Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. What a stupendous stunner?

Something that transcends the usual, something that is so phenomenal that even people who have seen it all get utterly moved. We are talking about what veteran Dan Dierdorf said about the amazing demolishing by Michigan of a powerful Ohio State team that many thought would win the national championship.

This was not just a win but a stunningly physical beatdown of the vaunted Ohio State lines, both defensive & offensive. An additional fuel was, in the words of Michigan Defensive End Aidan Hutchinson,

- “yah man, I mean these guys have been disrespecting us, stepped on our jerseys, talking about hanging 100 on us, doing all the rah, rah talk; but we were about it today”

Something like that happened on Friday, December 3, 2021, the day of the November Non Farm Payroll report. Everyone who spoke about it raved about the internals of the report & what that showed about the U.S. Economy. Bob Michele of JPMorgan Asset Management did not get as personally emotional as Dan Dierdorf did about Michigan but he was almost as eloquent (on BTV Real Yield) describing both the report & the economy as terrific and saying business is as good as it gets. Rick Rieder called it a good report across the board without any ambiguity. Even the usually un-rosy David Rosenberg was ebullient (for him that is):

- The Great Thaw – What an incredible employment report. …. what is really important is that the participation rate rose (finally!) from 61.6% in September and October to 61.8% in November. This was the first expansion since July and the level is at the highest point since March 2020.

Rates in the belly of the Treasury curve did rise as they should have. But then something stunning happened. Rates began falling & kept falling hard across the entire curve all through the day. So hard that normal technical levels were pushed aside just like the Ohio State Defensive line:

- 30-yr yield closed down 7.5 bps to 1.69% ; 20-yr closed down 7.2 bps to 1.78% (thus inverting the 30-20 yr curve); 10-yr closed down 8.4 bps to 1.36% (well below important 1.40% level); 7-yr closed down 8 bps to 1.31%; 5-yr closed down 6.5 bps to 1.14%; 3-yr closed down 3.5 bps to 85.8 bps & the 2-yr closed down 2.5 bps to 59 bps, breaking 60 bps level.

Just about everybody knew what had happened in the Michigan – Ohio State game, but hardly anyone knew what happened on Friday to interest rates, especially the 30-yr rate. Not even David Rosenberg who asked for thoughts:

- David Rosenberg@EconguyRosie – Taper, inflation, rate hikes, wage spiral, fiscal blowout, depleted labor supply, rampant asset inflation all ‘in the market’, and yet the long bond yield today is lower than it was in the worst part of the 1930s Great Depression. Thoughts welcome!

Scott Minerd had said on CNBC Fast Money on Thursday (day before the NFP Friday) that if the 10-year yield breaks 1.40%, then it will go to 1.20%. But during those comments, Minerd said something we had not heard from such acclaimed prognosticators:

- “… there is something going on here, something I have never seen in my career and even in history I can’t find, the fact that real rates of interest are so low to maintain economic growth; there is something structurally different about this expansion; .. “

Before we get there, could we hark back to Friday October 22?

2. What a call? The Khan of All Khans!

If we recall correctly, the week that ended on October 22 was a week of celebration of 10-years of CNBC Half Time Report hosted by Scott Wapner. The bond guy was left to be the last guest of the week. But it proved to be a great illustration of “the last but not the least” saying!

Think back to the magnificent call Jeff Gundlach made on that Friday, October 22 to Scott Wapner:

- “Long term Bonds do make sense with 30-year Treasury at 2%+; with all the debt, be alert to debt deflation; 30-yr at 2% can give you a 30% return because the yield can fall to 1% as it did in Covid.”

Want to know how well that call worked? TLT, the 20-year Treasury ETF, is up 7.1% since October 22 and EDV, the Zero-coupon ETF, is up 9.4%. Yes, the 30-year yield is actually down 38 bps since its 2.07% close on Friday, October 22.

Remember Genghis, Ogadei, Kublai? They were not only Khans of the Mongols but their title was Khan of All Khans because their writ was supreme. In a similar vein, the 30-year Treasury bond is the Bond of All Bonds. Just look how the post-October 22 rally in the 30-year bond has contracted the Treasury yield curve:

- the 30-2-year spread has contracted by 51 bps; the 30-3 year spread has contracted by 46 bps. The 30-20 yr spread has inverted with a negative 9 bps spread; the 10-7 yr spread has contracted by 16 bps to 5 bps & could invert soon.

A week and half after Gundlach’s call, Ian Lyngen of BMO said the following on BTV Surveillance:

- “… pain trade is towards lower yields … rates grind down for end of the year towards 1.25% – 1.35% ; consistent with trading environment this year”…

The 10-year yield closed at 1.36%, just a basis point from 1.35% and, if Minerd proves correct with 10-year yield going to 1.20%, then Lyngen’s call would come true.

Think back to Aidan Hutchinson’s (Michigan Defensive End) comments about the disrespect shown by Ohio State players. Such fuel of disrespect doesn’t only galvanize a beatdown in Football but it also leads to a demolishing of disrespecters in Treasuries. Recall the tweet dated October 19 from BTV’s LA:

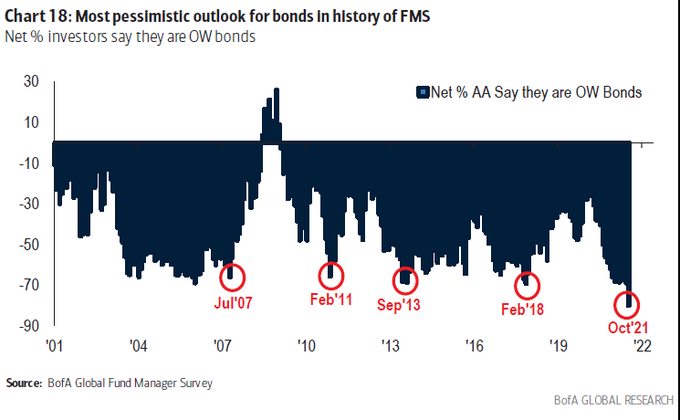

- Lisa Abramowicz@lisaabramowicz1 – – Fund managers’ allocation to bonds fell to the lowest level ever in the latest BofA fund manager survey as inflation woes drove expectations for higher rates, via@theterminal

Now that’s what we call fuel for a Treasury rally. What we don’t know how much of this fuel has been used up in the 38 bps rally in the 30-year. Could Ms. LA enlighten us?

Actually & to be absolutely frank, the man who drove this Treasury rally is neither Gundlach nor Lyngen. And he only began driving this rally just before Thanksgiving. Who is this man, you ask?

3. Hail to the Chief

That man is Fed Chair Jay Powell. Just look back to how the Treasury curve closed on Tuesday, November 22:

- 30-yr up 6 bps to 2.04%; 20-yr up 7 bps to 2.09%; 10-yr up 6 bps to 1.68%; 7-yr up 4 bps to 1.59%; 5-yr up 2 bps to 1.35%; 3-yr up to 95 bps; 2-yr up to 61 bps.

Then came Wednesday and Treasury rates fell with 30-yr down 6 bps. Now fast forward to Friday after Thanksgiving:

- 30-yr yield fell 13 bps; 20-yr fell 14 bps; 10-yr fell 15 bps; 7-yr fell 16 bps; 5- yr fell 15 bps; 3-yr fell 14 bps & 2-yr fell 12 bps.

No it was neither the Turkey nor any wine. It was the minutes of the November Fed minutes released on Wednesday, November 24 afternoon. And, by the way, on that post-Thanksgiving Friday, the Dow fell 905 points, the S&P by 107 pts, NDX by 342 points, RUT by 86 pts & Transports by 611 points.

Why? Probably because the Fed minutes released on November 24 revealed a completely different Chairman Powell than the one we all saw in the FOMC presser on November 3. It was as if Dr. Jekyll had turned into Mr. Hyde.

After a wonderful Thanksgiving weekend, the mood turned rosier. Treasury yields went up 3-4 bps and Dow was up 237 with NDX up 374 points. Then came Tuesday & Wednesday with Fed Chair Powell speaking to the Congress with Secretary Yellen. The dam broke then:

- Dow fell 653 points on Tuesday & 462 points on Wednesday. S&P fell by 88 points & 54 points. The NDX fell by 263 points on Tuesday and by 258 points on Wednesday. Treasury yields across the curve fell hard on both days with the 30-yr falling by 12 bps and the 3-yr rising by 3.5 bps & 2-yr rising by 8 bps, ( further contracting the curve).

Fortunately Thursday was a relief day for stocks with the Dow up 618 points & the NDX up 113 points. But the Treasury curve still contracted further with 30-3 yr & 30-2 yr contracting by 8 bps. Some argued that the sell off in NDX & stocks in general had reached oversold levels.

Then came Friday & the NFP report and Treasury & NDX melted down further.

We went through this painful rehash to demonstrate that it is the Jekyll-to-Hyde transformation of Chair Powell that is absolutely & singularly responsible for the two-week long turmoil in all financial markets.

But which apparition is he imitating now? A really smart guru says it is the Fire version or the Q4 2018 Powell.

“think about this – 3 rate hikes next year plus a full taper plus at least 1 trillion dollars of fiscal drag – add it all up & its a colossal fiscal & monetary hit to the economy … asset prices are so high that they probably can’t take it; they are probably going down 20-30% into the Fed meeting or until January. until the Fed backs away.. “

But in that 2018 Fire version of Hyde-Powell, Treasury yields kept shooting high & didn’t stop until Powell reversed. The reverse is happening today. Treasury yields are melting down leading us to wonder whether this is the Ice version of Hyde-Powell, a la 2007-2008. Look how the banks got torpedoed this week & how commodities got discarded across the board. Also credit underperformed Treasuries.

This seems like Ice to us, not Fire. And that is a big problem, not merely for Hyde-Powell or Biden but to all of us, the American people!

4. Stocks

Frankly & despite the above, Friday afternoon did seem somewhat panicky to us. We did wonder whether the Docusign decimation plus the meltdown in Treasuries was because of some kind of liquidation of a fund or a group of over-allocated longs. A tiny sign of that was that unpopular IBM & Cisco closed up on Friday.

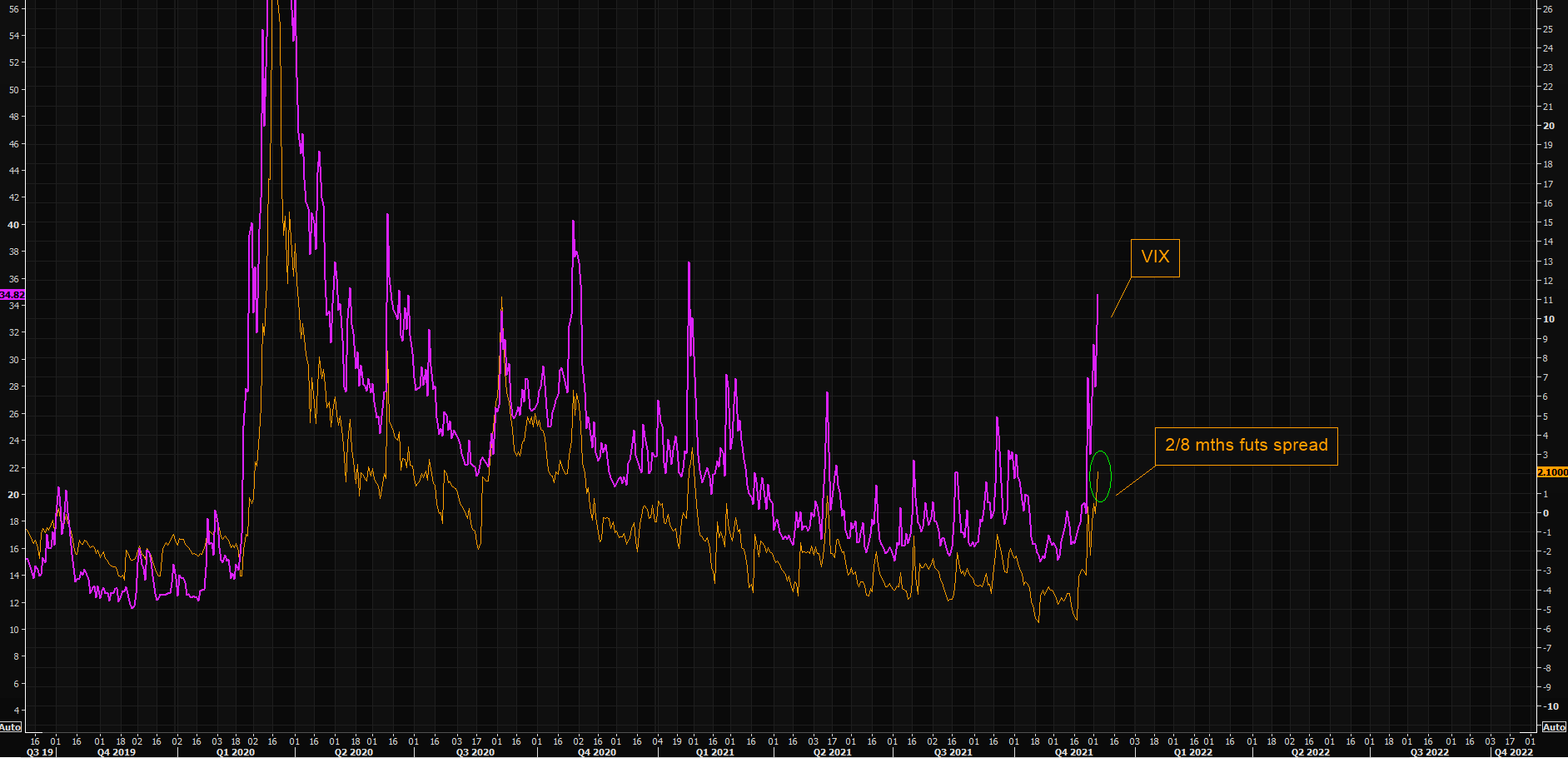

When in doubt, we look at the VIX or to smart people who write about VIX:

- The Market Ear – VIX term structure – extreme edition – From shifting quickly lower yesterday, the entire structure is shifting sharply higher today. The stress in the short end of the curve is now extreme. Picking up dimes in front of the steam roller strategy has resulted in a lot of p/l pain since last Friday. This is big panic being priced in…especially as we are 25 handles above yesterday lows…

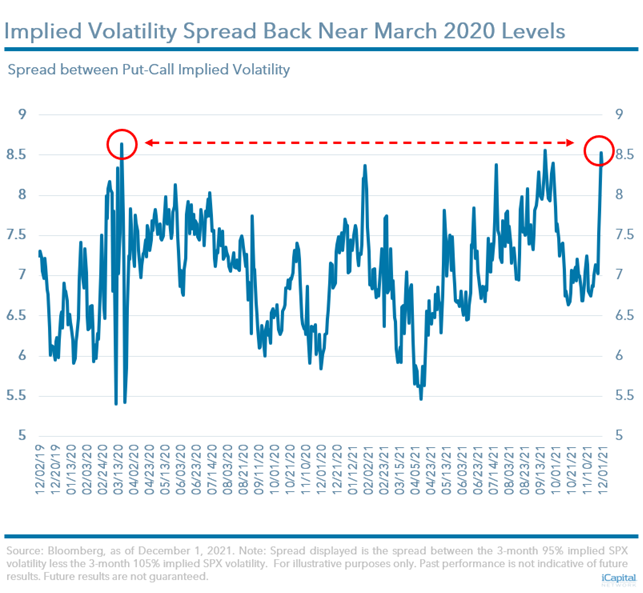

What about “put” volatility vs. “call” volatility?

But what about VIX futures?

- The Market Ear – How is “under the hood” VIX stress doing? – It is very stressed. VIX 2/8 futs month spread is trading at levels we last saw during the “crash” in late January. The entire term structure is very extreme here as people are grabbing short term protection.

Given the above, would you have expected the below?

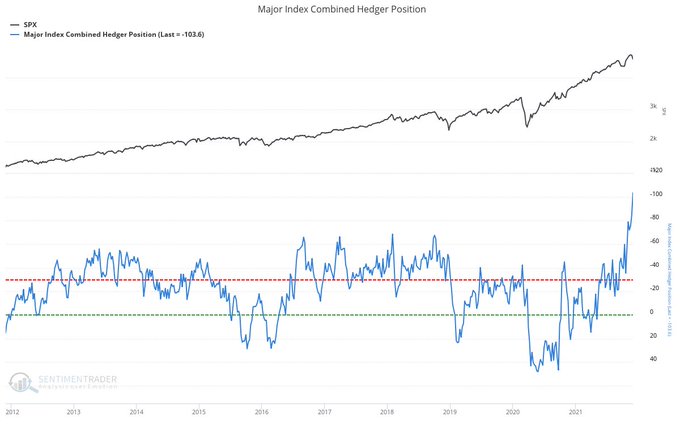

- SentimenTrader@sentimentrader – All aboard a derailed train. This week, speculators in major equity index futures bought aggressively, moving to a net long position of over $100 billion. That’s nearly twice as large as any other position extreme, in either direction, ever.

What’s going on? More importantly, what will happen next? Will VIX fall or will the longs sell? Guess we will find out next week.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter