Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.So simple?

Wasn’t Friday a “wonderful day for the QQQ + TLT portfolio” (to use the phrase of Bloomberg’s Brian Chappatta on Friday, June 4, 2021)? QQQ was up 55 bps and TLT was up 1.06% on Friday. The week was better for the QQQ up 2.3% than for the TLT up 41 bps (EDV up 1.2%). Both QQQ & TLT beat the S&P 500 on Friday as well as for the week. The S&P was down 14 bps on Friday and down 32 bps on the week.

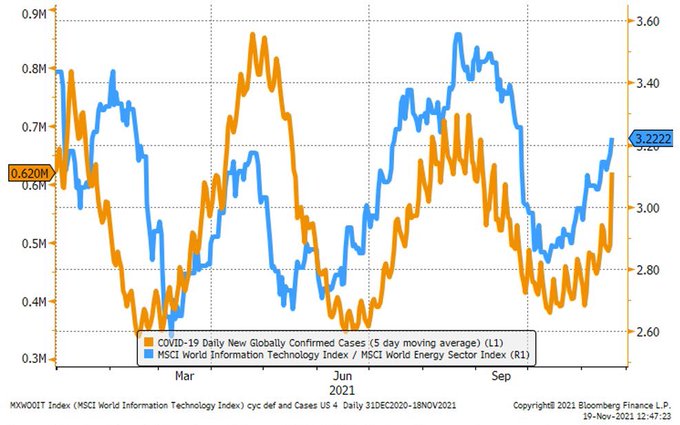

Friday’s action had a new catalyst for the Tech outperformance per a retweet by Jesse Felder:

- Michael A. Arouet@MichaelAArouet – –Tech/Energy ratio vs. Covid cases What a chart. Ht@JeffreyKleintop

Actually the out-performance of Tech was highlighted a day before by

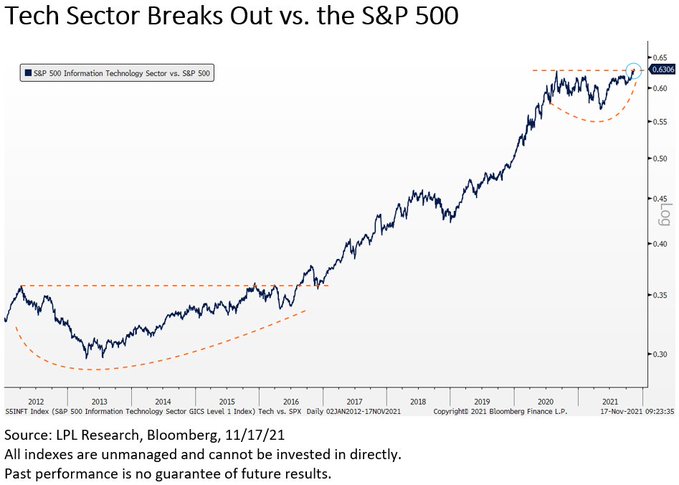

- Ryan Detrick, CMT@RyanDetrick – Nov 18 – Tech is breaking out relative to the S&P 500 after 14 months.

The linked article from LPL Research states,

- “The theme of 2021 has been rotation, rotation, rotation,” said LPL Financial Technical Strategist Scott Brown. “But technology is the only sector to recently hit a 52-week relative high and we believe that sets up a favorable outlook heading into 2022.”

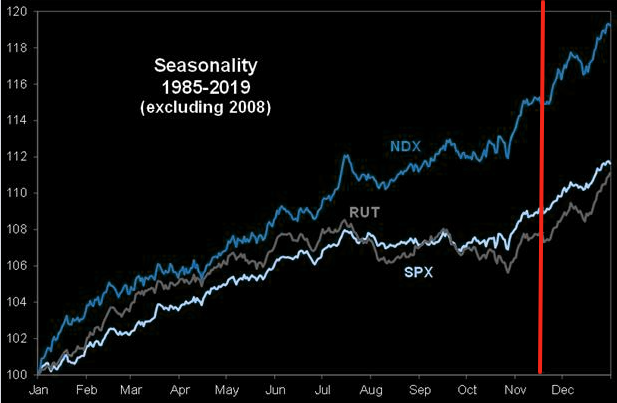

That seems to fit in with the Seasonality chart from The Market Ear:

But how will this seasonality handle a potential Covid Wave 4 that may be underway right now? With a short term peak in the market & a potential 38%-50% retrace of the rally from October, said Mark Newton, technician at Tom Lee’s firm. Such a pullback will however be a viable buying opportunity to end the year at 4800 or above said Tom Lee on Wednesday, November 17:

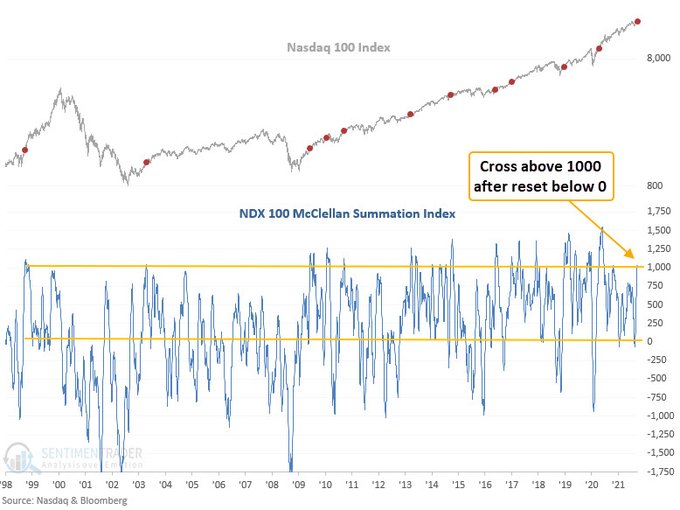

Guess technicians have become like economists these days. The above short term peak signal was on one-hand technical call and the new buy signal observed this week was on the other hand call from another technician, as retweeted by @Sentimentrader:

So whom should you trust? An interesting answer from a 3rd technician:

2. Da Fed & Treasury Rates

The “Da” comes from the old Chicagoland term “Da Mayor”. Just like many in that Chicago felt that Da Mayor Daley was a bully, we get the sense that many in Fin TV believe that the Fed & the Treasury market are bullying them. Despite their fervent wishes for a Treasury market selloff, the darned thing just doesn’t listen.

And it continues to tease them by rates moving higher in the first part of the week only to go down again in the latter half of the week. And the Treasury curve bull-steepened again this week with the 30-year, 20-year falling 3.7 bps while the 5-year fell by 1.3 bps & the 3-yr rose by 0.6 bps.

Then you have Priya Misra of TD Securities saying that the “markets are underestimating fiscal drag in 2022″ & that she doesn’t expect the Fed to raise rates until late 2023. Yes, you read it right – late in 2023 as she said in her conversation with BTV’s Tom Keene on Tuesday, November 16:

- “The market is pricing in the first rate hike literally right after when tapering ends, … Our view is that there are huge Covid impacts on inflation that are going to start to decelerate. Growth is going to slow, inflation will peak. … There’s a lot of hidden slack” in the labor market‘ … We also think the service economy will pick up and create demand for those jobs.”

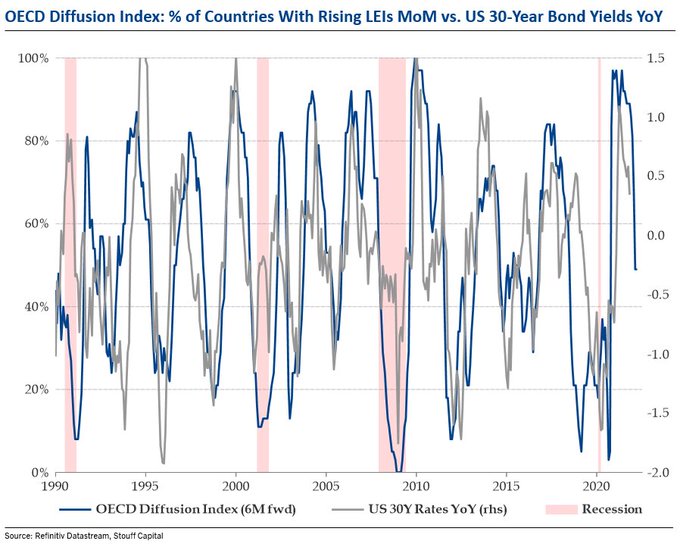

But that is about the front-end or the belly of the Treasury curve. What about TLT or the 20-year plus section of the Treasury Curve?

3. S&P & Small Caps

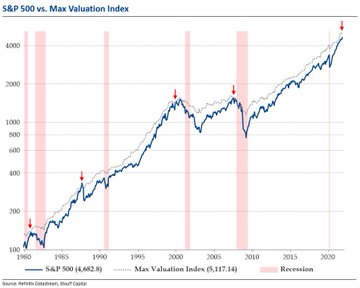

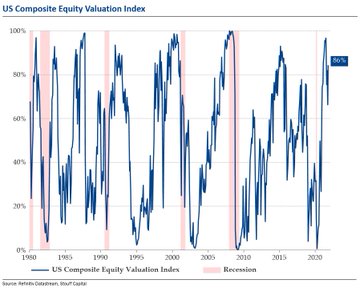

What do “a peak in global economic momentum” followed by “a peak in bond yields” mean for stocks, especially when “valuations in the US are undeniably stretched on almost all measures“?

- Julien Bittel, CFA@BittelJulien – – Valuations in the US are undeniably stretched on almost all measures. My composite US equity valuation index is in the 86th %tile of its historical distribution since 1980. On the other hand, equities could rise another 9% before we hit max valuation extremes on my numbers.

What do more traditional indicators say?

- Lawrence McMillan of Option Strategist – Equity-only put-call ratios have rolled over to sell signals, as the internal deterioration in the market this week involved a sharp increase in put buying. Breadth has been the really negative indicator this week. The last four days have had negative breadth, and that the last two days have been abysmal. Needless to say, the breadth oscillators are on sell signals, and they are plunging. In contrast to some of the negative indicators above, implied volatility indicators are mostly positive for stocks. The trend of $VIX remains lower, for example.In summary, we are holding a “core” bullish position because of the strong $SPX chart. However, we will trade confirmed signals around that — both buy and sell signals.

If Treasury rates behave & Covid dampens the economy a bit, then MANAA should work well as they did this week with Microsoft up 1.9%, Apple up 7.1%, Amazon up 4.2% & Alphabet up 17 bps all making up for Netflix down 82 bps. If MANAA stays in a “core” bullish position, then it is easy to see how the S&P can remain in a “core” bullish position too.

What about the chart from The Market Ear that used to show a correlation between TLT & the QQQ/IWM ratio. If that correlation is still valid, then what might it mean to the question raised below?

- J.C. Parets@allstarcharts – – will this be a successful retest or a massive failed breakout in small-caps? $IWM

Carter Worth of CNBC Fast Money did not definitively call it a “failed breakout” but termed Small Caps a “trap”:

4. Commodities

The Dollar was up with UUP & DXY both up 99 bps on the week. Naturally, Gold was down 1%, Gold Miners down 3.3%, Silver down 2.9% & Copper down 1.3% with FCX down 7.3% on the week.

Oil was down harder with Crude down 5.8% and Brent down 4.3%. Oil Services were shot with OIH down 10.5% & XLE down 5.1% on the week.

Emerging markets were down hard as well. Indian ETFs were down 3%, Brazil was down 5%. Chinese ETFS had the smallest hit. So EEM was only down 1%.

Does that mean the peak of inflation is behind us? Or is this the pause that refreshes especially for the most politically dangerous inflation of them all, one that would make Thanksgiving a little less happy? As Geopolitical Futures wrote this week:

- “Next week is Thanksgiving, a U.S. holiday that celebrates, and is celebrated with, food. This year, however, Americans are reckoning with rising food prices. The news abounds with stories of long lines at food banks, poultry shortages and more-expensive-than-anticipated dairy products. High energy costs and transportation disruptions are fairly well documented too. Less attention has been given to the rising price of fertilizers, a critical input to food supply that threatens to keep food prices high well through 2022“.

For a global view of food prices & their impact on politics, take a look at our adjacent article Is the Real Global Danger Ahead or Is the Peak Behind Us?

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter