Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Was Godot Chinese?

- Scott Wapner@ScottWapnerCNBC – Two days ago it was Phase 1 might not happen by year end. Today it’s “very close” Tomorrow it will something else.

You have to hand it to the two Presidents, Trump & Xi. They just don’t let hope die or even wither. So nobody wants to act on their own suspicions that the deal will never come. Because they don’t want to miss the big up move if it does and especially if it does before December 31.

So, as Mohammed El-Erian said on BTV, people just want this year to end. This was put in a different way by Mithra Warrior of TD Securities to Jonathan Ferro of BTV – “lot of people want a downturn but they don’t want a downturn in December“.

And neither does Fed Chairman Powell. So the dance continues in wait for Godot, sorry Phase 1 of US-China deal. Actually getting the Phase 1 deal could prove more dangerous, like a top.

- Bloomberg Economics@economics – “There’s a deep belief that we will get a mini-deal and it’ll be a stepping stone to something bigger,” says @elerianm on the U.S.-China trade war. “That’s naive…It’s not just about economics anymore, it’s about national security and human rights” hbloom.bg/37o4w37

So the onus is on Chairman Powell to radiate optimism & add liquidity quietly to prevent an year-end eruption in illiquidity. His FOMC have put themselves in a trap by declaring their policy is in “appropriate place”. So he cannot act on December 19 in either direction lest that panics the stock market.

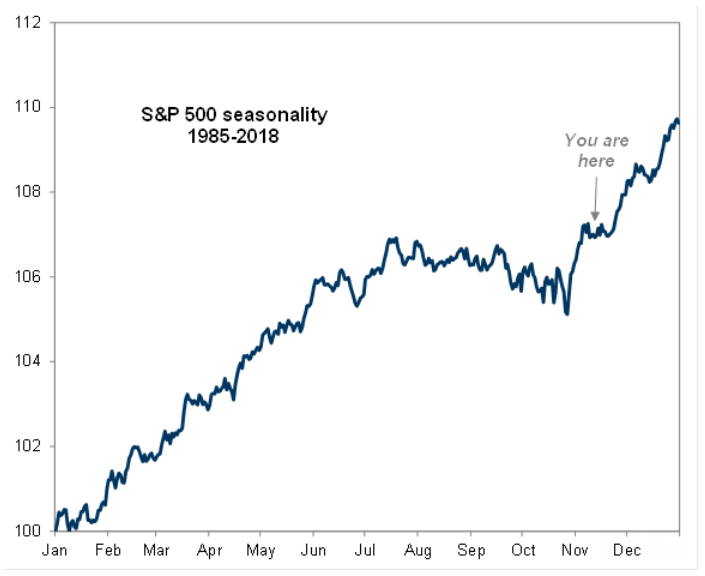

That raises a question. Where is the S&P now vs. seasonality history? From Goldman via The Market Ear:

2. Economy

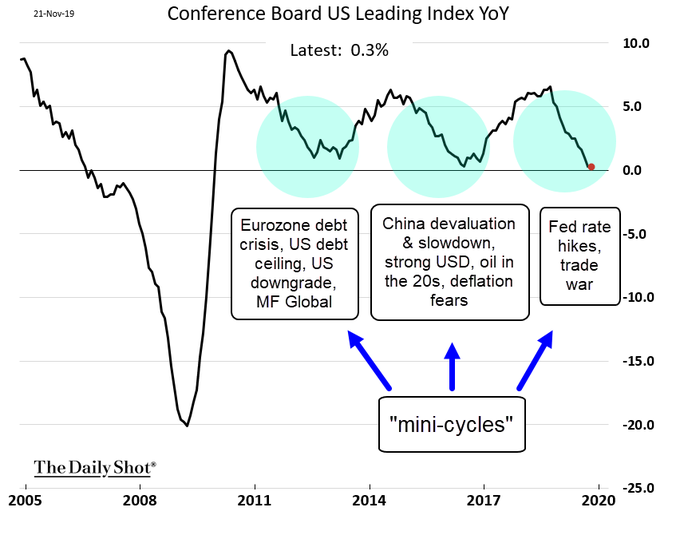

See the chart below & realize how many words it says.

- (((The Daily Shot)))@SoberLook – Chart: US “mini-cycles” –

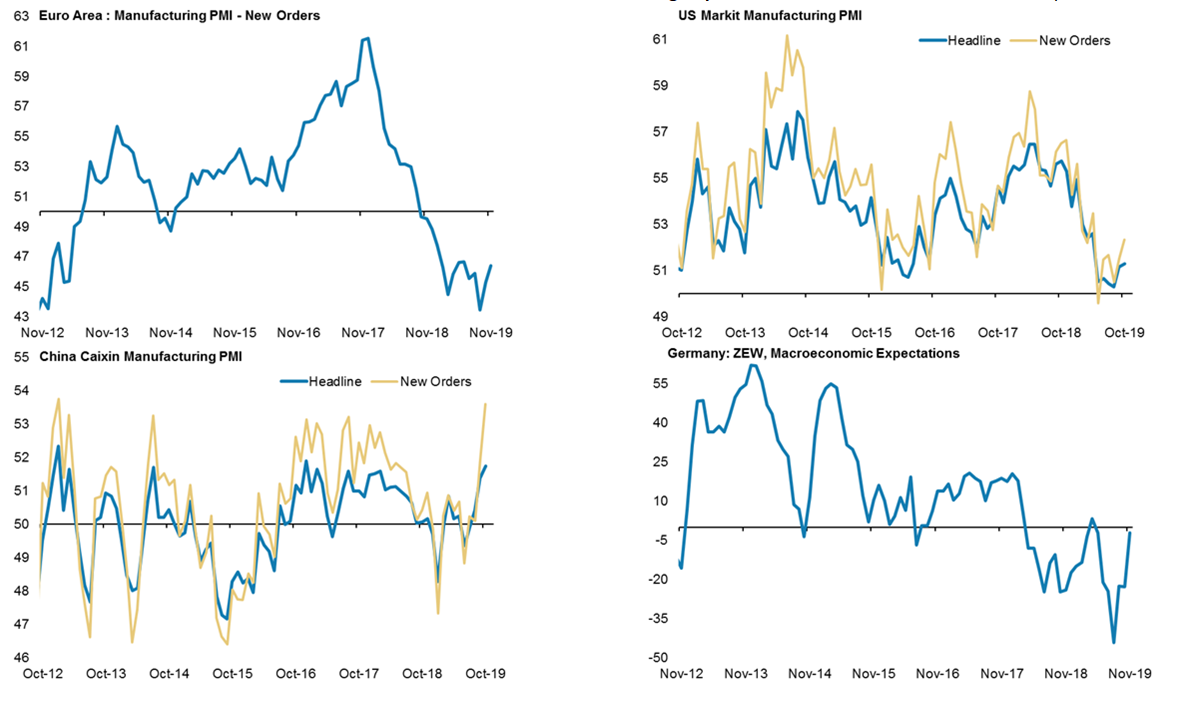

According to The Market Ear, Morgan Stanley Global Economist Chetan Ahya points out that now “we have seen several soft indicators turning up – US markit, China Caixin (indeed Caixin mfg new orders has spiked up sharply), German ZEW“.

On the other hand,

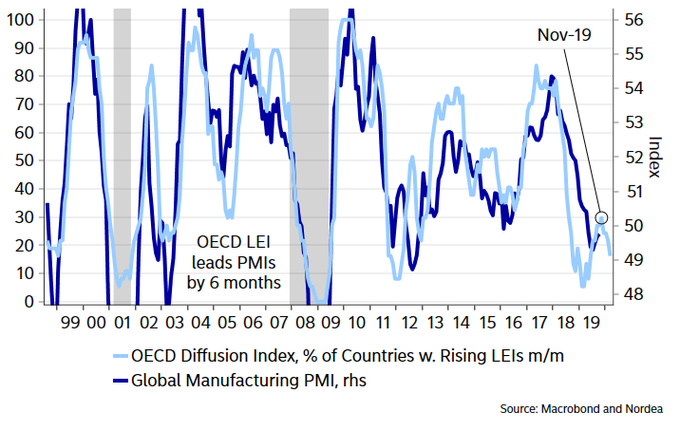

- AndreasStenoLarsen@AndreasSteno – A little rebound in manufacturing but more weakness in services.. Could it be that even the manufacturing rebound is a fluke? The narrative that “PMIs have bottomed” will continue to be questioned over the coming quarter. Our weekly editorial -> ndea.mk/ManuFluke

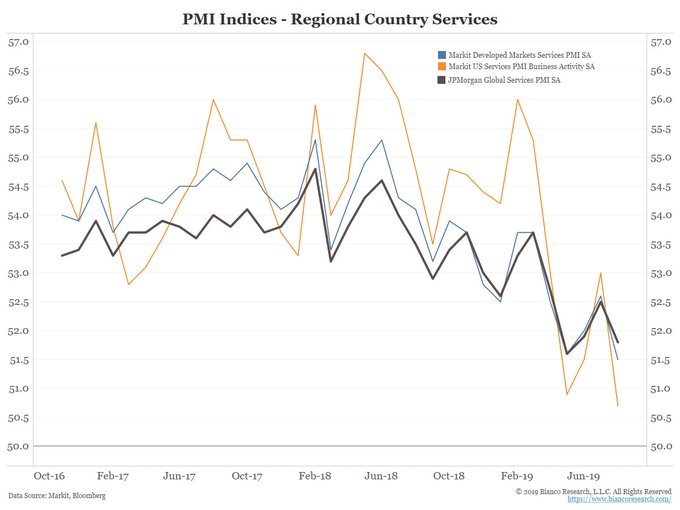

Who else is talking about weakness in Services in US?

- Jim Bianco@biancoresearch – Global services PMI out today. They downticked, dragging down the overall composite index. Not that the US (orange) is now far worse than the developed countries (blue) or Global, which includes China/EM (black).

Can we really end a section on the economy without hearing from him? David Rosenberg said on CNBC Trading Nation on Thursday that “companies’ decisions to cut capital spending is beginning to trickle down to hiring decisions, and that puts consumer spending in a danger zone“.

- “The engine on the labor market is starting to sputter, … The question is when does this morph into deteriorating employment conditions, because that’s when it hits the consumer.”

- “I understand that there’s a lot of optimism that the Fed saved the day. But you have to remember the last cycle. The Fed starts cutting rates in August of ’07. Stock market rips. That’s up 11% to the highs on October of ’07, and all the recessionistas like myself were being laughed at, …. Recession started two months later.”

3. Interest Rates & Credit

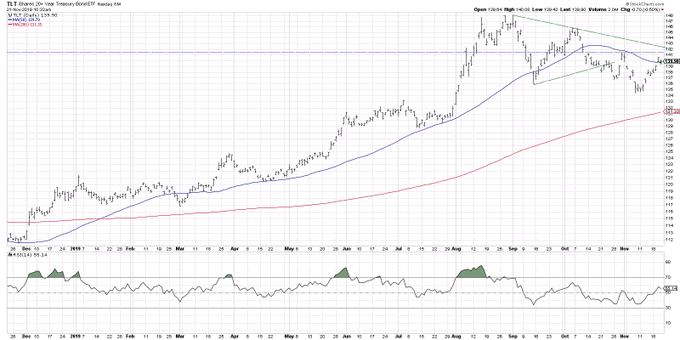

For the second week in a row, Treasuries were the best performing asset class with TLT up 1.5% & EDV, Zero-Coupon Treasury ETF, up 2.3% . Not only did the rates fall but the Treasury curve flattened virtually every day.

The 30-year yield fell this week by 9 bps (after a fall of 11 bps the week before), the 10-year yield fell by 6.5 bps, the 7-year by 4.5 bps, the 5-year by 4.5 bps. The 3-year & 2-year yields actually rose by 1 bps highlighting the flattening. German rates also fell at the long end by 3 bps.

TLT has rallied from just below $135 two weeks ago to just below $140 on Friday. Is this a real move or only a bounce from an oversold condition?

- David Keller, CMT@DKellerCMT – Bonds $TLT would need to a) break to a new swing high above 141.50, and b) break above trendline resistance from the Aug and Oct highs. Until then, this is just a bounce within a downtrend!

This week, we kept hearing about spread-widening in the high yield sector, esp the lower kind.

This is clearly a negative signal but how negative? First leveraged loans & now CCC? We will wait and see whether the pressure builds in this sector.

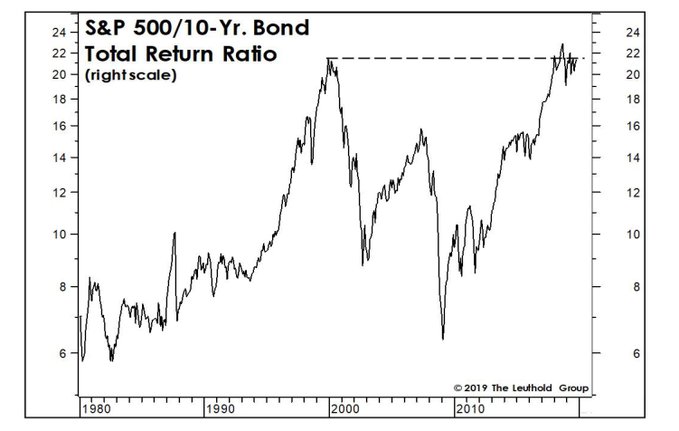

Remember how stupid are investors to lend money to the US Government at x%? Because stocks always go up over 5-years, 10-years? Guess what happened over a 20-year period from 2000 to 2019?

- The Leuthold Group@LeutholdGroup – – Since Y2K thru Oct. 2019, S&P 500 cumulative TR is a couple bps behind the 10-yr Treasury. To achieve this, it required $SPY to escalate to over 25x Normalized EPS and 2.2x Sales.

But, as we recall, almost every time we have seen a chart & a claim like this, stocks have outperformed Treasuries at least over the near term. And that brings us to:

4. Stocks

- SentimenTrader@sentimentrader – There are short term concerns now for stocks. But from a longer term momentum perspective: MSCI World Index has been in a persistent uptrend. 28 days above its 10 dma When this happened in the past, global stocks rallied 91% of the time 6-12 months later

What happened to the VIXplosion we were supposed to see? VIX did rise by 2.4% this week. What about next week?

- Bob Lang@aztecs99 – we OFTEN see volatility tank into a holiday. so, next few days.

What about the channel? A chart from The Market Ear:

Any sign of inflows into stocks?

- The Market Ear – Bernstein: Last 3 weeks has seen best inflows into Equities since Feb 2018, there is ample scope for this trend to continue

Hmmm; we recall what happened after Feb 2018, right? But now to short term concerns.

- Lawrence McMillan of Option Strategist – So, the above paragraphs have laid out some pretty negative data, from extremely overbought put-call ratios to sell signals in mBB and breadth. But the one area that is not turning negative is volatility. $VIX remains at low levels and hasn’t even peeked its head up on recent down days. As long as that is the case, it’s bullish for stocks. In summary, short-term bearish positions are in order, but the intermediate-term remains positive as long as the $SPX and $VIX charts continue to remain in the bullish camp.

Then,

What about earnings & other funnymentals? Listen to the other from the old Merrill Lynch pair who claims that he is “incrementally cautious”. And this is a man who expects volatility to be higher next year, higher than what people think. If it does, will Richard Bernstein describe it in the same sleepy, boring sorry incremental fashion? Really has any one ever seen an agitated Rich Bernstein?

His main point to CNBC’s Mike Santoli:

- “The one thing that people are kind of missing out [on] here is that earnings in the United States are still decelerating, … By our work, we would argue that the first half of 2020 you could actually see a full-blown profits recession.”

By the way, could anyone let us know what “Sant” means in Italian? Because whether you add “eli” or “oli” to it, you get good results at least for viewers.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter