Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. WOW

How else can you describe what they did to Amazon, Microsoft, Google, Domino’s Pizza on Thursday?

- StockTwits @StockTwits – This chart shows what just happened to Amazon. SPIKING on a huge revenue beat -> http://stks.co/p1uOX $AMZN

AMZN was up $55 or 14% on the revenues beat and on the excitement of its new venture. Microsoft was up 10.4% on its quarter and on Thursday morning Domino’s Pizza shot up 10% and rose another 4% on Friday. GOOG was the last in this race up merely 3%. And all this was a day after Nasdaq hits an all-time high. The week before Netflix delivered its own fireworks and rose 23% in the past two weeks. Frankly, we can forgive ourselves for missing the AMZN jump but how could we have missed the Domino’s spike despite knowing so much about their product? Peter Lynch would never forgive us for not being overweight DPZ.

But the market reaction was stunning and perhaps reflects not merely the numbers/outlook but also the built-in worries about the numbers. Now comes the interesting part – do these stocks and the market indices carry their momentum with a confirmed breakout or do they fail in breaking out? Janet Yellen may have something to say about it on Wednesday.

2. Debbie Downers

A number of gurus pointed to resistance, breadth & sentiment levels on Friday.

- Dana Lyons @JLyonsFundMgmt – Amazing NDX-breadth dichotomy today.

- Northy @NorthmanTrader – Fwiw: Upside risk remains into 2125-2180 $SPX with a $VIX to sub 11. Knock yourself out

- Northy @NorthmanTrader – $SPX vs $VIX: Buying versus Selling Opportunities

Then after the close,

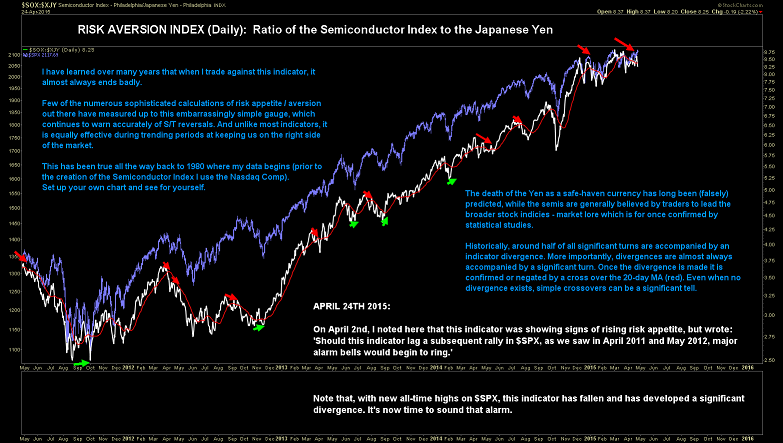

- James Goode@OntheMoneyUK – $SPX Timing Model: Sentiment warning lights start to flash

Total Put/Call: http://schrts.co/7WBCSN Risk Aversion: http://schrts.co/IJ05pI

The second chart has an interesting risk indicator:

And finally the verdict from Lawrence McMillan:

- Lawrence G. McMillan @optstrategist – The Stock Market 4/24/15 http://www.optionstrategist.

com/blog/2015/04/weekly-stock- market-commentary-42415 …

But do the above mean much when the Central Banks are the best friends of Stock markets? We might get a partial answer on Wednesday.

3. Interest Rates

With stocks threatening to break out, how can interest rates fall? The yield curve bear-steepened this week with the 30-year yield rising by 9 bps while the 2-5 year curve barely budged. Steepening of the curve seems to be the major trend of 2015 with the 30-5 year spread closing at 129 bps on Friday, the highest for 2015. But as Rick Santelli pointed out on Friday, the action merely brought the 10-year yield near the top of its 1.86% – 1.99% channel that has prevailed for 27 straight sessions.

Almost all of the week’s spike in 30-year yield happened on Wednesday. How big was that spike?

- Thursday – John Kicklighter @JohnKicklighter – Yesterday’s jump in yields was the biggest daily jump (behind Feb 6) since June 2013: htttp://cdn.dailyfx.com/forex/fundamental/article/special_report/2015/04/23/FOMC-Minutes-See-Growth-End-of-QE-and-Financial-Risk.html?CMP=SFS-70160000000NbTmAAK …

We all remember how yields acted after June 2013. Will the Fed statement lead to a repeat performance & break the 1.86% – 1.99% range or will the leveraged shorts panic creating a fall in yields?

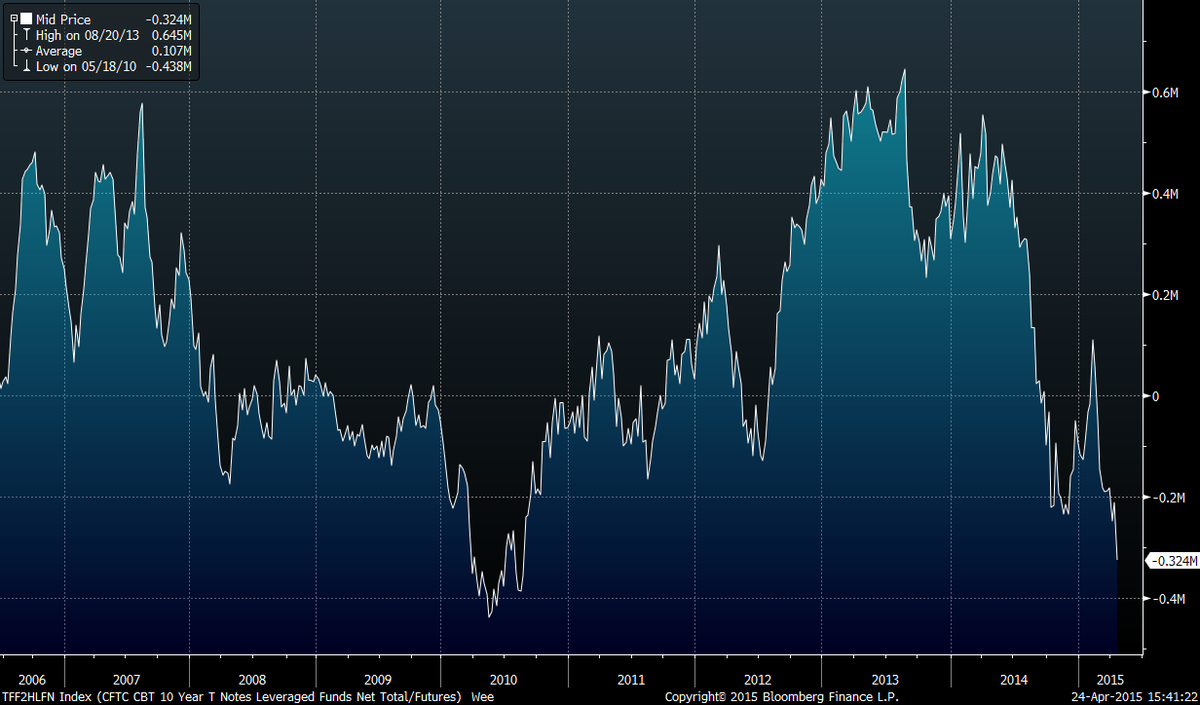

- Matthew B @boes_ – Leveraged funds are now sitting on the biggest net short position in 10y UST futures since 2010, close to record

.

The fundamentals have not mattered to the Treasury market for a couple of weeks, fundamentals like:

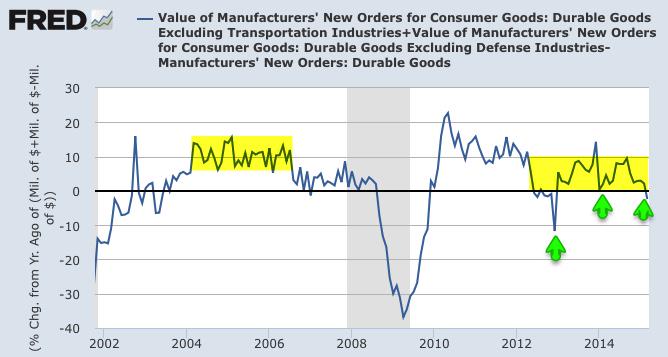

- Friday – Urban Carmel @ukarlewitz – Core durable goods fell 2.4% yoy, the first neg print since 2012. Winter (arrows) weak but this was a real stinker

The lowest yield target we had seen for the 10-year was 1% from Gary Shilling. After the close on Friday, we saw a lower target from a model, a model used by Scott Minerd of Guggenheim Partners. In his chart of the week titled 10-year Rates Could Bottom Near 0.80% in March 2016, he discussed his model & the chart below:

- “What’s even more interesting is that the average actual bottom in rates has been 73 basis points lower than the model predicts, which would put rates at just 0.09 percent“

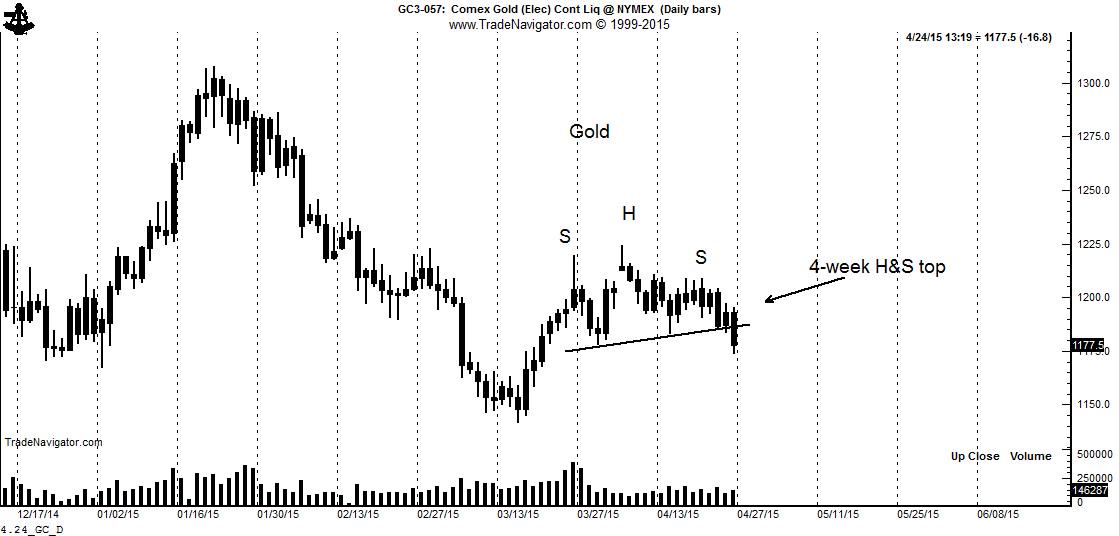

4. Gold

Oil has mounted a six-week rally. The miners have had a big move. But Gold just can’t do a thing except act ugly. And even a fall in the Dollar on Friday could not prevent Gold from falling hard. Add the following ominous warning to that action:

- Friday – Peter Brandt @PeterLBrandt – H&S top pattern completed today in #GOLD $GC_F $GLD

What will Chair Yellen do to the Fed next Wednesday?

Featured Videoclip:

1. Stanley Druckenmiller with BTV’s Stephanie Ruhle on April 16, 2015

Jeff Gundlach has said that investors should listen to every word Mr. Druckenmiller utters. Who are we to disagree with Mr. Gundlach and why should we when we concur? This interview covers three different topics in three different clips:

- Zero Interest Rates Unnecessary Now – http://bloom.bg/1PSnIYU

- Won’t be Contagion with “Grexit” – http://bloom.bg/1yrEA37

- China Stock Gains Signal Economic Recovery – http://bloom.bg/1yrEw3x

Almost everyone is telling us that parabolic up moves like the one in Chinese market are a bubble & will lead to crash. Mr. Druckenmiller provides a different perspective in the 3rd clip. Below is a description of that conversation courtesy of Bloomberg Television PR:

DRUCKENMILLER:

- “The Chinese stock market is up, I don’t know, 140 percent in six months after being in a downtrend for five to seven years, and it’s doing so on record volume with record breadth. If it was any other stock market or certainly any developed market, I would tell you, being a market observer, there’s a 98 percent chance China will be in a cyclical boom 6 to 12 months from now. Because it’s China, and we don’t know the nature of what we’re dealing with here relative to normal mature developed markets, I would downgrade that assessment from 95 percent, but I would still hold it over.”

RUHLE: Because you don’t trust the data, Jim Chenos style?

DRUCKENMILLER:

- “No. It’s not the data. I’m watching the markets, and whenever I’ve seen a stock market explode on record volume and record breadth and move to that degree, like day follows night, 6 to 12 months down the road, you’re out of recession, and you’re into a full-blown recovery. The reason that happens, I think there’s enough of that, that it’s certainly greater than 50 percent China will be in 6 to 12 months, and just think of how differently the world is thinking about that. The Fed had it in their minutes last month that one of the reasons to delay, or one of the things of concern was the Chinese economy. Christine Lagarde was on the cover of the Financial Times last Friday. Her biggest worry, the Chinese economy, so as someone who’s trying to think of what security prices might look at 6 to 12 months down the road, I’m very intrigued with, A, the possibility of a Chinese economic recovery, and how differently we all might be thinking if it’s actually unfolding later in the year.”

RUHLE: No concerns that stocks listed in Shanghai and Shenzhen are overvalued?

DRUCKENMILLER:

- “Well, I’m not — first of all, no. Over valuation doesn’t concern me at all. I’m not even opining on the stock market. I’m opining on the transmission mechanism, the stock market to the economy, but I would point out that the H shares in Hong Kong representing China are 10.1 times earnings. I mean, I bought the NASDAQ at the high end, I mean, in 2000 when it was a 150 times earnings, so I’m not talking about valuation or even the Chinese stock market here. I’m talking about when you get this kind of thrust, when economic activity is weak, in a normal market, you get a big economic response 6 to 12 months down the road. Because it’s China, I think we’re talking about 70 percent, but the market is probably at 15 percent on that.”

RUHLE: But what about the argument that so many Chinese have now invested in their own market as an alternative because the real estate market is so poor there?

DRUCKENMILLER:

- “What about it? My first boss asked me a question when I was 22 years old. Do you know happens to the money when the stock market goes down? I said, I don’t know. It goes into the bond market. He said, no. It evaporates. It evaporates. You know what happens when stock prices go up? Wealth goes up. Confidence goes up. Economic activity generally goes up, so the more, the merrier.”

Very simple & very profound. But that didn’t work in America in 2nd half of 2000 or in Q4 2007-Q1 2009. On the other hand, the Chinese stock market was consolidating for a couple of years before this move up.

In any case, what does Mr. Druckenmiller own to benefit from China’ recovery?

DRUCKENMILLER:

- “… We just had a discussion about China. Analysts have been downgrading BMW and Volkswagen because of their Chinese exposure. What do you think happens with a weak Euro giving you an earnings tailwind if Chinese [sic] recovers — if China recovers? You got great companies like Airbus that now are much more competitive than they were against Boeing, but all our anecdotal evidence is Europe has actually turned. It looks pretty good.”

Kudos & thanks to Ms. Ruhle for getting this interview and for getting him to speak in such detail about his investing thoughts. The lady used to be a terrific salesperson, we are told. Well, now she has become a terrific journalist.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter