Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.One Constant

What we discussed last week, all of us saw this week. Many things change in this market – Stocks go up & down; Dollar goes up & down; Gold goes up & down; 30-yr & 10-yr yields go up & down. But the rise in the 2-year yield is one constant in this market. Wednesday was the only day this week when the 2-year yield fell. By how much, you ask? Only by 0.4 bps, a rounding error from unchanged. On Tuesday, the entire yield curve including the 3-yr fell in yield but the 2-year yield broke company & rose up slightly.

Only one reason can explain this. The market believes that the Fed will raise rates in December. But that in itself doesn’t suffice to explain this market action. What about the below?

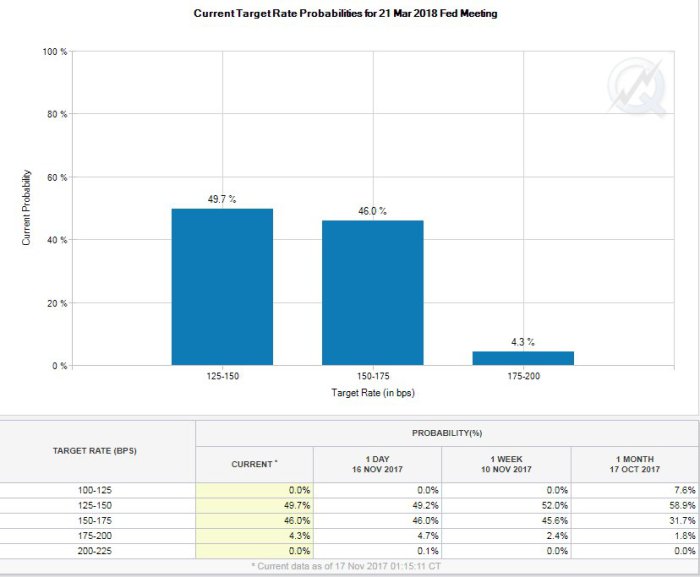

- Charlie BilelloVerified account @charliebilello – Probability of a March 2018 Fed hike (to 150 – 175 bps) has moved above 50%, highest level since year.

At the same time, the spread between 3-year & 2-year yields fell to 10 bps on Friday, a clear skeptical statement about future Fed hikes. If the 3-2 spread fell by 3 bps from 13 bps to 10 bps on the week, the 5-2 spread fell by 6 bps to 29 bps, a steep drop. This means even the belly of the curve is now rejecting the message of the 2-year. What about the long end? It is screaming “mistake” – the 30-year yield fell by 10 bps on the week and the 10-year yield fell by 6 bps while the 2-year yield ROSE by 6 bps on the week thereby flattening by 16 & 12 bps resp.

This just has to mean that it is time to buy the long end, right? We don’t know but some smart ones are saying precisely that based on patterns & on BAML fund manager data.

- Urban Carmel @ukarlewitz the path between here and higher yields is unlikely to be as straight-forward as is currently believed. New from The Fat Pitch https://fat-pitch.blogspot.com/2017/11/path-to-higher-yields-in-2018-unlikely.html …

$TLT

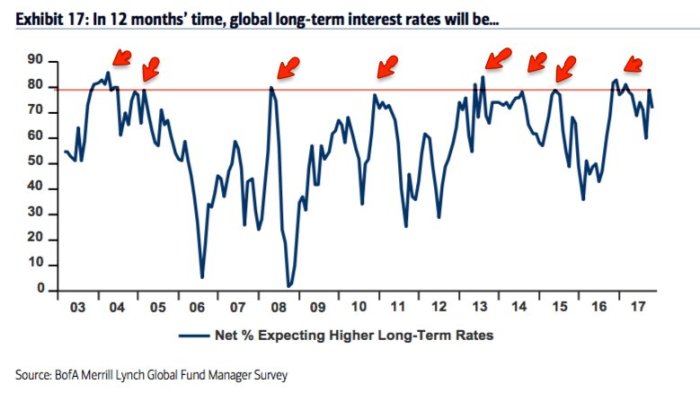

One nugget from this article – “Macro expectations are now nearly as high as at the start of 2017, which was a 4-year high“. Is there a pictorial representation of this high level of macro expectation? Urban Carmel provided it another article titled BAML Fund Managers Current Asset Allocation.

The above is their talk. What is their walk?

The above is their talk. What is their walk?

- “Fund managers are underweight global bonds, nearly to an extreme that has often marked a capitulation low in the past. Only 5% of fund managers believe global rates will be lower next year, a level at which yields have often fallen. …. A pure contrarian would …. overweight global bonds relative to a 60-30-10 basket. … Now in November, allocations to bonds dropped back to -56% underweight (-0.7 standard deviations below its long term mean). This is again approaching a capitulation low.”

Treasuries may rally further but isn’t High Yield much more important, at least right now?

2. US High Yield

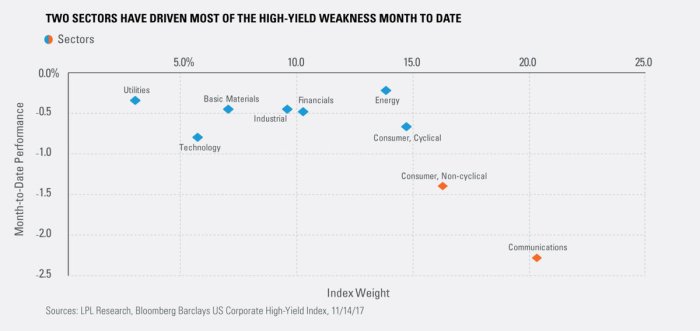

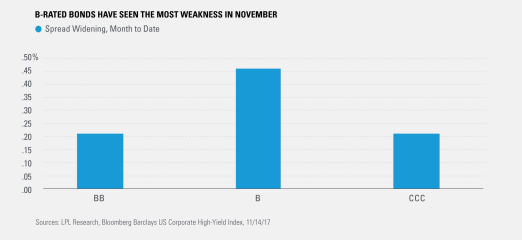

By now virtually every one has heard about the steep fall in HYG & JNK, high yield ETFs. But is this decline equally bad across all sectors?

- Ryan Detrick, CMT @RyanDetrick ICYMI Our latest

#LPLResearchBlog takes a look at high-yield and why all the alarms sounding on the group lately might be false alarms … https://lplresearch.com/2017/11/16/whats-happening-with-high-yield/ …

- “The good news is that so far, most of the weakness in high yield has been contained to a small portion of the market. When we break the move down into individual credit rating buckets, it is clear that B-rated bonds have seen the most weakness. Yet, if investors were expecting economic growth to falter, we would expect the lowest-rated CCC bucket to underperform as their weaker financial condition suggests that they would fare the worst in a broad economic downturn.”

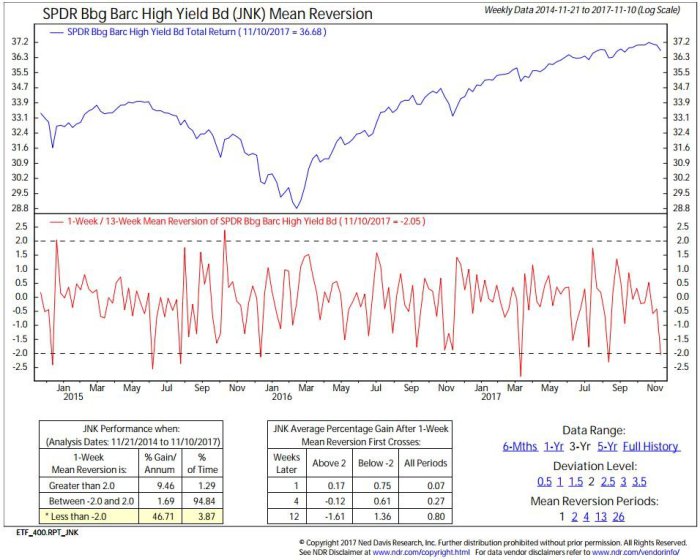

Well! If the decline in High Yield is not a symptom of broadbased weakness, then does it mean JNK or HYG may be ready for a rebound? Apparently, NDR seems to think so:

- Babak @TN – NDR’s

$JNK mean reversion model also suggesting that high yield here is a#contrarian buy h/t@dnleeson

Hmmm! If Treasury yields are likely to fall and if High Yield could rally, then wouldn’t it suggest the possibility of US stocks rallying?

Hmmm! If Treasury yields are likely to fall and if High Yield could rally, then wouldn’t it suggest the possibility of US stocks rallying?

3. US Stocks

What about the big rally on Thursday? So many attributed it to House passing the tax reform. Jim Cramer dissented on Thursday evening pointing out that the rally began in the morning & was in swing before the passage of the House bill. So why the rally on Thursday?

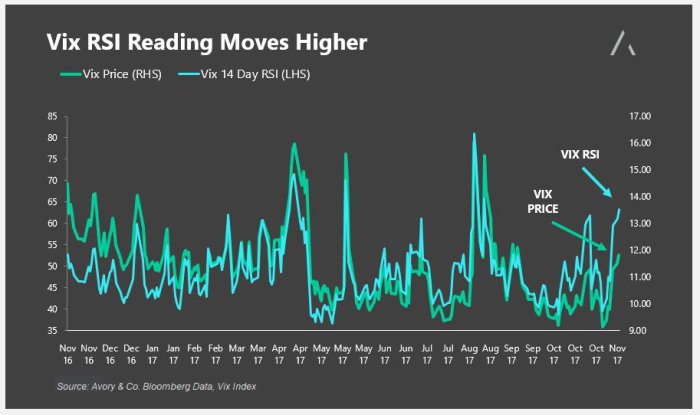

We did see a tweet saying that the Put-Call ratio by Wednesday’s close had reached pretty high levels. That was good but the real story for us was the action in VIX:

- Chart via @_SeanDavid & @AvoryCo – Wed Nov 15 – : “VIX RSI hitting overbought conditions despite the S&P 500 only .65% off all-time highs.” $VIX $SPY $STUDY

Yes, the 187 point rally on Thursday led to a 100 point fall on Friday. But that is deceptive because the 21 handle S&P rally on Thursday only gave back 7 handles on Friday and the 23 handle rally in Russell 2000 led to another rally of 6 handles in Russell 2000 on Friday. Mike Santoli pointed out on CNBC Closing Bell that Equal Weight S&P had outperformed regular cap-weighted S&P on Friday. A more detailed description was below:

Yes, the 187 point rally on Thursday led to a 100 point fall on Friday. But that is deceptive because the 21 handle S&P rally on Thursday only gave back 7 handles on Friday and the 23 handle rally in Russell 2000 led to another rally of 6 handles in Russell 2000 on Friday. Mike Santoli pointed out on CNBC Closing Bell that Equal Weight S&P had outperformed regular cap-weighted S&P on Friday. A more detailed description was below:

- SentimenTraderVerified account @sentimentrader For a day the S&P 500 declined more than 0.25%, the NYSE on Friday had the most positive breadth ever. Most advancing issues, volume and new highs since 1940.

Did smart guys think this action was bullish, at least in the short term?

- Greg Harmon, CMTVerified account @harmongreg – I know you are all ready for a crash and all, but a measured move out of the bull flag on

$IWM says 149.50 next

Ok, but are we likely to thank the S&P on Thanksgiving?

What about technicians & seasonality?

- See It Market @seeitmarket NEW Blog: “Seasonality Should Help To Extend Stock Rally Into Next Week” – https://www.seeitmarket.com/seasonality-should-extend-stock-market-rally-into-next-week-17487/ … by

@MarkNewtonCMT$SPY$SOX$JNK

4. Give us your tired… wretched refuse … tempest tossed .. homeless

Investors said that late this week, not the Statue of Liberty. And they enveloped in their eager arms the tempest tossed wretched refuse of the past 6 months that had been thrown out of their homes in investor portfolios. Footlocker, one of the worst of these, rallied 36% this week, 28% of which was on Friday. Why? Because they were deemed just very bad and not the utterly wretched.

Even the biggest daddy of store-based retail, Walmart, exploded up by 10% on Thursday in an explosive carnage of shorts. Imagine a $300 billion company rallying by 10% in one day!

All this happened without Amazon, the force of the tempest, suffering even minutely. The realization is dawning that store-based retail may be a valuable asset after all and that may be the right message of the Amazon-WholeFoods deal, as some of us have maintained since that day.

If the message is that the twain of online & store-based retail shall meet, then we might well see a price war and a natural degradation of multiples, especially if it goes the way of that ancient meeting of the twain of Cable Companies & Phone companies.

5. US Stocks vs EM Stocks

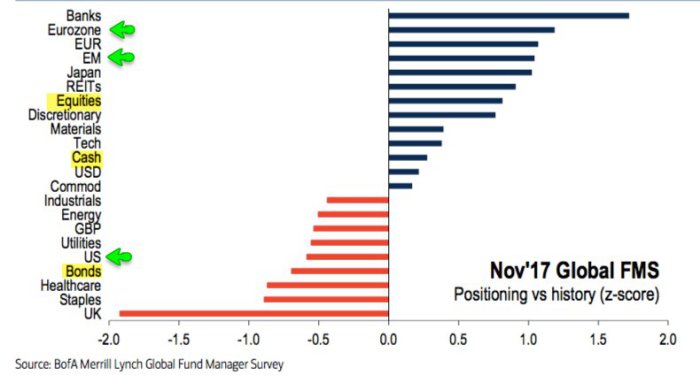

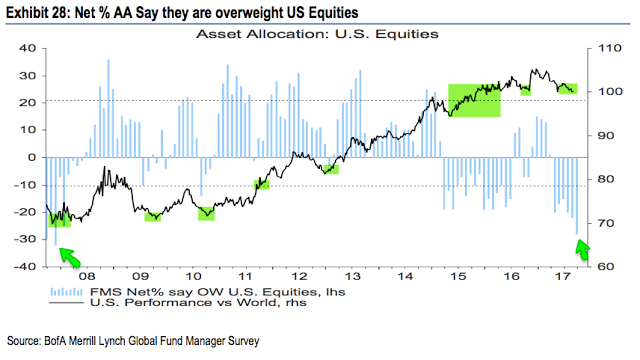

It is consensus now that non-US stocks should do much better than US stocks. Jeffrey Gundlach is probably the most outspoken advocate of this thought. He may well be right but is there a short-term opportunity for US stocks to outperform both Europe and Emerging Markets? That seems to be the message conveyed by the BAML Fund Manager survey:

- Urban Carmel @ukarlewitz After a 21 month rally, fund managers get bullish. Cash at 4-yr low, equity allocation at 2-1/2 yr high. New from The Fat Pitch https://fat-pitch.blogspot.com/2017/11/fund-managers-current-asset-allocation.html …

- “Within equities, the US is significantly underweight while Europe, Japan and emerging markets are significantly overweight. … Fund managers have since dramatically dropped their allocation to the US. … US equities should outperform.”

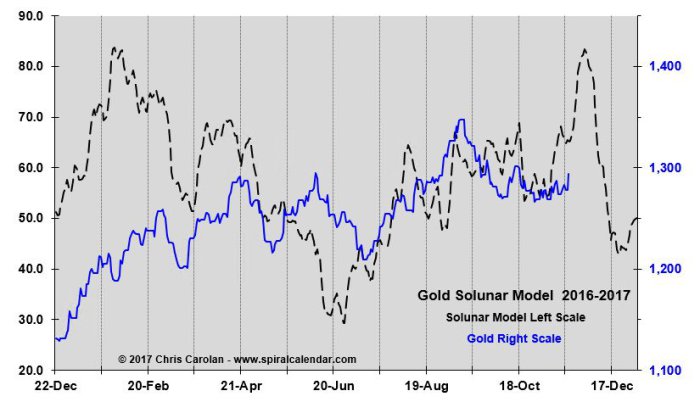

6. Gold

6. Gold

Gold had a good week with a 1.4% rally. Almost all of that came on Friday. What now?

- Carolyn Boroden @Fibonacciqueen We needed a lot of patience for this Gold to start moving!…minor target 1 was met today after holding symmetry…ratchet up your stops if you were in it!

On the other hand, seasonality seems positive in the short term according to:

- Chris Carolan @spiralcal Gold has a serious seasonal tail wind for the next two weeks.

$GC_F

7. Gundlach’s favorite long-term ETF

Despite recent recovery, there is a great deal of skepticism about the two big reforms that were enacted in India recently. We have tried to explain the reality in our rather simplistic way. This week, we feature two “expert” opinions that might shed some light.

First came from Moody’s on Thursday, November 16:

- “Moody’s upgraded the Government of India’s local and foreign currency issuer ratings to Baa2 from Baa3 and changed the outlook on the rating to stable from positive. Moody’s has also upgraded India’s local currency senior unsecured rating to Baa2 from Baa3 and its short-term local currency rating to P-2 from P-3.”

- “Moody’s has also raised India’s long-term foreign-currency bond ceiling to Baa1 from Baa2, and the long-term foreign-currency bank deposit ceiling to Baa2 from Baa3. The short-term foreign-currency bond ceiling remains unchanged at P-2, and the short-term foreign-currency bank deposit ceiling has been raised to P-2 from P-3. The long-term local currency deposit and bond ceilings remain unchanged at A1.'”

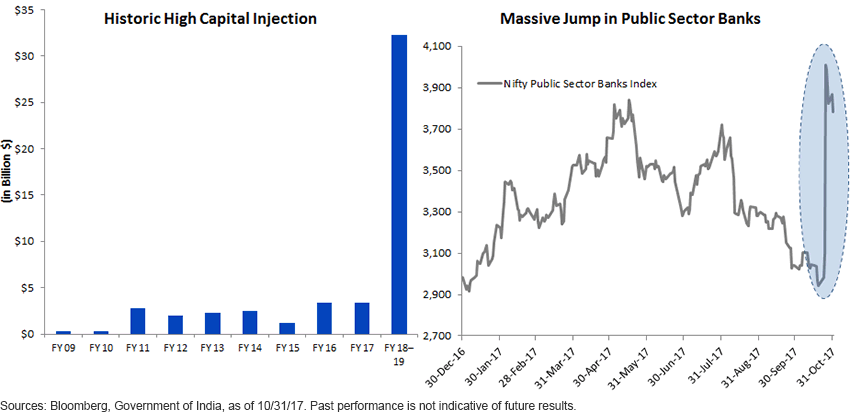

Second came from WisdomTree. The important discussion in this article is about the recent liquidity injection of $32 billion into India’s banks:

- “In a major announcement last month, the Modi government pledged $32 billion in capital for these beleaguered state banks—$20 billion will come from recapitalization bonds issued by the government, while banks will raise another $12 billion from markets. To give you a sense of the magnitude—this capital injection is higher than the cumulative injection of the last decade! (See Historic High Capital Injection chart below.)”

- “Until now, there has only been a partial transmission of lower rates to the economy. In spite of this, the market has responded with double digits so far. When you combine a complete transmission of cheaper credit, now poised to happen, with a cocktail of ongoing reforms and their benefits, I think India’s market is just starting a multiple-year bull run.”

As the above article says, Morgan Stanley predicts a triple for Indian Stock Market over next 5 years. This week Gundlach went further and said INDA, the iShares ETF for India, “… could go up 1,000% in the next 20 years, just like China did.”

Perhaps, many don’t get it because they simply don’t understand the relentless power of hundreds of million people getting higher incomes from higher education & greater opportunities. For them, the picture below.

In how many places around the world, do you see a poor girl doing her homework while selling peanuts et al on the roadside? The expression on her face shows how happy she is studying. Because she knows that is the key to a better life for her.

In how many places around the world, do you see a poor girl doing her homework while selling peanuts et al on the roadside? The expression on her face shows how happy she is studying. Because she knows that is the key to a better life for her.

That is one reason Gundlach says hold your Indian stock market ETFs for 20 years and make your grandchildren rich.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter