Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.The Really Big Story of the Week

No, we don’t mean the raising of tariffs on Chinese exports. That is a big story but really not that big. Why? Look how the US Stock Market behaved this week. Every morning, US indices opened down; went down a few hundred points & then rallied from there to close modestly down. Because the Chinese tariffs are not that big a factor for the US market & the US economy.

But the reality is that President Trump has drawn a bead on China. And the real reality is that whenever America has drawn a bead on a foreign adversary, America has proceeded very methodically & very smartly to squeeze their options & strength to provoke them into a conflict America can win. The Soviet Union is the most recent example. They were a major challenger & where are they now? The other example is Japan from the 1930s, the example most relevant to today’s conflict with China.

For a broader & possibly deeper discussion of this week’s tariffs action, see our adjacent article titled China’a Ignorant Arrogance – President Trump’s Smarts; Back to 1930s USA vs. Japan.

The Trump team understands that the real adversary in this trade fight is the U.S. stock market and not China. So the news releases are managed as carefully as possible to not change the bullish tenor of the U.S. stock market. And, frankly, the tenor of the U.S. stock market depends much more on the Fed than on Chinese tariffs.

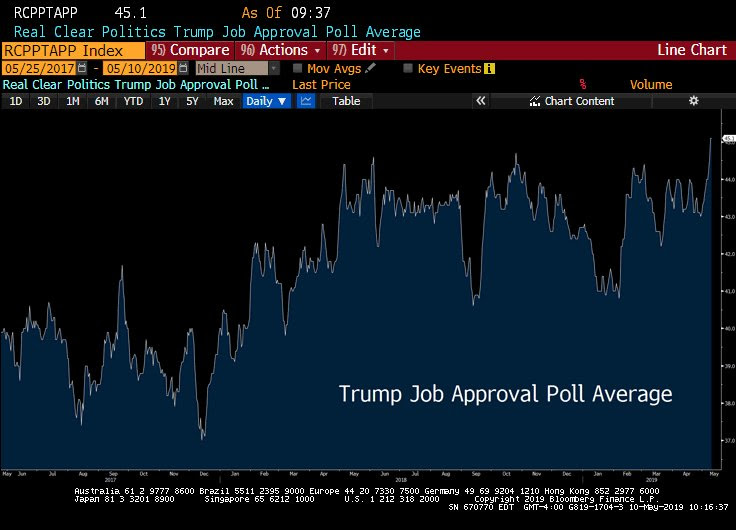

On the other hand, we think this week’s tariffs action on China will make President Trump more popular as the defender of America. But how popular is he now? Look at the chart tweeted by Larry McDonald (@convertbond) of Bear Traps Report:

And that is without this week’s truly big deal, this week’s verbal agreement. What verbal agreement you ask? An agreement that, according to previous comments of Mohamed El-Erian, will take the US GDP trajectory to a sustained 3% handle – a Trump-Pelosi-Schumer agreement on a $2 trillion infrastructure program. Read the accolades from Democrats for President Trump:

- Schumer – “We agreed on a number, which was very, very good, $2 trillion for infrastructure, … Originally we had started a little lower; even the president was willing to push it up to $2 trillion. And that is a very good thing”

- Peter A. DeFazio, (D-Ore.), chairman of the House Transportation and Infrastructure Committee – “It was a good, positive meeting, … the President spent a good time listening, and then he had things to say on his own. It was pretty balanced. He responded to points that were made and made points of his own. “

Who do the Democrats think President Trump is? FDR? They would be right if they did. Remember what we wrote on January 23, 2016 just before the Iowa Cacus in our article Reagan, FDR, & Nixon – 2016 Election:

- “It would actually be easier for Donald Trump to move left & adopt the FDR banner than it would be for Bernie Sanders to move right to appeal to Reagan supporters”

Donald Trump was a life-long Democrat; he loves building things & he has always been attuned to what construction & industrial workers think. He has great respect for President Reagan but his heart was always with FDR type policies. So when he needed Republicans in 2016, he emulated Ronald Reagan. Now the Republican Party is his. However, he needs blue collar Democrats & Big 10 country to back him in 2020. So he is now gravitating to where his heart has been – FDR type infrastructure program that will bring jobs to blue-collar urban labor & their unions.

2. President Trump & the Fed

How would you fund a 2 trillion dollar infrastructure program? First you need low rates, really low rates. Rates are already low, lower than most would have bet on at the end of 2018. But they are not low enough to raise $2 trillion. What if the Fed lowers interest rates by 100 bps and that gets the 10-year rate to 2% (already a forecast among many economists) and the 30-year rate to 2.5%?

At those rates, could the U.S. Treasury raise $2 trillion by launching a 30-year Treasury bond that pays about 2.5%? Hasn’t Secretary Mnuchin spoken wistfully about such a possibility? Hasn’t Jim Cramer publicly advocated such a program on TV with his usual passion? The structure & incentives could be negotiated but the need for such a bond would be obvious to many, especially the Pelosi-Schumer-DeFazio wing who want to show why the middle class & labor should vote for them in 2020.

Would Chairman Powell actually oppose such a joint Trump-Pelosi-Schumer demand? Especially when the Treasury market is almost screaming for a rate cut at the next FOMC? Would Chairman Powell oppose this when his own colleagues like Dr. Brainard are already talking about “the possibility of targeting longer-term interest rates as a “new” tool to combat the next recession.’”

Even the Fed should realize that a $2 trillion infrastructure program would inject such enthusiasm & related capex that it might actually avoid the “next recession” or postpone it by a couple of years.

3. Need for a rate cut

Let us count the reasons. First, even after the rise in rates on Friday, the 3-month yield closed the week at 2.431% (1-month yield at 2.432%) while the 10-year yield closed at 2.465%. So the 10yr-3mo spread is down to 3 bps & so is the 10yr-1mo spread. And the entire 7yr-3mo (& 7yr-1mo) spread is negative or inverted.

This is AFTER Chairman Powell told us current level of inflation is transitory. Secondly, Powell could be & is, in someone’s opinion, wrong:

- David Rosenberg @EconguyRosie Fade today’s PPI headline. The core consumer segment was flat as a pancake. Core intermediate PPI was -0.4% and core crude was -1.2% (-4.5% YoY) so the leading ‘pipeline’ price measures are melting away. Doesn’t look too “transitory”, Mr. Powell.

Rosenberg added on Friday:

- Hints of Deflation – The key as always is the core and for the third time in a row, it printed +0.1%

- Jesse Felder @jessefelder – ‘The economy may be going gangbusters as job gains defy estimates, but something is amiss in the household sector, the driving force behind the world’s biggest economy.’ https://www.bloomberg.com/

opinion/articles/2019-05-08/ the-mighty-u-s-consumer-is- struggling … by @DiMartinoBooth

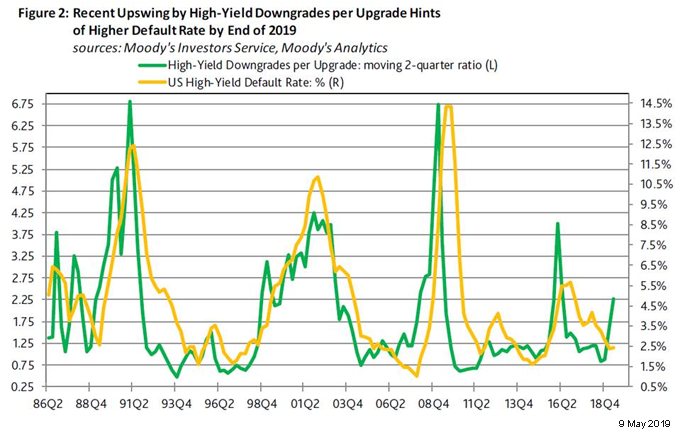

The fourth reason is the trend in credit, the foundation on which the stock rally rests:

The fourth reason is the trend in credit, the foundation on which the stock rally rests:

- Jenna & John @StrategicBond – Moody’s reporting thus far in 2019 that US high yield downgrades outnumber upgrades by a 2.28:1 margin. They say the longer that high yield downgrades double upgrades, the more likely are a pronounced widening of spreads and a worsened outlook for defaults.

In contrast, how did credit act on Friday? Look at what https://themarketear.com posted on Friday:

- Huge move lower in US credit, CDX IG. We have not seen such a big move lower in credit in a very long time.

This is the conundrum. Does the medium term deterioration matter or the bounce we saw on Friday? We think medium term deterioration is harder to reverse if not stopped preemptively.

Did all this turn a skeptic into a buyer this week?

- Douglas KassVerified account@DougKass – Pieces of paper yielding 2.3%-2.45% seems fine to me given the economic, political and market uncertainties.

-

Douglas KassVerified account@DougKass – For those that are less aggressive and risk averse, I suggest that the front end of the curve (two years or less) represents an excellent risk free rate of return relative to equities and inflation.

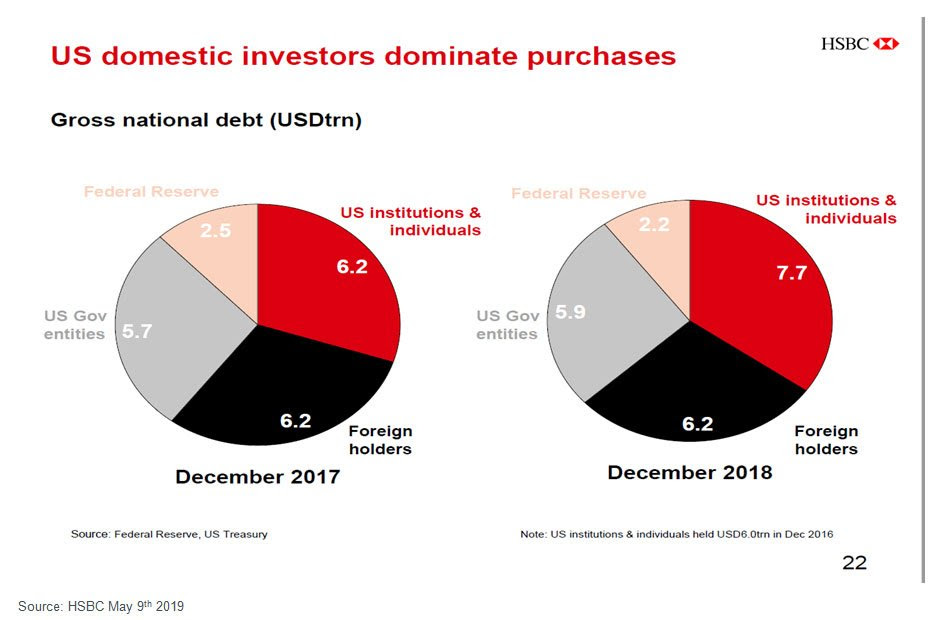

Doug Kass may be a new convert but others like Rick Rieder & Henry McVey have spoken about a shortage of quality bonds, something borne out by the strong demand for Treasuries:

- Jenna & John@StrategicBond – Too much focus on the supply of Treasuries (deficits) and not enough on demand. US domestic investor demand picked up last year to meet the extra supply.

What better proof of demand than this week’s fall in rates by 6-8 bps despite lackluster Treasury auctions? Perhaps the hardliners in Beijing should look at US domestic demand for Treasuries.

It might be more important for Fed Chairman Powell to see the writing on the Treasury rates wall. Especially when his colleagues are already discussing what the Fed should do AFTER the Fed reduces the overnight rate to Zero.

- Jesse Felder@jessefelder – ‘Federal Reserve Governor Lael Brainard on Wednesday became the second U.S. central banker to talk about the possibility of targeting longer-term interest rates as a “new” tool to combat the next recession.’https://www.marketwatch.com/

story/the-fed-is-dusting-off- a-qe-replacement-last-used- during-world-war-ii-2019-05-08

- “Once the short-term interest rates we traditionally target have hit zero, we might turn to targeting slightly longer-term interest rates—initially one-year interest rates, for example, and if more stimulus is needed, perhaps moving out the curve to two-year rates,”

- “Under this policy, the Fed would stand ready to use its balance sheet to hit the targeted interest rate, but unlike the asset purchases that were undertaken in the recent recession, there would be no specific commitments with regard to purchases of Treasury securities,”

Here is an idea, Chairman Powell – try to prevent the next recession instead. How, you ask? Cut the Federal Funds rate by 25 bps in the next two FOMC meetings.

4. Stocks

First thanks to Raoul Pal for introducing The Market Ear to all of us. Their chart below highlights the important action of the week:

- “Two huge days of rejecting the downside in SPX. It could get interesting if they take this higher, as “upside panic” has been very strong during 2019.”

The entire week featured down moves overnight leading to a low by mid to late morning & then a bounce to reduce the losses. And the week was a bad one down 563 Dow points & all major US indices down 2%-3.3% . But could this week prove the adage what ends well is well?

The entire week featured down moves overnight leading to a low by mid to late morning & then a bounce to reduce the losses. And the week was a bad one down 563 Dow points & all major US indices down 2%-3.3% . But could this week prove the adage what ends well is well?

- Mark Newton@MarkNewtonCMT – $SPXhourly futures chart shows prices having exceeded the highs of this 5 day Trend channel – a “CONSTRUCTIVE” bounce… http://newtonadvisor.com@NewtonAdvisors

How about a picture that says many many words? Below from The Market Ear :

- “Put call ratio closed at the highest levels since the Christmas panic.

The crowd is great at buying hedges at the wrong times, and love buying puts just when markets are about to bounce higher. Let’s see how this one plays out….”

From another smart veteran:

- Todd HarrisonVerified account@todd_harrison – $SPX2825 close enough?

But all of the above was just around the close & before the Lighthizer statement on Friday evening about the Unites States “preparing to raise tariffs on almost all Chinese imports that remain untaxed, valued at $300 billion.”

Also the above is more driven towards next week. What about the next few weeks? Below is a clip from Caroline Boroden, a technician who works with Jim Cramer. She sees serious warning signs. Watch & listen to Cramer explain her methodology of price symmetry & high-to-high cycles.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter