Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.On offense?

Last week we, perhaps in a flight of fancy, compared where we are today to the 1942 battle of Midway which transformed the US strategy to offensive from its defensive posture since Pearl Harbor. The parallels are not exact, but they never are. Our conviction is that we homo sapiens have not changed since the creation of our species. So we can benefit from looking at how others managed their own conflicts in their own era. After all, what did General Patton say after defeating German forces in his first tank battle in Africa – “Rommel, you magnificent bastard, I read your book!“?

We are now seeing the American people standing up in virtually all parts of America & demanding this destructive shut down be reversed. The capital markets version of that was Barry Sternlicht lighting it up on CNBC Squawk Box on Tuesday. His message – “The Government can’t carry a $23 trillion economy” & his warning – “If you don’t open …. , the damage will be irrecoverable…“

Is the stock market, at least the sector that is benefiting from the stay-at-home mandates, sending a similar message?

- Thomas Thornton@TommyThornton – – Goldman Sachs Stay at home basket starting to top

Sternlicht actually said that, at least in his business, rents are being paid in almost all sectors except the We-Work, Regus type shared office space providers. In direct contrast, Kevin O’Leary, an investor in over 50 small companies, said this shutdown is at the expense of landlords (does this Sternlicht & O”Leary difference partly explain why the S&P is beating the Russell 2000 so handily?).

- “…. what we are planning to do across the board is cut our use of office space & retail space by about 30%, hoping to get another 7-11% cash flow right across the board…”

He points out that no business would have even thought about doing so without the shutdown & the destruction created by the CoronaVirus. Hmmm! We heard this & thought of a parallel we all know.

Remember how outsourcing, both in manufacturing & in tech services, was almost unheard of in the 1990s. US Corporations liked the idea in theory but no one wanted to risk it. And there was no reason to change their business model so drastically. Things were fine as they were. Then came the brutal squeeze on profit margins in 2002. Stocks of big companies (GE, MSFT …) went into a nasty bear market from October 2000 into end of 2002.

That virtually forced big US companies to begin outsourcing manufacturing to China & tech services to India, leading to cherished productivity gains & robust profit margins in America and a bull market in China, India & emerging markets.

Is that type of secular change ahead of us in America, especially in the corporate sector? Look what Larry Fink of BlackRock said:

- “I don’t think any company’s going to go back to 100% of the workforce in the office. That means less congestion in cities. It means, more importantly, less need for commercial real estate.”

Kevin O”Leary took this farther & positively:

- “… there is going to be an amazing new America emerge from this with tremendous productivity gains… unfortunately not for real estate..”

As we recall, he specifically mentioned that his companies have been buying from Microsoft. And every family we know has increased its purchases from Amazon. Speaking personally, we may not want to step into a grocery store after receiving home deliveries of food, even frozen delicacies, from Amazon, Farm Fresh et al.

Does that mean the Demarkian warnings about exhaustion are merely tactical & short term in nature?

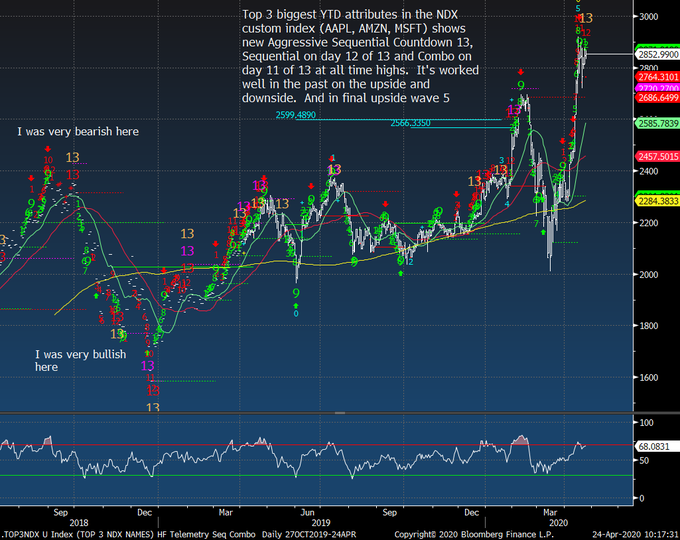

- Thomas Thornton@TommyThornton – Top 3 largest $NDX $QQQ stocks $AAPL, $AMZN, $MSFT nearing upside exhaustion again

The key word in the tweet above could be “again”. Remember the warning last Friday about trend exhaustion after that day’s rally. That led to two brutal days on Monday & Tuesday to be followed by a move up. The Nasdaq 100 only closed down 51 bps on the week. But next week could be different with earnings & outlooks from Apple, Amazon, & Microsoft.

Finally, the most interesting comment of the week came from Kevin O”Leary who coined a new trading index to watch for stock market direction:

- “… Only one trading index to watch – NY Cuomo index; … everybody watches it… sovereign traders in the Middle East watch it … entire world’s indices trade on the optimism of Cuomo in New York or pessimism …”

We can confirm that many we know in Mumbai watch Cuomo’s press conference daily & comment on it to us on WhatsApp.

All the above is fine, but is there a upturn in the economic cycle ahead & perhaps closer than what most think?

2. Flip to upside virtuous cycle? An Upgrade of S&P

Remember what Lakshman Achuthan of ECRI said back on April 6?

- “But if those shutdowns start ebbing by summertime, the economy will then begin reviving, albeit slowly and partially. As a result, the level of economic activity – in terms of output, employment, income and sales – will necessarily rise above the lows seen during the worst of the closures. … It’s when this vicious cycle ends, and switches to a virtuous cycle of self-feeding increases in output, employment, income and sales, that a recession is officially over. We believe that the end of the compulsory closures can jump-start this virtuous cycle in relatively short order”

This week, Achuthan elaborated on this “cycle” view using a 3-D model of a recession:

As he says, “this recession is extraordinarily deep. Already, 26.5 million people have filed for jobless claims, compared with a total of 8.7 million jobs lost during the Great Recession. And it’s not over“. In terms of diffusion, this recession is certainly severe, affecting a wide range of industries.

Now look at the size of duration between the two recessions in the above picture. Achuthan says that “on the third “D,” duration, this recession could be among the shortest on record“. Why?

- “With economic activity plunging so deeply, even a slow, partial opening up of the economy would lift activity off those extreme lows. If that happens, …. the recessionary vicious cycle will flip to a virtuous cycle of a self-feeding recovery. In that case, the recession could end by summertime. If so, this would be among the shortest recessions on record, closer to half a year, compared with a year and a half for the Great Recession“.

If Achuthan proves right, then would you not get more bullish on the S&P 500? Well, Ed Clissold of Ned Davis Research did this past week:

- Stephanie Landsman@StephLandsman – Market gets an upgrade from top strategist, says a lot of the worst news is over cnbc.com/2020/04/23/cor(via@TradingNation)

Why his upgrade?

- “The market tends to lead the economy … An average of four months before the end of recessions is when the S&P 500 bottoms. …. There has been clear improvement in the tape action, It tells you a lot of worst news is behind you”

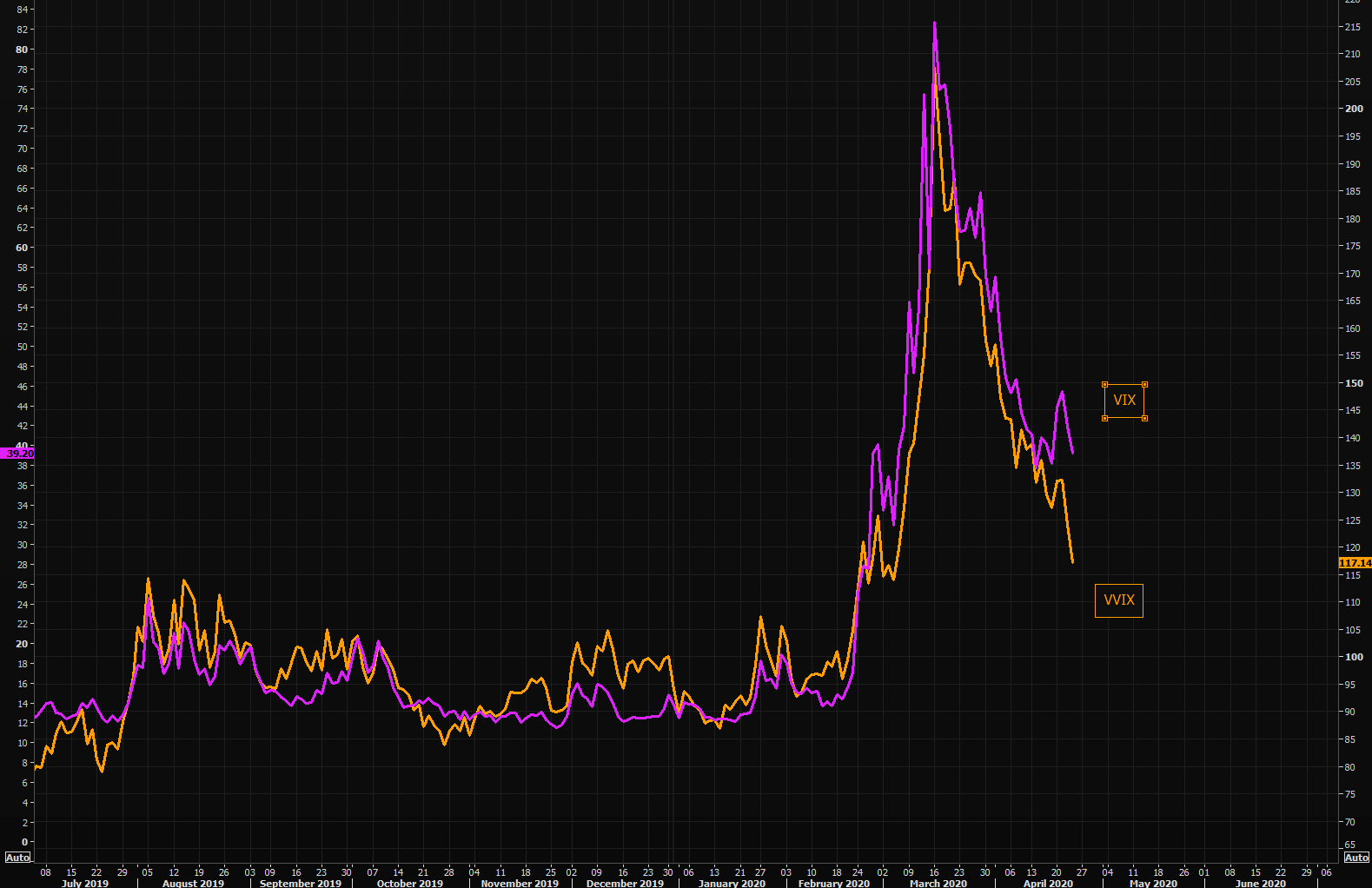

Isn’t that consistent with Achuthan’s target of flipping to a virtuous cycle in late summer? And we have seen a steady fall in the popular measure of fear in the S&P. Look at the month of April so far. On April 3, VIX closed at 46.80, a fall of 28.6% from the week before; the next week it fell by 11% to 41.67; it fell 8.4% to 38.15 on Friday, April 17; last week it fell by 5.8% to close at 35.93 on Friday.

- Bob Lang@aztecs99 – vix term structure starting to flatten out in favor of the bulls. prob need some more positive virus news, but the fed might throw yet another bone next week.@OptionVol @dynamicvol

What is the leading indicator of VIX saying, the rate of change kind? VVIX, the rate of change of VIX, is falling faster than the VIX. Look at the chart courtesy of The Market Ear:

Is this fall in VIX saying there are too few bears around? Not according to AAII via Market Ear:

Then you have month-end coming up. After that brutal March, wouldn’t big long money like to show a big positive April especially after a down for Dow (minus 1.9%) & the S&P (minus 1.3%)?

And, according to BAML Research, “Cash mountain: $4.7tn currently in Money Market Funds“.

3. Rates & Credit

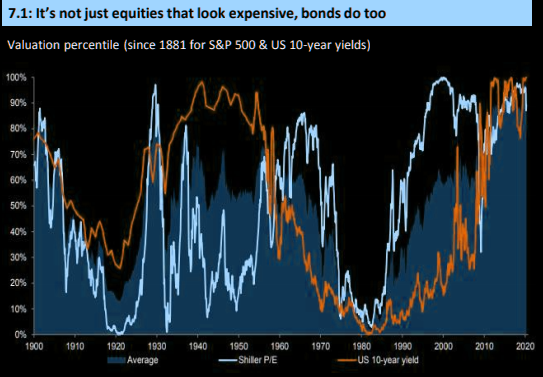

In the past, when you thought stocks were expensive, you looked at Bonds. But,

- Market Ear – Not only stocks are expensive, bonds are too; On the other hand, max frustration is when expensive goes even more expensive…

And while Dow & S&P 500 went down last week, TLT, the Treasury ETF, rallied 1.4%. Rates fell along the entire Treasury curve flattening it in the process;

- 30-year yield fell 10.2 bps to 1.166%; 10-yr yld fell 5.7 bps to 59.1 bps (yes, below 60 bps); 7- yr fell 2.1 bps to 50.1 bps & 5-yr yield fell by 0.3 bps to 36.1 bps.

Not just the levels, but the relentless appetite:

- J.C. Parets@allstarcharts – stocks go down, bonds go up. Stocks go up, bonds don’t go down. you notice?

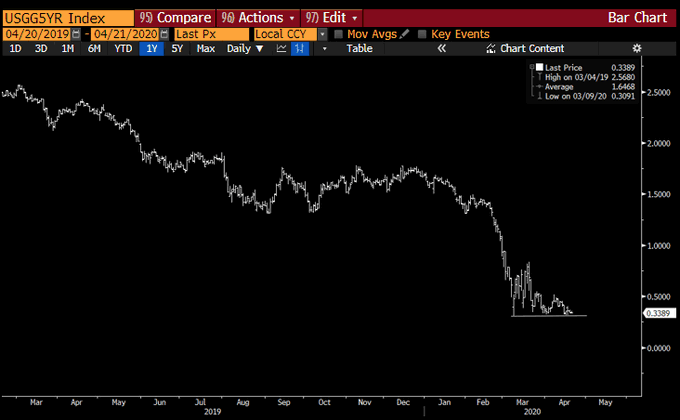

That’s one way to look at interest rates. What’s another? As Porn?

- Raoul Pal@RaoulGMI – – Last tweet before bed… 5 yr yields = pure chart porn. Probably the best looking chart in the world. Yields are going to zero. Good night all.

But some luminaries think this is “madness”, to use a favorite descriptor at CNBC Fast Money:

- Lloyd Blankfein@lloydblankfein – In finance, most surprising to me is that despite the trillions the US is adding to our budget deficit and national debt, investors (many foreign) will lend the US a virtually limitless supply of dlrs for .6 pct for 10 years.

Perhaps, he might want to speak with his old firm’s credit group. Because, per FT,

- “Goldman Sachs — which helped underwrite a €3.5bn syndicated loan for Italian-American carmaker Fiat Chrysler this month — did not take part in a similar €12bn facility for German rival and long-standing client Daimler, leaving other lenders to make up the difference.”

Of course, Goldman is not the only US bank “pulling back from lending to European companies” according to the FT article. Why? One reason is,

- ” … profit margins on loans were much higher in the US than in Europe, demand for credit was rocketing everywhere and that banks’ balance sheets were an increasingly scarce resource. … “

A scarier reason, according to the FT article:

- “Some US bankers said European lenders were acting “recklessly”, loading up their weak balance sheets with more risky loans that could turn into problems in years to come. “I don’t understand why the Europeans want to do these things,” said a senior investment banker.”

Perhaps Mr. Blankfein should also talk to old friends at BAML:

- Lisa Abramowicz@lisaabramowicz1 – “The base case remains that the credit cycle ahead of us is likely to be at least as damaging as anything we have seen in recent recessions,” including a 30% drop in EBITDAs & a 21% cumulative default rate: BofA Global Research

Is this why high yield ETFs, HYG & JNK, are down 4.8% over the last two weeks while the Treasury ETF, TLT, is up 3%?

Also why are foreign investors willing to “lend the US a virtually limitless supply of dlrs” as Mr. Blankfein wonders?

- Peter Brandt@PeterLBrandt – What we talked about last week, @RaoulGMI on @RealVision $EURUSD The world is short USD

Not only could the world keep exporting us their deflation, but what we see within the US is also scary:

- Richard Bernstein@RBAdvisors – With corporate, household, and municipal cash flows under historical pressure maybe yield/income #investors are finally realizing higher yields come only with added risk. There is NEVER a free lunch.

Adding to the real problems, look at the sheer stupidity of Senator McConnell in suggesting States should be free to file for bankruptcy. Not only did he give NY Governor Cuomo a chance to be both Dirty Harry & Ronald Reagan, but how many Muni investors did he scare into selling their Muni funds & piling into Treasury funds?

How does this mess square with Lakshman Achuthan’s case of this recession ending & flipping to a new virtuous cycle? He warns:

- “And while that sounds downright optimistic, the end of recession is only the start of a recovery, probably with double-digit unemployment rates, which are unlikely to plunge in short order. So, things won’t get back to “normal” anytime soon.”

Finally, Mr. Blankfein might want to speak to the “Buffet” of Treasury investing:

- Lisa Abramowicz@lisaabramowicz1 – – Lacy Hunt has spent years explaining why long-dated Treasuries would continue to outperform, & he’s been right year after year. 2020 is no exception, with his Wasatch-Hoisington U.S. Treasury Fund gaining 29% so far. @mccormickliz

Read what Lacy Hunt is arguing now:

- The historic, pandemic-fueled surge in the U.S. government’s debt load is paving the way for years of middling economic growth, deflation and yields of all maturities near zero.

- At $17 trillion and counting, the U.S. debt burden is on a path to eclipse the size of the economy by an unprecedented degree, and already highly-leveraged companies are taking on more loans to stay afloat. That backdrop creates a world leaning too heavily on “unproductive debt” and less able to invest in technology and labor. Hunt expects it will take a half-decade or more to reduce the slack in the economy, an environment that makes very long-term Treasuries the best bet in fixed income.

- “The U.S. had a debt overhang problem even before the coronavirus,” Hunt said. “It won’t be productive debt, and will not generate future growth. So inflationary expectations will turn into deflation expectations, and the entire yield curve is going to be pressed down on to the zero bound.”

Imagine what this might do to valuations of companies with high growth rates, fortress like balance sheets & huge customer bases that grow more dependent on buying more & more with greater convenience from these companies. Know also that fall in Treasury yields increases the PE multiples of such technology companies.

You know this forecast of Hoisington was not the scariest thing we heard this week, very scary as it is. No we were appalled at the Unusual Options Activity highlighted by CNBC’s Jon Najarian – Buy TLT May 180 calls. That is a 6% rally in TLT by May expiration. Holy Whatever!

4. Gold & Oil

Speaking of Jon Najarian, he also said that he expects Gold to get to $2,000 & remains bullish on GDX calls. Smart given that GDX & GDXJ, Gold miner ETFs, were up 13% & 14% resp. What a pair of twins that makes, David Rosenberg & Jon Najarian!

- David Rosenberg@EconguyRosie – Remember the Great Depression. Deflation came first with the massive shock. Then came the policy-induced inflation with a lag. The vagaries of eroding productivity once demand stabilizes. Buy gold!

That brings us to the craziest thing we have seen. The fall in May Oil to negative $37 on settlement. The negative rates in Europe we hated but at least could figure those out. But the May oil crash was just nuts. The only thing crazier could be perpetual Government bonds that don’t ever mature but fluctuate in yield & price and settle monthly on a cheapest to deliver basis. So the settlement yield would mainly be based on demand & supply of physical holdings of required bonds. Wouldn’t touch such a bond, not on our life.

This entire oil mess is beyond us. So the best way to think about it is to listen to Mark Fisher, the trader extraordinaire. Simply his view, as expressed on that day, was buy June oil below $15 & sell above $20. But be very careful before June oil expires in mid-May because the same could be repeated around that time.

He also alluded to $USO, the utterly stupid vehicle as it was constructed. Now Fisher said it has become a closed end fund. What does that mean? Does that now trade at discount or premium to its NAV? Does $USO have a NAV? And how useless that NAV would be when oil futures trade the way they may around expiry?

The most insane, positively insane, part of this oil mess is the rally in XLE, integrated Oil companies ETF, a rally that touched its near term resistance at $35 this week as May oil fell below $37. Next week Exxon & Chevron are on deck with their earnings. As Craig Johnson of Piper said, if XLE breaks through $35, it could go to $40.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter