Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Back to the Fed!

Interest rates fell; Treasuries outperformed credit; Gold & Silver rallied; S&P outperformed Russell 2000; Utes, Staples & EM handily outperformed financials & industrials. Isn’t that what typically happens after the Fed tightens in a mediocre growth economy? Isn’t that what happened in January 2016 & in January 2017 after the last two Fed rate hikes?

The action was pretty dramatic in a sleepy sort of way – 30-year yield dropped 10 bps & the 5-year yield dropped 8 bps, both handily outperforming the 2 bps fall in yields in corresponding German Bunds. Gold & Silver rallied by 1.4% & 2% resp while the Dollar declined by about 60 bps. Dow and S&P fell by 1.5% in the worst week of 2017 & Russell 2000 dropped by 2.7%. Utilities rallied by 1% and EEM rose by 9 bps.

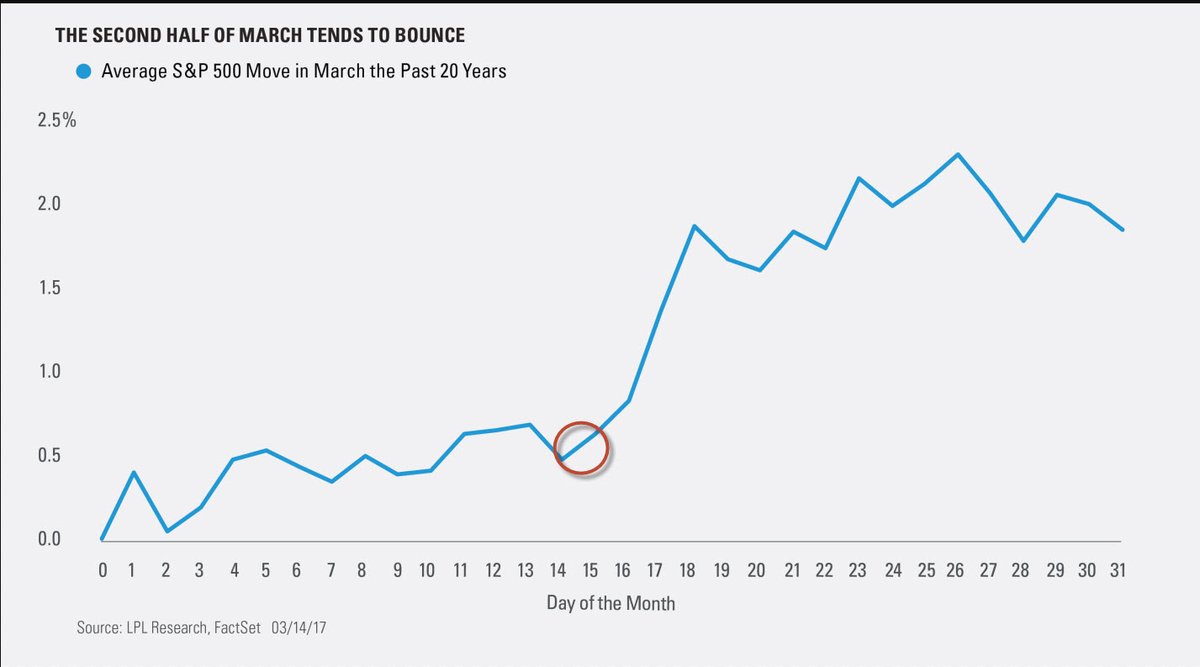

As we have noticed before, when the Fed becomes the big factor historical patterns & charts stop working. Remember the tweet below from last week?

- Ryan Detrick, CMT @RyanDetrick – March 15 – The past 20 years has seen the #SPX bottom now and rally the rest of the month … https://lplresearch.com/2017/0

3/15/can-we-expect-green-for-s aint-patricks-day/ …

Instead of rising this week, the S&P fell by 34 handles & the Dow fell by 318 points.The S&P broke 2350. Yes, this action could be attributed to the uncertainty about the Republican health care bill. So what happens now that we have certainty? Will the 10-year yield bounce off the 2.40% level? Will stocks bounce back from this bad week? So many indices & asset classes are perched on top of important levels & moving averages that it makes sense to punt today & wait for the markets to tell us next week.

Instead of rising this week, the S&P fell by 34 handles & the Dow fell by 318 points.The S&P broke 2350. Yes, this action could be attributed to the uncertainty about the Republican health care bill. So what happens now that we have certainty? Will the 10-year yield bounce off the 2.40% level? Will stocks bounce back from this bad week? So many indices & asset classes are perched on top of important levels & moving averages that it makes sense to punt today & wait for the markets to tell us next week.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter.