Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Buy in May & Come in?

This has been a topsy-turvy year. Whether you mean “upside down” or “chaotic” by that term, this year has been that. The proven wisdom over the years of 60-40 stock-bond allocation was shown to be dangerous. Seasonality patterns were torn apart. And, as this week showed, the “Sell in May & Go Away” dictum may need to be turned upside down to “Buy in May & Come In”.

Smart people have been coming on Fin TV and calling for a sharp & strong rally for the couple of weeks. Finally the stars got aligned and we got a rip-roaring rally this week, more specifically during the last 3 days of this past week.

The old 60-40 saved many during the two weeks before last – Dow, S&P & NDX down 2.1-2.8% & TLT up 2.5% in the week ending May 13 and Dow, S&P, NDX down 2.9%-3.2% with TLT up 2.1% the week ending May 20.

The balance was restored this week with,

- Dow up 6.2%, S&P up 6.6%, NDX up 7.1%, RUT up 6.5%, DJT up 7.1% with TLT only up 35 bps. And VIX fell 12.4%. And amazingly, HYG & JNK, high yield credit ETFs, rose by 4.9% on the week.

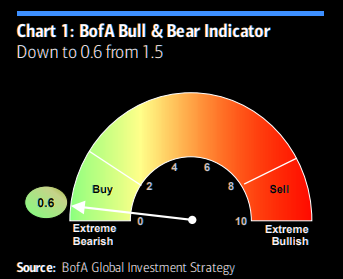

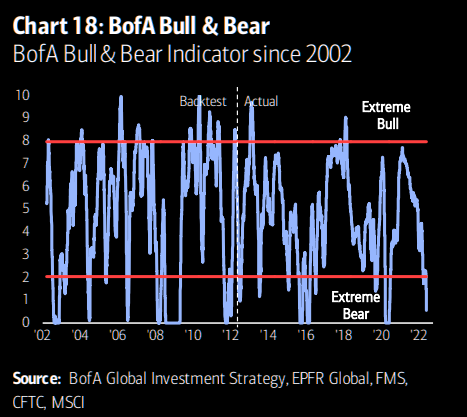

And the “most accurate contrarian buy signal”, as it was dubbed last week, is even more bullish now:

- The Market Ear – The king of contrarian sentiment signals in even deeper buy territory – BofA’s contrarian bull/bear sentiment indicator was signalling buy last Friday already. Back then most were in fear. The signal is now even stronger. Maybe the crowd starts chasing SPX here. After all, it is up 8% since last Friday...

But signals don’t create rallies by themselves. Actual buying does. Last week the talk was about sizable month-end buying from investment banks. That should exhaust itself by Tuesday May 31. Is there another source of buying or forced buying which is buying of the most painful kind?

- The Market Ear – Could momentum chasers fuel a further squeeze in equities? CTAs have been selling equities aggressively and are still running rather big shorts. Their p/l YTD is impressive. Will they reduce those shorts quickly should this squeeze further?

What is another source of buying, now that earnings are out & corporate windows have opened?

- The Market Ear on Monday May 23 – The corporate put in the money: buybacks 3-4x higher – “we see record buyback announcements YTD with estimated 3-4x higher than average executions in recent weeks. S&P 500 companies have announced $429B of buybacks YTD (stronger pace than 2019 and 2021) as companies continue to generate strong cash flow on healthy margins. In the latest sell-off, JPM estimates 3-4x higher buyback executions than trend, which implies the corporate put remains active. Based on 1Q results, buybacks were up 45% y/y and 3% q/q, led by Tech ($62B in 1Q22), Financials ($49B) and Healthcare ($39B)” (Kolanovic)

But all the above is secondary. Just a quick glance at this past week shows the primary & dominant trigger in the market:

Notice that the stock indices were virtually flat on the week until the Fed minutes were released at 2 pm on Wednesday. And then, Voila!

2. “Thank you Jay”& now a Yield FOMO?

“Thank you Jay, if we may fondly call him so” was what we wrote on May 8. We thought his performance was superb in his presser on Wednesday, May 4. We had added then – “Our point is that Jay Powell was being sensible in saying that the Fed was not considering a 75 bps increase in the next FOMC.”

Unfortunately for him, the next day was a disaster of sorts because of the unholy combo of falling productivity & steeper inflation. And the Treasury market puked on Thursday & Friday – 30-year Treasury yield rose by 18 bps, 20-y yield rose by 20 bps, 10-yr up by 18 bps, 7-yr up 17 bps & 5-yr up 15 bps. And VIX jumped up to 35 on Friday morning.

That was bad luck for him but good news for Treasury investors because that was the local peak in Treasury yields. David Tepper closed his Bond short, as he told CNBC on following Monday morning. And Treasury yields have now fallen for 3 straight weeks since Friday May 6. And TLT is up 5% since that Friday.

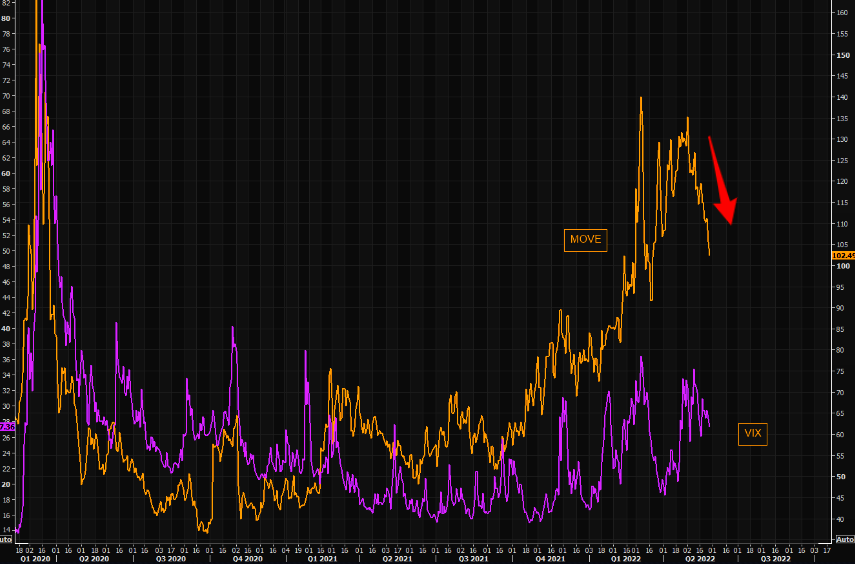

And look what Bond volatility has done:

- The Market Ear on Thu May 26 – The puke in bond volatility – Bond volatility, MOVE index, continues “crashing“. This is the biggest consecutive move lower (deducting the wild moves in March) in MOVE since Corona hit the world. Note how “sticky” VIX has been in comparison.

In accordance with Jay’s updated FOMC minutes that followed, Bostic went softish on Monday. And then we saw Frances Donald of ManuLife speak of a Fed “pivot” in September to CNBC’s Kelly Evans on Tuesday:

- “.. 3-6 months from now they are going to have plenty of data across a range of indicators from inflation expectations to actual inflation to a breadth of global & domestic data that will give them cover for a pivot … to me September is looking like a pause … “

Two days later, Priya Misra of TD Securities spoke of a 3rd regime in interest rates this year (1st being short rates going up, 2nd being long rates going up) on BTV Surveillance:

- ” … now the rates market is starting to price in growth concerns which is why the curve has steepened, interest rates have fallen followed by the front-end … I think people are seeing the tightening in financial conditions; … now the market is saying the Fed is overdoing it & they might not be able to hike much above neutral; that’s why cross-asset correlations have come back & they are here to stay … growth concerns are front & center … what happens (after the next two 50 bps hikes)? that’s the big focus … “

Ms. Misra was calm & unruffled as she spoke about tightening in financial conditions on Thursday morning. In stark contrast, Prof. Jeremy Siegel was anything but calm as he spoke with CNBC’s Scott Wapner on Tuesday after the close about what he saw – “the 2nd largest monthly decline in the money supply in more than 60 years” and said “the Fed is withdrawing liquidity perhaps a bit too quickly“. Watch this clip. It is important but also humorous with Wapner’s stunned consternation at Siegel’s pivot:

Then came Ian Lyngen of BMO on Thursday morning on BTV Surveillance (minute 50:50):

- “… we have a pretty significant 7-year auction this afternoon that we are expecting will provide a good barometer of the willingness of investors to underwrite the deficit… the recession commentary that is making the rounds is really defining the conversation of overall rates; 10-yr yield peaked at 3.20%, now down to 2.75%; the 2-10 curve us at 25 bps; …”

By the way, the 7-year auction was just white hot. Santelli couldn’t believe that only 6% of the auction was left for the Dealers to buy. Does that justify the “Yield FOMO” term Ian Lyngen used on Thursday morning?

Ian Lyngen also answered the “where are the buyers” question Dominic Konstam had asked on Friday May 7 on BTV Surveillance:

- “over the course of last 2 weeks are early indications that Japan is coming in back into the (Treasury) market .. will continue over the course of the next several weeks …. there is this sense of Yield FOMO as it were looking back at 3.2% in 10bps; .. will become defining as the summer plays out … if Powell overshoots, then are going to see a material slowdown … that’s why we are not at 3.50% in 10s but closer to 2.50%”.

The Yield FOMO fear also engulfed high yield credit:

3. Knapp vs. Krinsky?

Frankly, we don’t get Scott Wapner, the host of CNBC Half Time & Over Time. The key to excellent Fin TV are guests, smart guests, who add value and Wapner has delivered that probably more than any one else. But he seems to go overboard at times like when he abused JPM’s Dubravko when Dubravko was right & Wapner didn’t understand his point. And since then, he has been petty in not bringing back Dubravko on his show.

Now this week, Wapner went the other way in praising Barry Knapp, a frequent guest on CNBC. Knapp is smart & often makes good points. But Wapner went overboard for some reason calling this week’s rally as “the Knapp Rally”. How nuts is that? Many smart guests spoke of a rally given the abysmally oversold conditions. So did Knapp last week in a “I am beginning to buy” kind of a way on CNBC Squawk Box.

Actually the two smart points he made were DELETED from the clip posted by CNBC Squawk Box as they often seem to do. Those points were what we featured last week – that Tech was valued similarly to Staples & so Knapp would take techs over staples any day at the same multiple & his call on buying Semiconductors which worked out well this week.

With that, we confess wondering whether Knapp had the gumption to complain to CNBC Squawk Box about deleting his smart actionable points from the posted clip of his remarks. Probably not would be our guess. Because guests probably don’t get re-invited if they complain about actions of CNBC shows.

With all that, we do highlight what Knapp said this week to Wapner. It is a different & more meaningful reason than the ones expounded by many rally proponents:

- Fed policy normalization corrections are really the second best window to put money to work if you didn’t buy the lows of the recessions; end of QE2 in 2011; end of QE 1 in 2010; drawdowns of fears that the Fed is tightening into slowdowns are generally way over done particularly early in the business cycle; these are great entry points; … at this level you have to have a deep recession (median declines for a recession is 24%) ; we would have to have a deep recession to justify downside particularly in cyclical sectors; I think this is the start of the recovery from Fed policy normalization correction; …. I do think that the bottom was in …. I also think that the global financial crisis was a negative productivity shock while this was a positive productivity shock; That’s part of the reason why margins have held up as well as they have; .. I think the productivity part of the story is going to be evident in the second half of this year; & ultimately the Fed can raise rates farther than expected; .. but the real limiting factor on how far they can go is Federal Government Debt not private sector debt; … That’s a very different dynamic and it implies we are not close to the end of the cycle….

If Knapp proves right about his productivity thesis & margins holding up throughout the second half of 2022, then this may well end up being the bottom of the stock market for this cycle.

The contra example was provided by Jonathan Krinsky on May 25 (before the 2 pm Fed minutes release that sparked the huge rally) who had called the steep correction we have seen in the past few weeks:

- Short term market call is very difficult here … you can make the case for a counter trend rally; in our view that is a small part of the equation & we still see a significant move lower ultimately for the S&P and the Nasdaq; …. you can get a 3-4-5 day rally but its not changing the primary trend of the market though; … 4,000 was a logical place to pause; … where we get to 3400, 3500 is really a culmination of a couple of things; even two months is reasonable perhaps [for this rally to last] … from October 2007 into July of 2008, the S&P was down about 20% just as we are now; …. then we had a 2-month reprieve , a 2-month bounce from July & August of 2008 … what’s remarkable in August 2008 is that VIX was below 20, a month before Lehman Brothers … it just goes to show that once markets exhaust themselves in one direction, it doesn’t mean you have to reverse & go into other direction; I would be surprised if we go straight down to 3,400 – 3,500 ; but if we go up to 4,100 – 4,200 it doesn’t mean it changes the primary trajectory

We certainly don’t have a clue but, in our simple view, what the Fed does with QT will end up being far more important to markets than what they do with interest rates. If they stay on the QT road while the global economy keeps slowing down, then we might get a different market reaction than what we might see if they postpone QT or make it much more gentle as the economy slows.

4. Oil, Emerging Markets

Those who like feeling a shiver down their spine might enjoy the clip of JPM’s Christyan Malek on BTV Surveillance on Friday (at minute 2:05:00). His upside target on oil is $150 in second half 2022 & he says gas prices across the U.S. will hit $6 in 2H22. He points out that “we have never been below 5% of global spare capacity in the world; that equates to a much bigger premium for oil than what you would expect it to be“.

He made an interesting case about emerging markets saying

- “what we discovered is resilience of emerging markets to higher prices; their bar is much lower because its about living; do we buy oil at $150 or do we suffer consequences – hunger, riots, revolutions?”

But what about emerging market countries who hardly have the currency needed to buy oil? Malek did not address this but we all might have to especially when a particular emerging market state has the 4th or 5th largest nuclear weapons arsenal in the world; a state that has only $10.2 billion in reserves but a $90.12 billion in debt; a state that unsuccessfully tried to persuade the IMF last week (in a meeting in Doha) to provide a loan of $3 billion dollars. And a state that is now in the midst of a political civil war?

They could have done it more smoothly but how smart was the Biden Administration to get out of Afghanistan & the need to suck up to Na-Pakistan for the overland & air routes to Afghanistan!

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter