Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips –our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Yellen understood what Paulson/Bernanke didn’t in 2008

This week was the 7th anniversary of the Lehman disaster. Remember the talk then about how the Lehman filing was “priced in the markets” before it happened. We are convinced that both Secretary Paulson & Chairman Bernanke believed that a Lehman filing was priced into the markets. What made them feel so? On Friday, September 12, 2008, Lehman stock closed down 57 cents to $3.65, a suggestive price. So, in our opinion, Paulson allowed Lehman to file for bankruptcy without fearing any major consequences.

What Paulson/Bernanke had forgotten to consider was that the corporate bond market was confident that Lehman bonds were safe. And, if we recall correctly, the Lehman bond position on Friday September12, 2008 was valued at over $140 billion. Thanks to Paulson/Bernanke, these bonds were reduced to mere pennies on the dollar on Monday, September 15, 2008. Almost instantly, the CDSs of Goldman & Morgan shot up to the sky and a full systemic crisis was on. To say Paulson/Bernanke panicked would be a severe understatement. They begged the Congress for the $800 billion TARP and Paulson literally knelt before Speaker Pelosi to convince her of their desperate need.

This week Chair Yellen faced the same chorus of “Fed hike is priced in” before her decision. And it was priced in to the stock market as is now obvious. Indeed, as Guy Adami of CNBC FM kept arguing, the stock market expected it and wanted it. The world’s central banks expected it and the economist-journo crowd was lusting for it.

Fortunately for us, Chair Yellen understood that the stock market was NOT the primary market to decide whether a rate hike was priced in or not. She understood that the only market that had to reflect the “priced in” condition was the Federal Funds market. And that market was in the other camp in a resounding “no hike” condition. And this is the market that has had a 100% track record in predicting a Fed rate hike during the week it happens.

Had Chair Yellen yielded to the stock analysts, economists & journalists, she would have stunned the FF market. Then, as Jim Bianco had warned in his conversation with Rick Santelli on September 3, that market would immediately have priced in a much higher FF curve for next year and beyond.

History shows what happens when the Fed stuns the interest rate markets negatively – accidents. As Larry McDonald has pointed out on CNBC and in print, outstanding global credit is currently at $50 trillion, up over 100% from $22 trillion in 2005 & up over 50% from $31 trillion in 2010. Rarely have global credit markets been so exposed to a financial accident & rarely have global central banks become so utterly helpless to rescue markets from such an accident. This is why sagacious people like Art Cashin, Larry McDonald et al were warning about the dangers of a rate hike at this time.

Kudos to Chair Yellen. She understood the risks and stayed her hand.

2.Anger at the Fed & Fed’s principal mistake

The feeling was palpable:

- David Schawel ?@DavidSchawel – Anger seems to be the most common emotion associated with yesterday’s Fed decision. Peeps mad.

- David Zervos ?@zervoscorfu – This lack of economic confidence from the Fed will keep the QE haters chirping loudly and the market on edge! Quite a sad decision today!

- Joe Saluzzi ?@JoeSaluzzi – David Malpass: The Federal Reserve Pulls a Lucy http://www.wsj.com/articles/the-federal-reserve-pulls-a-lucy-1442531250 …

If the Yellen Fed is Lucy, who is Charlie Brown? All the traders/investors & economists/journos who had bought into, what they considered as, the sheer certainty of a rate hike or at least a hawkish commitment. Instead, they got a dovish action and a dovish statement. How dovish?

- David Rosenberg – The Fed decided to hold its fire and the bar looks to have been set vert high over the near term

The palpable anger was not about the Fed action but about being misled for the past several weeks. With all the Fedspeak we had heard, the comments from people in the know about the Fed being desperate to raise rates, too many people had become conditioned to expect a rate hike this week or at least a virtual promise this week of a rate hike to come very soon. How stupid must they have felt? No wonder the anger is so palpable.

And it is totally the fault of the Fed-heads and their abominable practice of constantly babbling on TV about their individual opinions. It got so bad that both Peter Fisher & Jim Cramer protested loudly four weeks ago :

- Peter Fisher on Friday, August 20 – “I think we also have to unpack a problem with the Fed here. … The Fed has been publishing, every member of the Fed publishing their own forward path of interest rates ; they have to get on one page; … They’ve been having a free lunch all of them explaining their own views … They need to get on one page on the path”

- Jim Cramer on Thursday, August 19 – “We need those people to shut up so the Fed can speak with one voice. News flash to the Fed: Your job is bigger and way more important than the NFL, so get some discipline and rein it in, for heaven’s sake. Frankly, it’s an embarrassment to the institution“

And guess what happened four weeks ago? The beginning of the August decline. But that experience hasn’t taught this Fed anything. Why? Because Fed-head Bullard will be on CNBC Squawk Box on Monday, September 21 from 7-9 am as guest host. Frankly, we blew our top when we heard this and sent an angry tweet to CNBC’s Kelly Evans who announced this with cc to Jim Cramer.

We all just heard from Chair Yellen. We read her statement and we heard her answer questions from a bunch of reporters for 45 minutes. This was two days ago on this past Thursday. So why do need to listen to Bullard on Monday? What can he say that is different from what Chair Yellen said on Thursday? Is he going to walk back part of her message and if so how do we know she agrees with what he will walk back?

Or is he there to massage & make cooing sounds if Monday morning is anything like the morning on Monday, August 24th? And will anyone really believe, with all due respect, whatever crap that Mr. Bullard will dish out? Shame on you, CNBC Squawk Box. You do this just because investors cannot sue you for tort, for delivering comments from a Fed-head who arguably has misled some investors in the past.

Sorry, folks! We are really fed up with the Fed and we just can’t keep our frustration bottled up anymore. We don’t want to hear from any Fed-head any more except for Chair Yellen.

3.Nature of Investor Fear & Repeat of August 19th?

Below is our description of what happened on the afternoon of Wednesday, August 19 after the release of the Fed minutes?

- “The minutes were more dovish than the consensus expected and that did lead to a fast rally that turned Dow positive from a 160 points drop on Wednesday morning. But the rally reversed almost immediately thereafter and the stock market closed down hard. The selloff accelerated on Thursday and the pace & ferocity of the selloff was more intense on Friday. It was as if the minutes had revealed a potential hike of 50-100 basis points in the September Fed meeting.”

Isn’t what happened on this past Thursday afternoon & on Friday a virtual replica of what happened from 2 pm on Wednesday 8/19 to the close on Friday 8/21? Last week, we suggested a possible bonfire of the shorts after the FOMC statement. It was that & more in the immediate aftermath of the Fed statement:

- Thursday – StockJockey ?@StockJockey – Small Speculators in Index Futures have had enuff

The S&P shot up to 2020 and then, as if on the proverbial dime, the stock market turned and fell hard. Friday morning was ugly and Friday’s close was just as ugly.

- Thursday – StockTwits @StockTwits – That was one ugly reversal; From highs to lows in a matter of one hour: http://stks.co/q2rgn $SPY

Both Friday 8/21 and this Friday 9/18 were options expiration Fridays. We know what happened on the morning of Monday, August 24. Let’s see what happens on Monday morning.

- Ed Bradford ?@Fullcarry – Equity risk premium after FOMC no hike statement

Why would dovish comments from the Fed lead to such selloffs? We had written on August 22:

- “So why the precipitous fall in the US stock market? We think people suddenly realized that the FOMC doesn’t have a clue. In a sudden stroke of mental lightening, investors realized that the FOMC is neither omnipotent nor omniscient. Forget being omniscient, people realized that the Fed doesn’t have a handle on the economy. And the belief in the infallibility of the Fed was the main foundation of the 5-year stock market rally. A rudderless economy piloted by a Fed that is almost clueless as the rest of us – that doesn’t justify current multiples, does it?”

- “All of a sudden, this light went on and the foundation on which the resilience of the US stock market was based suddenly crumpled.”

Frankly, the realization on this past Thursday was worse. Now it is not just about Fed being clueless. It is about the Fed being possibly helpless. The uber-dovishness of the FOMC statement sent a chill down the spine of many investors about the trajectory of the global economy. Every one knows that China is slowing hard. But the finger-pointing at China suggested that the Fed was worried about the China-EM slowdown possibly infecting the US economy. This suggested weaker global growth and that changes the investment case substantially. Look what the FF market has begun to price:

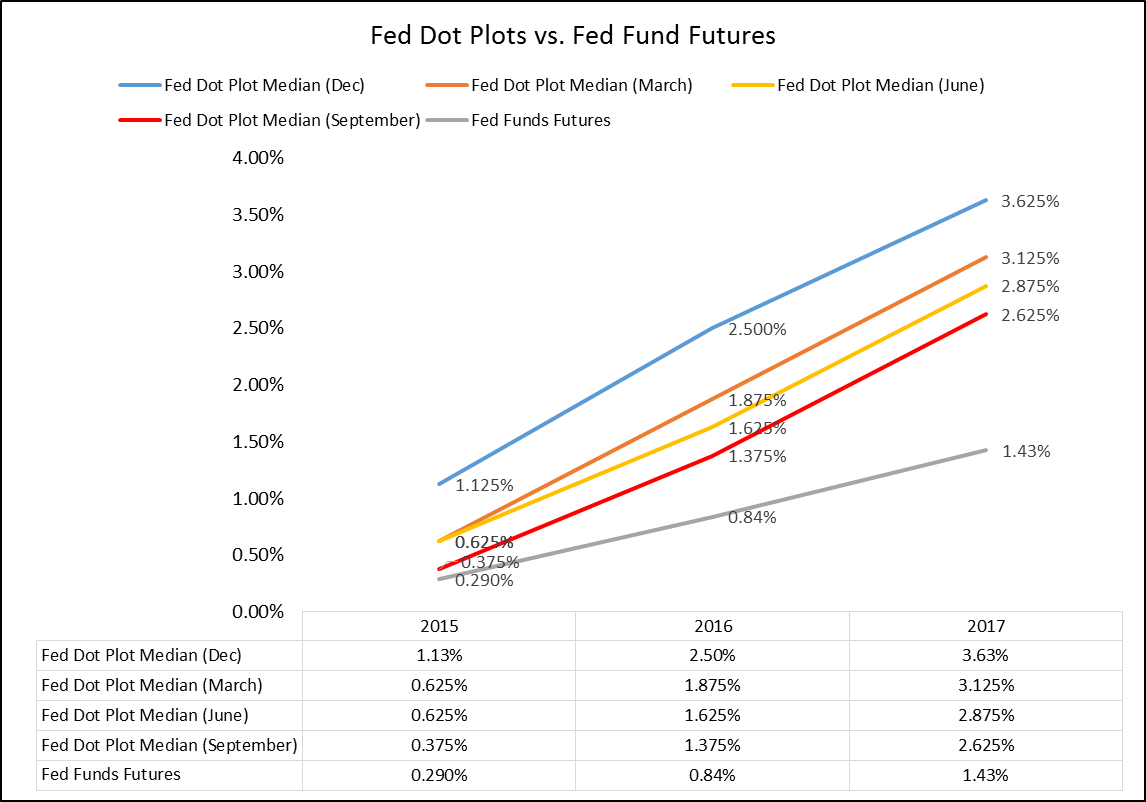

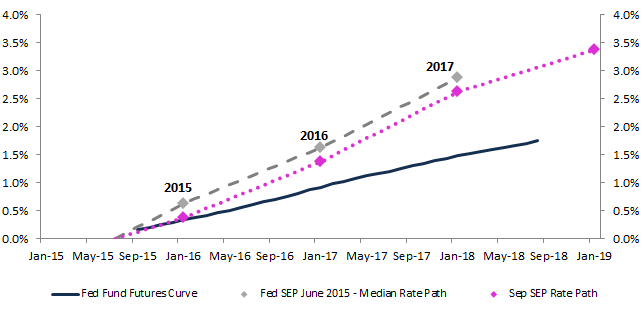

- Charlie Bilello, CMT ?@MktOutperform – Fed moves their dots lower yet again, appeasing the market. Market wants more, still a wide gap.

- Justin Wolfers ?@JustinWolfers – Fed funds futures markets continue to be more dovish than the #FOMC.

- David Rodriguez ?@DRodriguezFX – One Fed official actually foresees NEGATIVE Fed Funds rate in 2016. Wow.

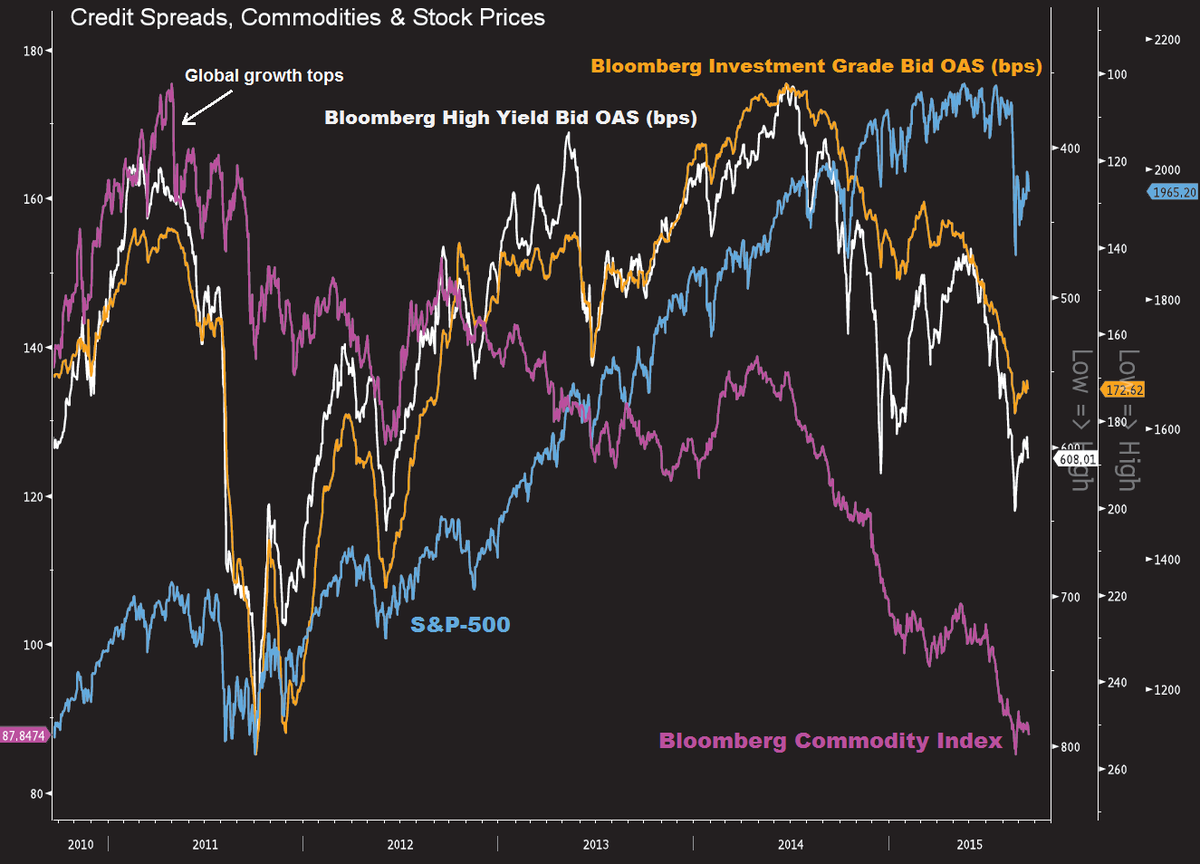

How would slowing global growth be represented in the markets? Like below?

- Antony Filippo ?@Vconomics – Credit spreads, commodities and the S&P-500

4.Curious Action of the U.S. Dollar?

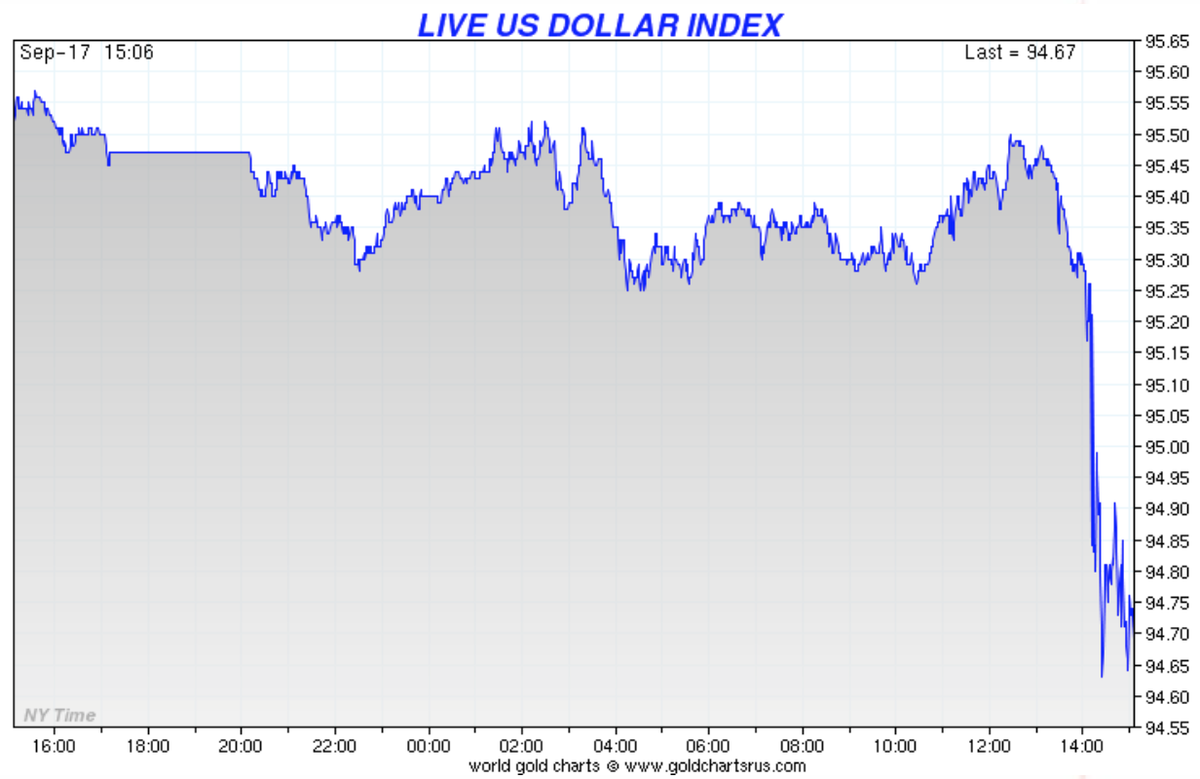

The Dollar behaved as it should have on Thursday:

- Thursday – Dan Popescu ?@PopescuCo – US dollar tumbles after Fed holds rates steady http://reut.rs/1KTXUMl via @Reuters

The Dollar opened weak on Friday morning and then it reversed to close up by 1%. In fact, DXY recovered its 200-day moving average at the close on Friday. One day or one weekly close doesn’t make a trend but the specter of a Dollar rally after a dovish Fed action brings back uncomfortable memories of 2008.

5.Treasuries – Tepper’s EM river reversing?

Yields rose across the entire curve for the first three days of the week. The selling seemed unrelenting and occurred regardless of the moves in the other asset classes. Frankly, it seemed as if some large holders were liquidating part of their positions ahead of the feared Fed tightening. This was despite large short positions in Treasuries revealed in CFTC data. Was that Tepper’s EM reserves river flowing out?

Then yields fell literally off of the proverbial cliff after the FOMC statement. From Wednesday’s close to Friday’s close, the 30-yr yield fell by 15 bps, 10-yr by 16 bps, 5-year by 17 bps, 3-yr by 15 bps & 2-yr by 13 bps.

We wonder whether the Fed’s stunning decision would reverse the outflowing of Tepper’s EM reserves river. It seems likely that China & other EMs might have sold a portion of their Treasury positions in fear of Fed’s tightening. The question is whether that selling has stopped at least for awhile after the FOMC decision.

We suspect so otherwise the steep fall in yields after FOMC might have been tempered by selling at higher prices by China-EM et al. We should get a better sense next week. Because the natural action in Treasury yields should be:

- J.C. Parets ?@allstarcharts – bond market been telling us rates staying lower for years. Now the short end of the curve is falling and also pointing to lower rates….

6. US Stocks

The big turn was on Thursday just after S&P touched 2020 after the FOMC statement. Kudos to traders who changed their direction just at the right time. A couple of tweets we noticed are:

- Thursday – DK1 ?@canuck2usa – $/ES_F got a few on short

- Thursday – Northy ?@NorthmanTrader – Our trade outlook has now changed.

- Thursday – Cousin_Vinny ?@Couzin_Vinny – $SPY $NYMO just hit +75 – shoot we could see something soon http://stks.co/e2Yr1

What about next week?

- Ryan Detrick, CMT ?@RyanDetrick – NEW POST: Here Comes The Worst Week Of The Year http://stks.co/j397t via @YahooFinance $SPY $DIA

- “I took a look at how the week after September option expiration does (so next week). Going clear back to 1990, this is the worst week of the year. Up just four times the past 25 years, wow”

- “Looking at how all weeks have done over the past 10 years, you can see the next three weeks are among the worst of the year“.

How bad could the decline get, not just next week but in the weeks ahead? Guy Adami of CNBC FM said “we will test 1820“. His colleague Steve Grasso was more explicit. He expects the S&P upside to be limited by 2020 and expects the 1867 level to be broken first and then 1820 and, if that, he can see a decline to 1600. But before 1867,

- Scott Redler ?@RedDogT3 – $spx 1925-1938 is pretty big support. A close below this and the rest the August lows chorus grows louder.

On an intermediate term:

- Thursday – Carl Quintanilla ?@carlquintanilla – McClellan sticks by his arcane (but prescient) guide: Eurodollar liquidity, which forecasts more stock mkt weakness

What might be a reason for breaking down to these levels, especially after a dovish Fed?

- John Kicklighter ?@JohnKicklighter – The $SPX isn’t following the familiar formula more QE time = buy dips. Pop that spec bubble, gravity takes over

After all, there are only two major choices:

- Todd Harrison ?@todd_harrison – .@CraigScott31 After 200% return in 6 yrs, only one way to turn; the other way is to continue. $SPX

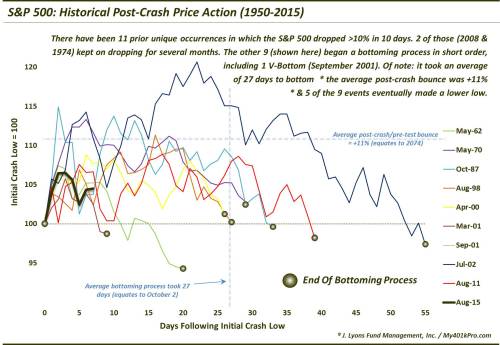

An intermediate term analysis from Dana Lyons titled What Happens After a Crash?

- “Here is a chart tracking each of the events from the day of their initial low until the final day of the bottoming process (the bottoming process was determined to be complete if it led to a rally of at least several months).”

- “This examination would loosely suggest that the current bottoming process (assuming we are in one) may possibly persist for another month, with a possible higher bounce along the way before a possible retest of the August 25 lows”

Any light at the end of this tunnel?

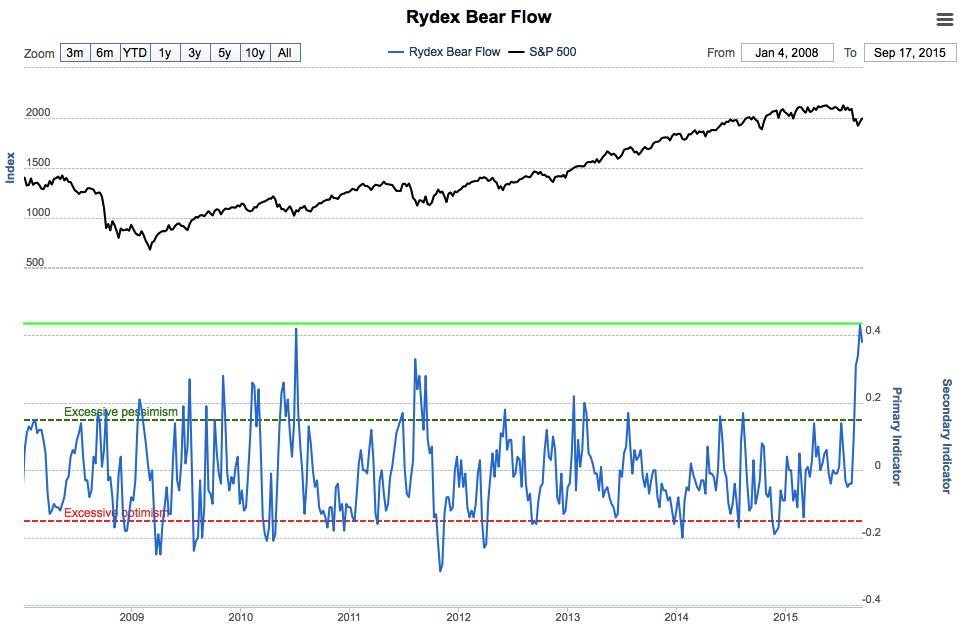

- Urban Carmel ?@ukarlewitz – Normalized flow of money into bear equity funds at an extreme (from Sentimentrader) $SPY $QQQ

7. Emerging Markets

China is the key to EM & to global growth. And China also determines the direction of the Tepper EM Reserves river. We are increasingly leaning towards a high probability of a Chinese QE and a resultant fall in the Chinese currency. This also means China will at least maintain a high balance in Treasuries. That may have been one reason for the unrestrained fall in Treasury yields on Friday. This is not a consensus view at this time but not a lonely one either.

- ValueWalk @valuewalk – China Planning A 20% Yuan Devaluation By Next Year? http://www.valuewalk.com/2015/09/china-massive-devaluation/ … $FXI

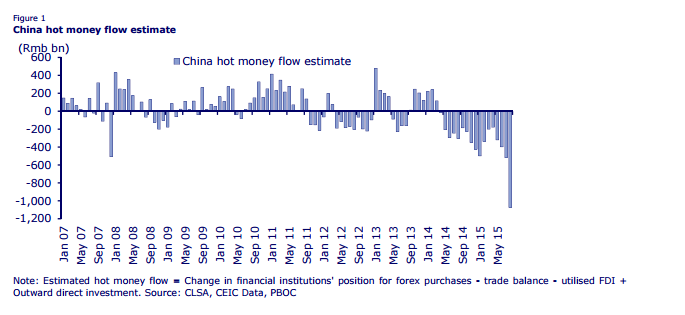

A different view about China’s need to bring back its Dollar reserves:

- ValueWalk @valuewalk – Has completely collapsed – G&F on China hot money flow estimate

Everything about China is huge & unprecedented. But especially ginormous is the level of assets in their banking system – $31 trillion according to Kyle Bass and that with GDP of $10 trillion. This is best heard from Kyle Bass in the video below:

8. Gold

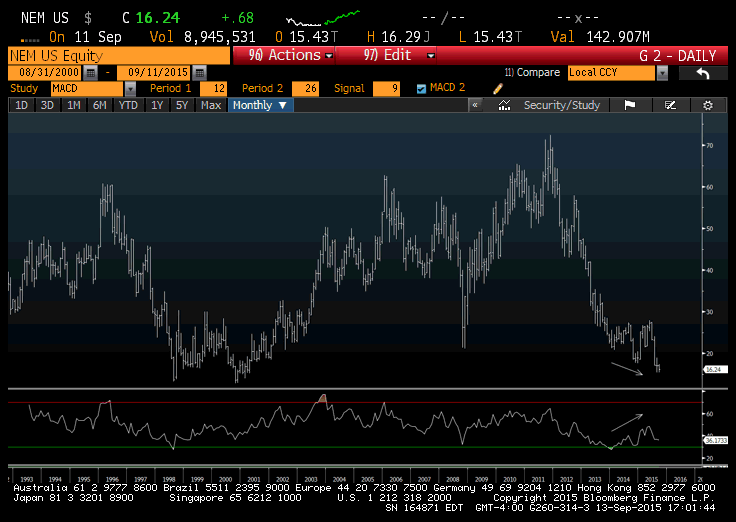

The best performing asset class of the week was Gold-Gold Miners. Kudos to Mark Newton for a terrific call:

- Monday – Mark Newton ?@MarkNewtonCMT – $NEM w/ Positive MTHLY divergence after testing lows from over 15 yrs ago-Fri saw TD Comb buys confmd, New 5dayHighs

- investFeed ?@investFeed – #BREAKING: #Gold prices spike over $10 an ounce following #Fed announcement. #FOMC http://www.investfeed.com

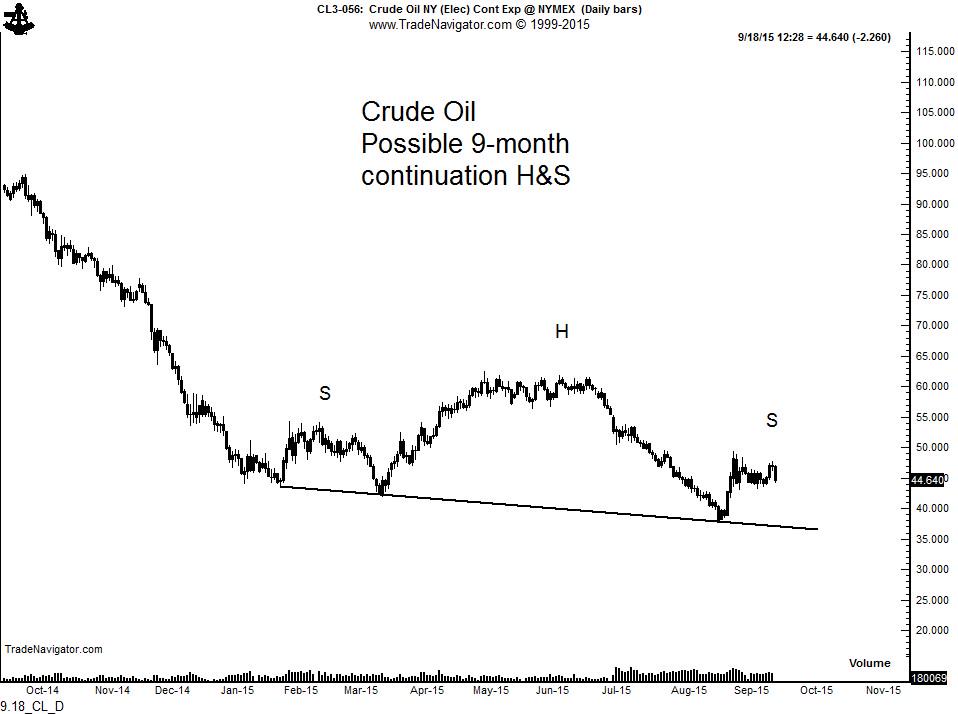

- Holger Zschaepitz ?@Schuldensuehner – Oil prices tumble as Wall Street selloff offsets rig data. http://reut.rs/1MfHxqD

- Peter Brandt ?@PeterLBrandt – $CL_F Might the continuation chart in Crude be building a H&S top formation — ABSOLUTELY

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter