Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Williams, Wilson, Newton et al

Sound almost like a law firm, doesn’t it? But first let us acknowledge the “hardly any” bulls that we wrote about last week, especially Jessica Inskip whose views were featured by Cramer last week. And Larry Williams who said buy on 15th trading day of November to Cramer on last Monday. What a call was that? Because Tuesday November 22 was phenomenal.

Before we get to that, let us revel in what was a good week and thank the Equity Gods & Goddesses:

- Dow up 1.8%; S&P up 1.5%; NDX up 68 bps; RUT up 1%; DJT up 1.3%; XLU up 3.2%, XLP up 2.4%; CLF up 9.3%; FCX up 2.5%; MOS up 5.3%; VIX down 11% to 20.50;

Actually we have to say more than mere thanks to Fixed Income Goddesses & Gods (let no one accuse us of gender prioritization):

- TLT up 3.2%; EDV up 4.7%; ZROZ up 4.1%; 30-yr yld down 12.3 bps; 20-yr yld down 12.2 bps; 10-yr yld down 7 bps; 7-yr yld down 7 bps; 5-yr yld down 6 bps; EMB up 2.2%; HYG up 1.1%; JNK up 1.1%;

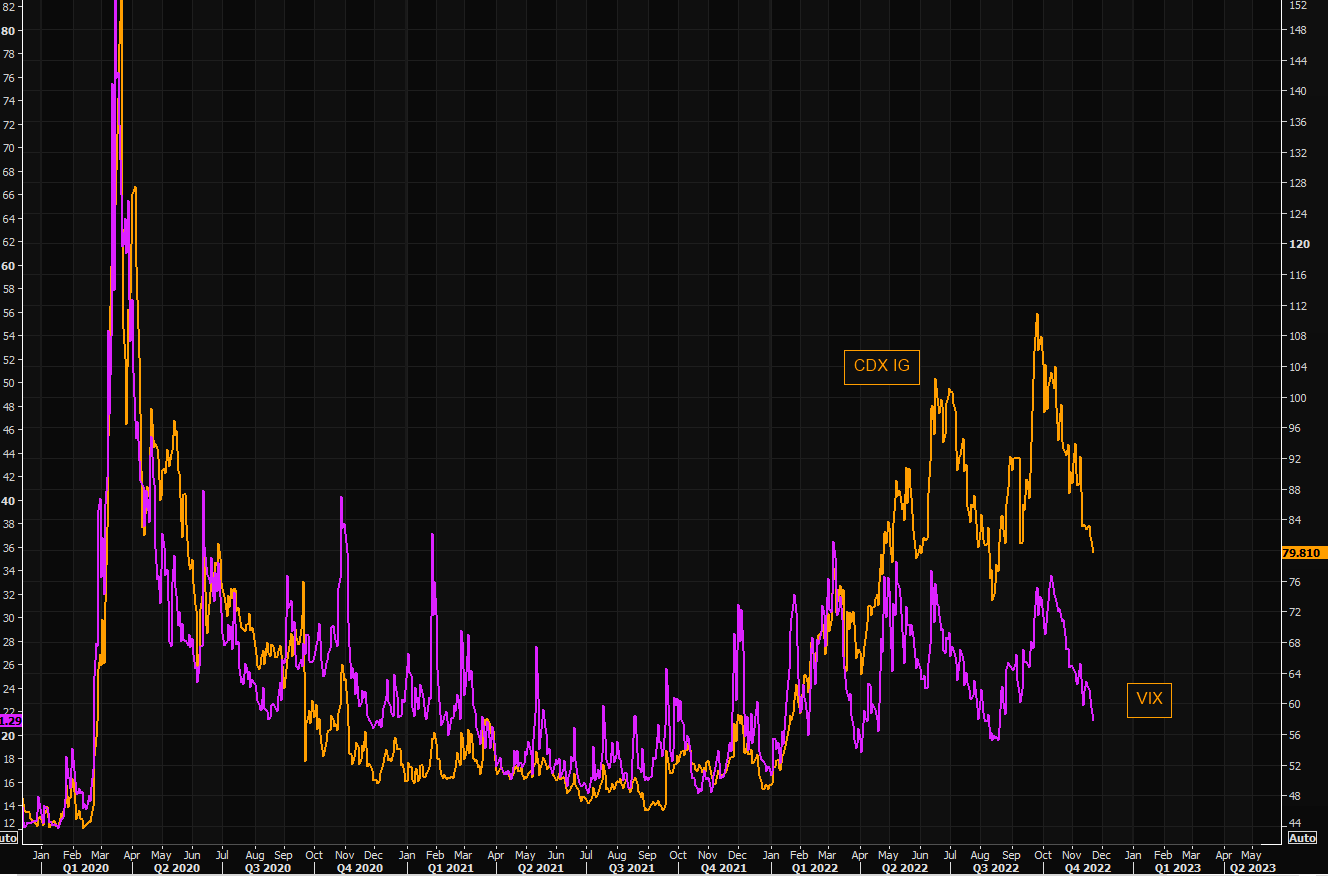

Every one saw the VIX going down this week but how many saw the puke in credit protection?

- Via The Market Ear – Wed – US credit protection puke – CDX IG is printing the lowest levels in a while. The latest move from panic highs is the largest cumulative move lower since credit protection started rising in early 2022.

Before you feel happy about this small stuff, read & think what (as we understand it) Mike Wilson says might happen – “10-year could fall precipitously to 3.25%“. From 3.696% close on Friday to 3.25%? That’s another 45 bps in the 10-year or 6.5 times the fall in 10-yr yield this past week.

Think about it. If the 10-yr yield drops by 7 bps & S&P rallies 1.5%, what might the S&P rally look like? Six & half times the 1.5% rally this week or another 10% from here????

Forget these big numbers. Let us look about 2.3% higher from Friday’s close of 4026. That gets us to 4,120. Why is that important or even possibly relevant? Because of what Mark Newton said on CNBC Overtime Tuesday, November 22:

- “4,120 is where a giant trend line from January intersects right up above 4,100; … 200-day moving average has less relevance to my work than these longer term downtrends & that’s going to be important … “

Newton explained why this rally has been important:

- “today was the date that leads us higher , 4100-4120 really by first part of December … today was different – it was a lot more broad-based & markets did close at a new multi-day high … look breadth is in very good shape – over 53% of all stocks are above their 200-day mv; that’s the highest level we have seen since January “.

Doesn’t this fit with the above puke in credit protection “since early 2022“? Does it mean more when credit, interest rates & stocks all send the same signal?

But, in the midst of this, we can’t forget that Fed Chairman Powell is going to speak next week & the Non-Farm payroll report is out next Friday. But can Powell really take out all the perceived dovishness that was read in the FMOC minutes released on Wednesday, November 23. It was that day when the 30-year yield fell by 10.4 bps, about 85% of the week’s decline of 12.3 bps. Aren’t the FOMC minutes now regarded as an update of FOMC views since the last meeting?

So perhaps it might all come down to next Friday’s NFP report and then to the CPI the following week. May be that is why Mike Wilson keeps saying that his call for a stock rally is really based on a rally in Treasuries!

Finally a sign that good, morally good, things are happening all around us. Michigan literally wiped out the formidable & egoistical Ohio State in Columbus in the fourth quarter on Saturday. Is that an omen for the next 3-4 weeks, the fourth quarter for investors?

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroviewPoints on Twitter