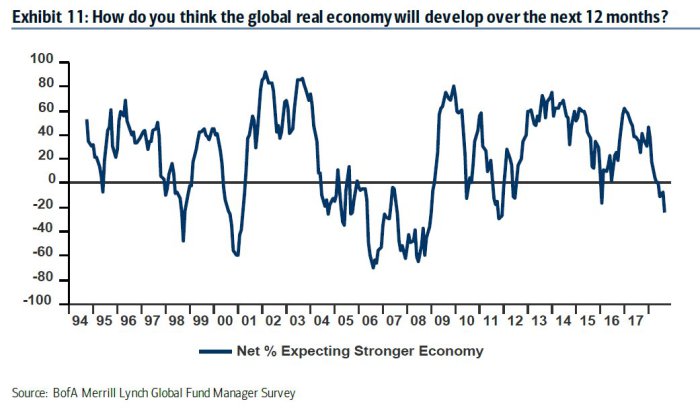

- Ryan Detrick, CMT @RyanDetrick According to the BAC/MER Global Fund Manager Survey, investors are at a 6-year low in global growth optimism. Contrarian?

On the other hand,

On the other hand,

- Urban Carmel @ukarlewitz –

$SPX hitting slatty lines

Also,

Also,

- Igor Schatz @Copernicus2013 – Reminder that September

#OpEx week is the most bullish opex week for the year.. while the following week is the most bearish of the year

Emerging markets enjoyed a hard bounce this week. Not only were Chinese ETFs up 6%, the Brazil ETF, EWZ, rallied 8% on the week. The exception were the Indian ETFs which were down 3% on the week. This week Goldman downgraded the Indian stock market on valuation concerns & the prospects of a difficult election next May. A hard decision by the Reserve Bank of India to sanction heads of a major private bank led to a 24% decline on Friday in Yes Bank stock and took down the broad indices as well.

We applaud the Reserve Bank for this & similar strong steps. Such steps are the basis for our belief that the NPL (Non-performing loans) problem for Indian banks has already peaked. This is similar, we think, to the S&L problem in American banking in 1990. The harder & harsher the RBI gets, the faster the medicine will clean up Indian lending & begin a virtuous cycle in the economy.

4. Dollar, Oil & Gold

The US Dollar was down about 75 bps this week despite the tariffs imposed on Chinese exports. Now comes the FOMC meeting, an event that could move the Dollar. With the Dollar, come moves in commodities, especially Gold & Oil.

Gold was up about 33 bps this week but Gold miners were up hard with GDX up 4.4% & GDXJ up 4.9%.

- Peter BrandtVerified account @PeterLBrandt – Mon Sep 17 – The last time Commercials were net long and Large Specs were net short Gold was Nov 2001 when Gold price was sub $300 $GC_F $GLD Daily chart potentially constructive.

What about Oil?

What about Oil?

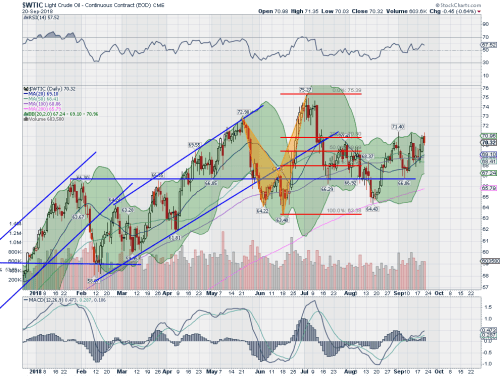

- Greg Harmon, CMTVerified account @harmongreg – Dragonfly Capital – Oil Gusher https://tmblr.co/Zjsg5q2c48R1f

$CL_F$USO

- The chart below shows bottom, at a higher low than the June bottom, and reversal. It has moved higher since and was having trouble breaking above resistance at 71. On the third push, it broke higher on Wednesday. Will it continue? The chart suggests it quite well could.

- Momentum is building and already positive. The RSI is knocking on the door of a move over 60 and the MACD is positive and rising. The Bollinger Bands® are also squeezed, often a precursor to a move, and now starting to open higher. It has turned higher in pre-market trading Friday and now has its next resistance over 71 at 72.80. A break there sees only the June high in the way of a move to the 80’s.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter