Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.“my fear is he doesn’t”

A number of people expressed their disenchantment with Fed Chairman Jay Powell this week. Several said this sell off was the Fed’s fault. Some attributed Powell’s comments to inexperience or a lack of seasoning. David Zervos said Powell’s “ego got in the way; Powell was too stubborn“. Jim Cramer was naturally the most explicit saying “I need to the Fed to shut up; I don’t trust the Fed at all; Jay did everything to cause this tremendous sell-off … He did the country a great disservice … Fed is being recklessly imprudent“.

We are afraid the problem is much deeper. Read what Jim Bianco said on CNBC Closing Bell on Thursday:

- “he has the wrong approach; he thinks balance sheet reduction on autopilot is something separate from monetary policy; it is a form of tightening; the market believes it is 1.5-2 rate hikes alone – just the balance sheet reduction; then they are going to do another 2 (rate hikes); that’s 4 rate hikes; the market is worried that’s too many; then you come out & say look we are going to autopilot 1/2 the rate hikes that we are going to do next year in the form of balance sheet; that’s why it sold off; I hope they understand this is a form of tightening; that’s what we saw in the Williams interview on Friday; he didn’t get it either & the market sold off; I hope they get it now; my fear is he doesn’t;

We think Bianco is right. What we saw of Chairman Powell during his presser is a stubborn attitude with a devotion to lagging indicators. He may think it is merely enough to say they are data-dependent without showing the markets any worry about the decelerating economy.

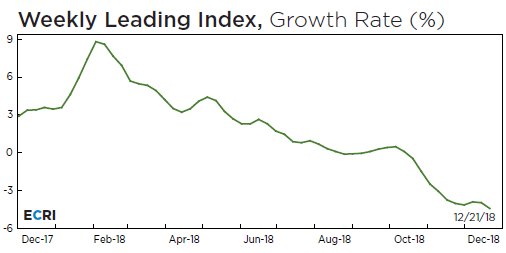

- Lakshman AchuthanVerified account @businesscycle ECRI U.S. Weekly Leading Index growth fell to -4.4%, a 199-week low. Read more and download the WLI for free here: https://goo.gl/tNCXyp

#economy

A more explicit way of putting it is:

- David Rosenberg @EconguyRosie Housing contracting; Non-res contracting (esp in shale patch); Capex contracting; Trade deficit expanding; Inventory building (pre-tariff) unwinding; Consumer spending plans rolling over; Fiscal gridlock. No recession in ‘19, eh?

A particularly malignant byproduct of a recession or semi-recession is the possibility of contagion.

- Lawrence McDonald@Convertbond – We must review credit markets since the Fed rate hike, it’s imperative. These are Senior Bank Loans BKLN, for weeks there was little price discovery, they held up well while investment grade bonds were FAR weaker. Since the Fed meeting, credit market freeze, see contagion here.

This has been our concern even before the “autopilot” declaration & the last FOMC meeting – that the Fed will again be too little too late in both recognizing the spread of contagion & taking aggressive steps to chemo it.

The Sovereign bond markets are sensing it even though the Fed doesn’t. The Japanese 10-yr yield closed negative on Friday bringing the entire 1-10 year JGB curve into negative yield territory. And the 1-year Treasury yield closed 7.3 basis point higher than the 2-year Treasury yield; 9.3 bps higher than the 3-year Treasury yield and 3.6 bps higher than the 5-year yield.

How can the 1-year Treasury yield be higher than the 5-year yield, higher than the entire 2-5 year Treasury curve UNLESS it is a scream to the Fed to cut rates NOW & stop the QT. Even a Powell admirer like Rick Santelli said on Friday ” we are melting” in yields and added “markets thinking less Fed“. Note that Santelli said yields were melting on Friday afternoon during a 100+ point rally in the Dow and during the 3rd day of an explosive rally in the US indices. Shouldn’t rates have gone up during such a rally? Instead they melted down as Santelli said. So would it be ok for Chairman Powell to merely profess commitment to data dependency next week after a clear cut weekly close inversion in 1-2, 1-3 & 1-5 yield curve?

Yields didn’t merely invert at the short end but the 2-year & 3-year yields fell by 12 bps & the 5-year yield fell by 8 bps. In contrast, the 30-year yield closed virtually unchanged on the week.

How should the Dollar react when the “markets are thinking less Fed“, to use a Santelli term? J.C. Parets answered by writing U.S. Dollar breaks down: So what is the impact according to him?

2. To “C” or Not To “C” – US stocks

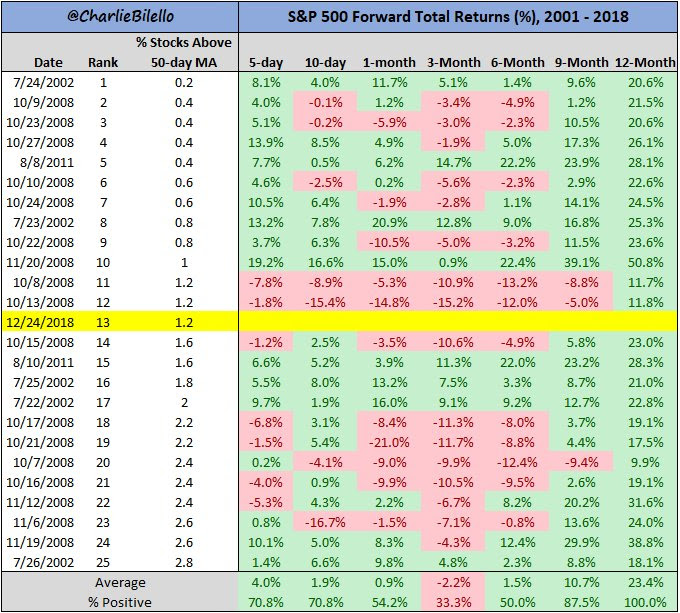

To watch the carnage during the last two hours of trading on Monday was something. We shudder to think what might have happened had Monday been a full day. What happens to the S&P after such an extreme oversold state?

- Charlie BilelloVerified account @charliebilello – S&P 500 entered the day at one of its most extreme oversold levels in history. From similar extremes since 2001: stocks were higher 100% of the time 1 year later with an avg return of 23%. $SPX

Does that mean we should jump in & buy next week? Not necessarily per the table above. Look at 10/8/2008 entry above. The 1-year return from that date was only 11.8%. Now scroll up and look at 11/20/2018 entry. The 1-year return from that day was 50.8%. That means the starting point on 11/20/2008 was way way lower than the starting point on 10/8/2008. How important was waiting for that extra 5-6 weeks?

Is there a message in there for this time? Yes, if you believe what Carter Worth of CNBC Options Action said on Friday that “all goes haywire in January“.

On the other hand, for short term folks:

- Andy NyquistVerified account @andrewnyquist – $SPY Two “hammers” in a row. Long lower shadow w/ close at highs. #IBDpartner Bounce likely to hold into next week. Upside targets include 38.2% Fib at $2519 and 50% Fib at 2573. @MarketSmith — http://ow.ly/Fzzt30lnZZt

Without feigning a Hamletonian (or is it Hamletesque?) manner, the big question for 2019 is whether the credit markets get seized with a contagion or not. If Fed demonstrates activism and contagion is avoided, then 2019 could be resemble 1995. Remember Greenspan killed inflation with his tightening campaign in 1994, slowed the economy to goldilocks level & cut interest rates in 1995. Well, Powell has already put inflation to sleep, he has slowed the economy already. Now all he has to do is cut rates. Then credit would rally and the stock market would do its thing.

But what if contagion does spread in credit & the economy? Things will still work out eventually. But what could happen between now & eventually will have to be experienced not predicted.

3. “Animal Spirits Kindled“

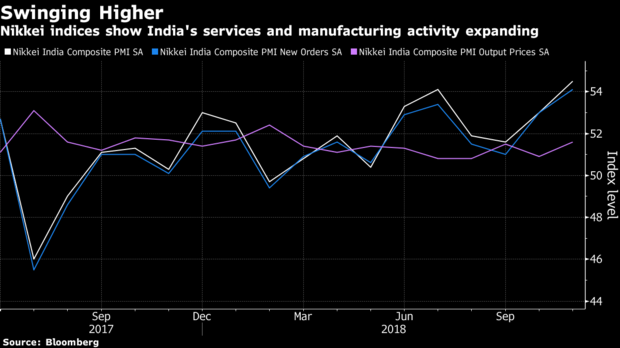

A month ago, outlook for the Indian market & economy looked bad. The Head of India’s Central Reserve Bank was locked into a dispute about monetary policy with the Indian Government. Liquidity conditions were tight & confidence in financial markets was low.

Then the Head of the Central Reserve Bank resigned and was replaced by a veteran appointee with a proven record of merging different viewpoints into a common purpose.

This week, Bloomberg reported that their “animal spirits” indicator used to measure overall activity also showed signs of a rebound in liquidity and increased lending. The article reports:

- “Inflows of new work expanded at the fastest pace in over two years, supporting further job creation and an uptick in business confidence. The picture for prices was mixed as input-cost inflation hit a seven-month low, but firmer demand enabled firms to hike their charges to a larger extent.”

This continues to show up in the Indian stock market.

(INDY vs. SPY – last 2 weeks)

Isn’t this a lesson for all central bankers? They may be independent but they are not disjoint. Working together with the Treasury department is a good thing as Alan Greenspan & Robert Rubin demonstrated in 1995.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter