Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TACs is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Tuco’s Smarts

There is book-learning and there is real smarts. Book-learned people tend to lecture & prepare the opponent for what they are going to do. They usually get taught a lesson, like the lesson Tuco taught (from min 2:50 – 3:40):

[embedyt] http://www.youtube.com/watch?v=hnFdTXtFdSE[/embedyt]

“When you have to Shoot, Shoot. Don’t Talk” – How profoundly simple is this dictum? The Good, The Bad and The Ugly is an absolute classic. But we don’t think Chair Yellen and her FOMC club of elite Ph.D. economists have watched it. Had they watched it & understood the profound simplicity of Tuco’s smarts, they would raised rates interest rates by 25 bps this past Monday. They would also have said that the rate rise was in lieu of what they had planned to do at the FOMC meeting on Wednesday, March 14.

They didn’t have to listen to Tuco. They could have remembered old proverbs like “strike while the iron is hot“. And, was the iron hot by last Friday evening! That is why we exhorted them last week to raise rates “Now, Now. Now“. But they didn’t. Because they are all about themselves and process is more important to them than outcome.

Look at the outcome they delivered by making the markets wait an extra week in fear of what happens next Wednesday. The Dow and S&P suffered their worst week of the young year; Interest rates jumped up another week & Treasuries suffered their worst 9-day loss in years; Gold & Silver fell hard. And for the first time in awhile, high yield credit got slammed & gave up most of the 2017 gains.

Yellen doesn’t get what Bernanke never got. When they speak and make markets wait, the markets run far ahead of where the Fed wants them to go. And then they reverse after the anticlimax of Fed’s actions.

We showed last week what happened after the widely feared speech of Chair Yellen on Friday, March 3 – Reversal > interest rates fell, gold rallied and JNUG, the 3X gold miner ETF, jumped by 10%. That relaxation of tensions was an one-afternoon event. Fears returned on Monday and continued till the release of Nonfarm payroll number on Friday morning.The number was 235,000, higher than expectations, even a bit higher than the whisper number. So what happened on Friday? A bigger reversal > interest rates fell; Gold & silver rallied with JNUG up 15% on the day.

The Nonfarm payroll number actually decreased the probability of a rate hike next Wednesday from a virtual 100% certainty to a nearly 100% certainty. But, despite the “goldilocks” label on the 235K NFP number, the markets don’t know whether the FOMC statement & the Yellen presser will be hawkish or not so hawkish – meaning will she hint at 4 interest rate hikes in 2017 or reconfirm the 3 interest rate hikes she signaled on Friday, March 3?

Frankly, that depends on whether Yellen’s focus is on the actual state of the economy or on her seemingly obvious decision to get the Fed funds rate to 1.25%-1.5% before her term ends in February 2018. The unfortunate history of American Institutions is that the head of the institution is uber alles focused on how the Institution looks.

The last two weeks have shown that the intentions of the Fed are & remain the most dominant factor in & for markets. We have seen what happened after the Fed raised rates in December 2015 and what happened after the Fed raised rates in December 2016. Will that pattern repeat after the Fed raises rates on Wednesday, March 14?

Or will the markets react the way they reacted in 1994 – S&P merely meandered, rates exploded higher, long maturity bonds got torched, high PE stocks got shot and EM got almost obliterated. David Tepper believes that the stock market will find it hard to go up much and bonds will get torched – kind of a 1994 scenario. He believes so because he thinks regardless of the pace of the actions of Trump administration, the direction is correct and we will get there for sure.

In our opinion, what happens to interest rates from Wednesday 2:00 pm to next Friday’s close will point the direction. So we will follow the Latin dictum Festina lente and wait until Wednesday afternoon & Thursday morning to make haste.

2. Faint heart never won Lady Victory

Remember the demonetisation stunner from Prime Minister Modi – the sudden revocation of 86% of currency notes from circulation in November? Remember how it was supposed to damage PM Modi & how the Indian economy was going to slow down as a result of that mess?

Remember what we wrote on November 19, 2016?

- “In one stroke, PM Modi has convinced the common Indian that he is on their side, that he is their champion against the corrupt & the powerful. In one stroke, he has expanded his reach among every religious, ethnic, jaat & language group in Indian society. In one stroke and aided by the vitriol heaped on him by the political opposition, he has demonstrated that he is the only leader the Indian people can support with their heart”.

Today PM Modi delivered a stunning landslide in the mammoth state of UP decimating the entire opposition. His party needed to win 202 seats out of the state’s 403 seats. They won 312 seats, a win none of the pre-election polls or exit polls saw. UP has 220 million people, mostly poor & backward, broken up historically into multiple jaatis or ethnic groups. Identity voting has been the norm and so it was expected to remain in this election. Instead, it was a wave across all jaatis. Why?

PM Modi managed to override jaat-based calculus by an economic-class based drive. That is how the people had seen this demonetisation action – a blow that did inconvenience the poor & lower middle class but one that decimated the corrupt rich. You add this “Modi is for us” wave to his already stellar track record and you get a landslide in the biggest state in India. This will soon translate into a majority in the Upper House of Parliament where the opposition had blocked his economic reforms.

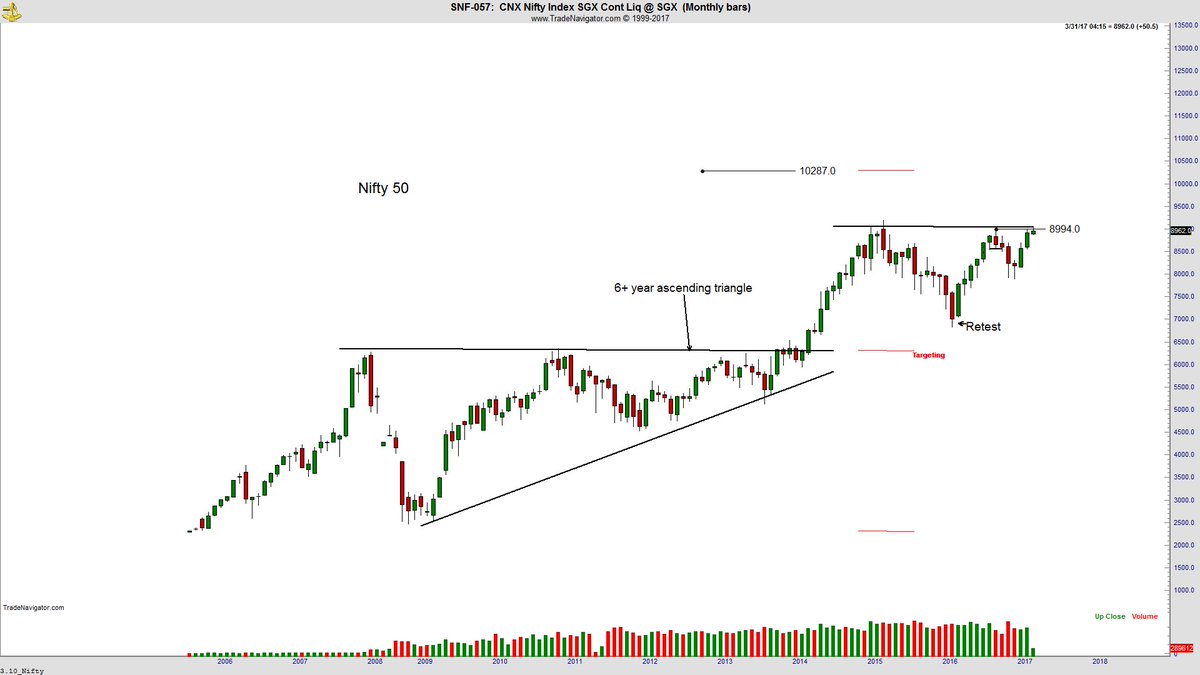

Guess technicals foretold this, right?

- Peter Brandt @PeterLBrandt – NIFTY $ZIN_F poised for new record high levels in its trend to 10,287, eventually 12,000

Does this election victory make India a Fed-free market?

Does this election victory make India a Fed-free market?

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter