Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.What a week?

Economically speaking,

- Jim Bianco@biancoresearch – A lot has happened THIS WEEK … economically speaking we had • Terrible global PMI • Terrible German ifo business confidence • Awful South Korean Exports • Giant dive in US Consumer confidence • Disappointing US consumer spending. Not a good week for the global economy.

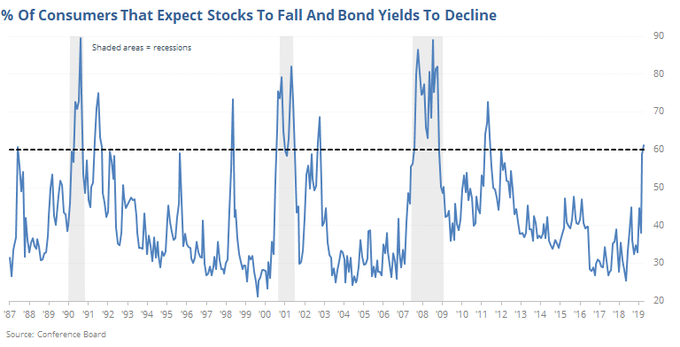

Giant dive in confidence means giant up move in falling confidence, right?

But what about the impeachment talk that is the rage on TV? Is this vengeance finally to be realized or is it the second coming of Mueller?

- Jim Bianco@biancoresearch – Despite rampant impeachment talk, Trump is still trading in the low 40s, like he was before this started. Not much change. Note volume is a record. So, traders are exchanging lots of money on this mkt is not really moving. Election 14 mos away, still a coin toss election.

But what are the chances of both impeachment and conviction in the Senate?

- Jim Bianco@biancoresearch– – Impeachment is like an indictment. To be removed, 2/3s of the Senate must vote to remove (which means 20 Republicans assuming all Democrats). Another market just started yesterday puts the betting on conviction and removal at just 13%.

The Mueller report dragged out the investigation for a year & half. But does this impeachment inquiry, based on one phone conversation between President Trump & the President of Ukraine, is capable to being dragged out for another year? Sorry, we forget. This impeachment inquiry is about the “cover-up” and not about the actual call, right?

No wonder the stock market is yawning through all this. But the side effects are the ones that cause trouble, right? Now that Senator Elizabeth Warren is shooting past VP Joe Biden in polls, does President Trump see the need to get to her left on China?

But what about President Trump’s focus on a strong stock market? It might be different against Senator Warren. Given that Democrats on Wall Street are threatening to sit out the 2020 Warren-Trump election, President Trump has enough ammunition to suggest a fall in the stock market is due to fear of Warren. That might be the reason for the sudden revelations of discussions about delisting Chinese ADRs in the USA & restricting US portfolio flows into China.

We remain in the camp of Kyle Bass who said weeks ago that President Trump will not approve a trade deal with China. Any deal he gets would be blasted by Senator Warren as a sell-out of American middle class & no deal with be passed by the House anyway. We expect President Trump will put substantial pressure on Democrats by accusing them of being anti-Hispanic for not ratifying the USMCA.

Finally, we wonder whether this impeachment kerfuffle gives President Trump an out for an economic slowdown & actually forces the Fed to be much more dovish than they wanted to, an out the voters might concur with.

But doesn’t the Fed need a slowdown in US Jobs Growth to get really dovish?

2. U.S. Job Growth & the Economy

- Lakshman Achuthan@businesscycle – – The U.S. jobs slowdown is important. More on ECRI’s call here: bit.ly/2liIN9K

What does that article say?

- “Year-over-year nonfarm job growth is at an 8-yr low. Meanwhile, ECRI’s U.S. Leading Employment Index growth has already plunged to a 10-yr low, pointing to further slowing in job growth ahead. This can weigh on consumer spending, which is the last pillar supporting the U.S. economy now that manufacturing is slowing sharply.”

Watch the full interview, the article says.

That brings us to,

- Richard Bernstein@RBAdvisors – – Everyone focused on the strong #consumer. However, Conf Board’s Employment Trends Indicator leads payroll #employment and the ETI just turned negative.

If the Fed is lucky, next Friday’s NonFarm Payroll would come in weak, thus making it easier to lower rates at the October FOMC meeting. But what if, next week’s job number is strong? Now imagine that happens & the Fed remains hawkish at the October FOMC and then, the November number comes in bad. Readers should look back at the aftermath of the FOMC meeting on October 31, 2007. The downturn began the next day on November 1, 2007.

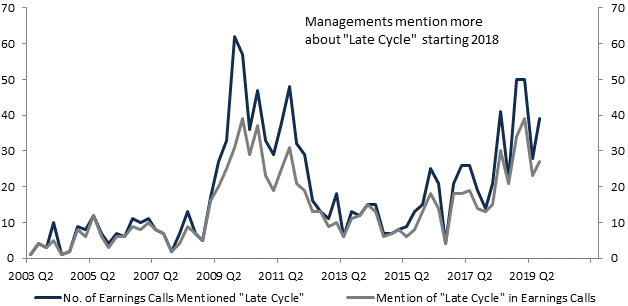

Can the Fed still maintain that we are in a mid-cycle adjustment?

- Richard Bernstein@RBAdvisors – – The #Fed might believe the #economy is in mid-cycle but companies increasingly believe it’s late cycle. (Chart: ISI)

And don’t company managements decide to postpone capex & other initiatives if they believe the US Economy is in “late cycle” stage? Does that make more likely that rates fall instead of a rise in rates?

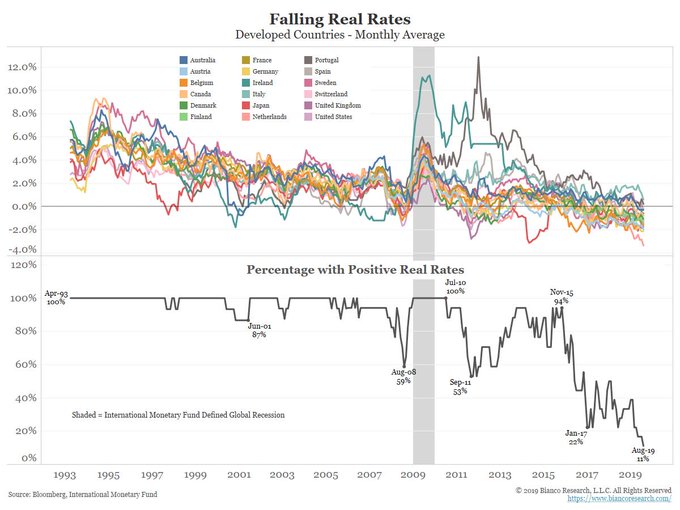

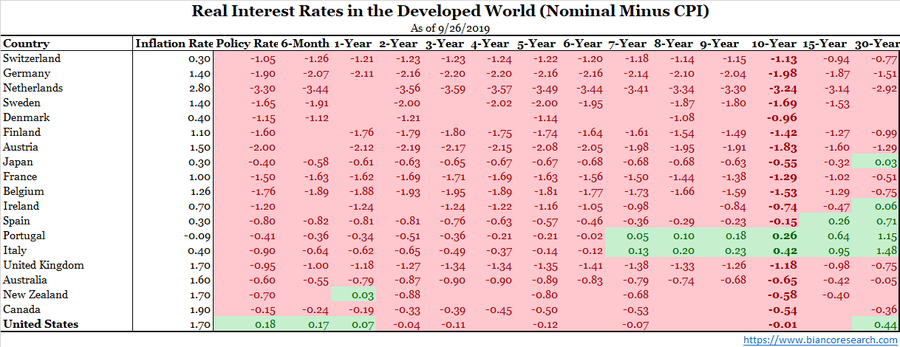

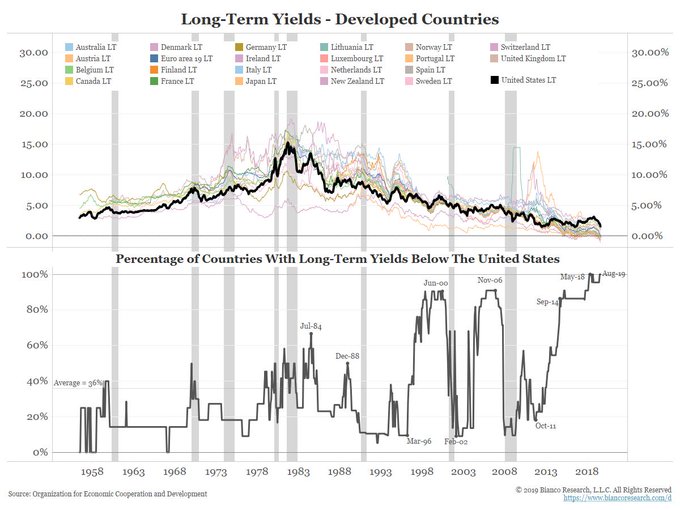

- Jim Bianco@biancoresearch – – Real Rates are negative everywhere (table). This is rare (chart) Aging population creating a massive bid for bonds. Get used to these low rates (negative real rates). They are not going away. One day we will look back and realize 2% 30-Year Tsys is a “massively large yield.”

You know, we found a NY Muni Bond maturing next year that was issued 15 years ago with a 4.375% triple tax exempt yield. Man, wasn’t that period a valhalla for high investment grade yields? Why didn’t everybody buy 15-year Muni Bonds in 2006 & sit on them? We can’t find such yields now, can we?

Actually you can but at the cost of guaranteed maturity. They are called Closed End Muni funds and old dictum says buy them when the Fed is done raising rates. The old bond king, Bill Gross, used to recommend these in the Barron’s round table. Look how $PNF from Pimco has done year-to-date:

PNF closed 2018 at $11.70 & closed this Friday at $14.39, a 23% gain in price that matches or slightly exceeds the price performance of SPY. And, PNF has paid monthly triple tax exempt dividends every month. And today’s yield for PNF is 4.42%, triple tax exempt of course. BlackRock, Nuveen, Eaton Vance & others have such closed end Muni funds as well.

The high yields come from leverage of about 35-40%. That is why they perform great AFTER the Fed is done raising rates, thanks to their borrowing costs going down & yields getting more valuable.

But the high monthly yields do protect investors to some extent even during rate rise cycles when borrowing costs rise & long maturity bonds decrease in value. Look at the 2-year chart of PNF that includes the 8 rate hikes by Powell FOMC – about 10% price gain over last 2 years PLUS 4.5% triple tax exempt yield = about 10% annual return for last 2 yrs even without tax benefit.

Sadly, no one on Fin TV even knows about these well-known funds. So their viewers miss out.

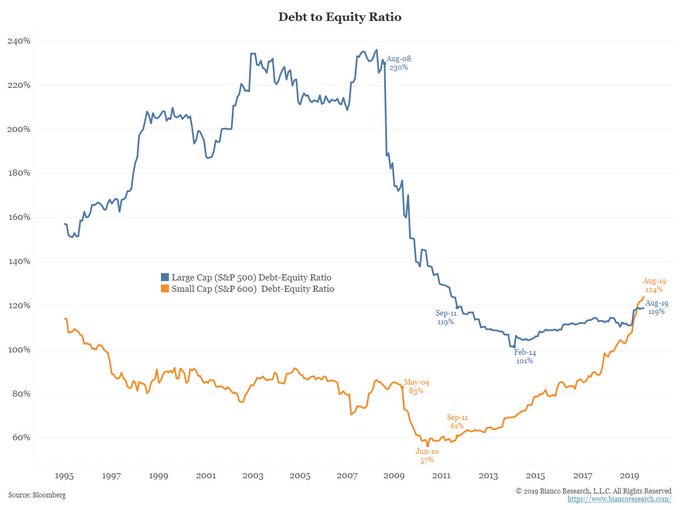

Now, even at the cost of making this article a Bianco Special issue, look at a sensible reason for under-performance by small cap stocks.

- Jim Bianco@biancoresearch – The US has the highest LT rates In the dev world. Multi-nationals can evade by funding their overseas operations in different currencies. Small cos cannot and are borrowing more aggressively than large cos. They are at a competitive disadvantaged. US rates are too high. (our emphasis)

What about S&P you ask? All we will do is relay what Lawrence McMillan of Option Strategist wrote in his Friday summary:

- “In summary, this is still a generally negative period, seasonally (late September into October), and this is usually a period of rising volatility as well. But our indicators remain bullish at this time, and only an $SPX move below 2940, accompanied by a $VIX move above 17 would change this bullish picture to a bearish one.“

Remember the great buy now call of Larry Williams communicated by Jim Cramer on Tuesday, August 27, 2019? Watch it below if you missed it earlier with focus on the caveat at about minute 5:35 of the clip below. What is that caveat for those who don’t have the time to watch the clip?

- “… just so you are ready to ring the register on a part of your position a month from now when these cycles turn against you … “

.

3. India’s “Trump” Card

No – We don’t mean the incredible & historic event at NRG Stadium in Houston between President Trump & Prime Minister Modi. It was crossing of the Rubicon for Indian-American groups in US Politics, we believe. We will write more about the long term strategic, political & economic ramifications subsequently. Those who care to understand how huge the event was should look at our adjacent article – Elvis & Family- Two Incredible Leaders Together in an Unbelievable Evening.

In this section, we refer to the Wisdom Tree article titled India’s “Trump” Card: Tax Cuts! Their first reason is:

- “This step reflects policy making in India that responds fast to changing domestic and international environments. Back-to-back reforms that were focused on streamlining taxes caused stress for manufacturers and distributors, and weakening credit growth has affected consumer spending. This has been reflected in weakening sales of automobiles and consumer goods. Thus, it was necessary for government to provide a fiscal boost in addition to the monetary boost provided by the Reserve Bank of India (RBI) in August.”

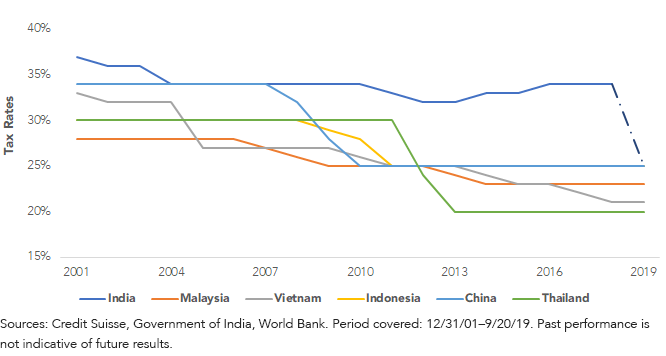

The second reason is trade competitiveness which is instantly explained by the following graphic:

Wisdom Tree points out that Energy & Financials are the two sectors likely to benefit most by the Tax cut. That brings us to our favorite bank stock – HDFC Bank & its comparison to JP Morgan. The chart is of HDB, the NYSE-listed ADR :

The longer term charts show a similar out performance:

Finally, the main reason to invest in Indian stocks is the achievable target of $5 trillion GDP in the next 5-7 years. That is a double from today & getting there in even 7 years is double digit growth with higher growth in corporate profits.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter