Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.If that doesn’t stop it … ,

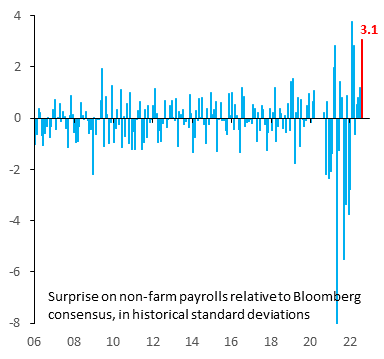

The term “that” refers to the huge surprise of the Non Farm Payroll number coming in at 528,000 more than 2X the estimate of 250,000 jobs. Treasury yields exploded up &

- Jason@3PeaksTrading – – TICK opens with extreme washout print at -1560 right into 8 EMA on $SPY

It certainly looked like a bad omen for the rest of the day. Then,

- Cousin_Vinny@Couzin_Vinny – – $SPX $SPY trading room was long 415P out at the open – hard to short this flow.

And a bit later,

- Jason@3PeaksTrading – – $SPY flying into a gap fill now after that TICK washout, silly gap down today

Look at Friday in a glance:

If the shock of the super-strong NFP and the explosive rally in 2-3 year Treasury yields was not enough the take stocks down even for a day, what gives? Especially in the cacophony of the Fin TV elites!

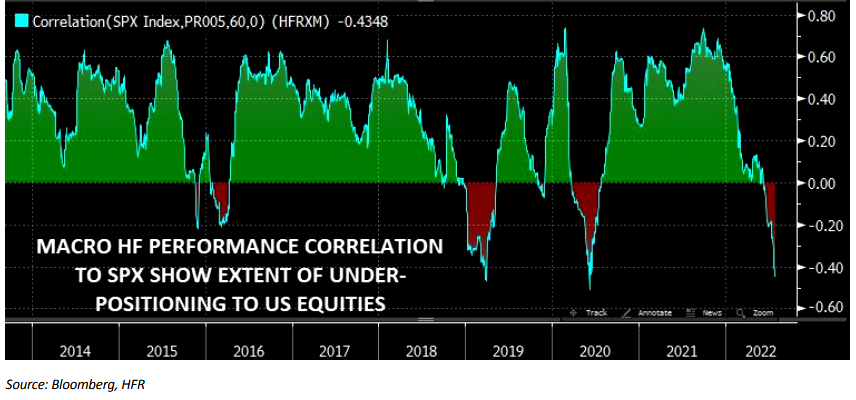

A simple answer could be large investors are still positioned wrong:

- Via The Market Ear – Thursday, April 4 – “Boss…I have no US equities” – In case you still wonder why things have squeezed hard. Hedgies are very “under positioned” to US equities.

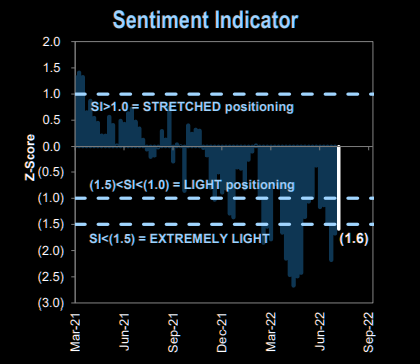

What about sentiment, you ask?

- Via The Market Ear – Saturday – Bears beware – Goldman’s sentiment indicator is still at “extreme” levels.

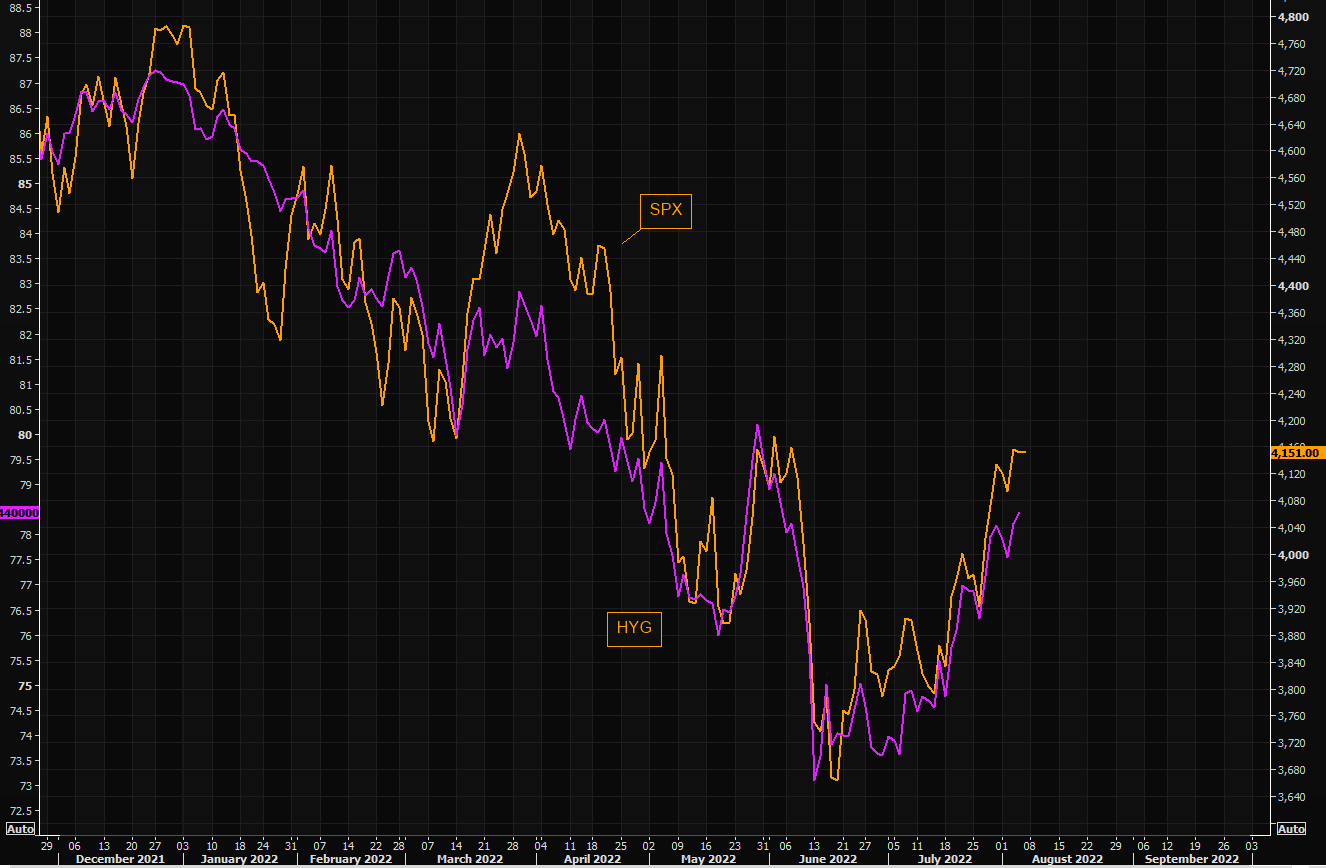

That could explain S&P’s refusal to stay down on Friday. Credit, in the past, has been the canary in the coal mine for stocks. Perhaps Climate Change folks have cleaned out all the coal mines or perhaps canaries have been rescued & placed in bird sanctuaries. OR credit is actually shouting Let’s Go a la TB12!

- Via The Market Ear – Friday – The bull in credit – HYG continues following the SPX higher. We have not seen such a bull in HYG in a long time. Second chart shows this space has seen a lot of inflow “love” recently.

Even those who said the S&P will fall to 5% after stalling out this week actually say the S&P will rebound to 4,350 even 4,400 by mid-late September:

Isn’t this bullish for those large “hedgies” who are still positioned light in U.S. equities? Heck, even a worthy guy who thinks stocks have made a double-top like the last rally & could fall apart, thinks the S&P could rally to 4,300:

So if no one can think why the stock market should take a trip down, then perversely it might just do that, right? Especially if the $VIX finally pukes below 20!

But wait, what about TLT? Surely it got butchered on Friday, right?

2.Pivot-Inflation

We actually wondered on Friday whether Powell has turned into Trump or a Trump-lookalike for the elite Fin TV crowd. We kept hearing how Powell had actually pivoted into an easing Fed-chair and how wrong he was to do so. But when we went back & checked what he had said, we could not sign of a pivot or even a hint of it. All we found was a posture of being dependent on incoming economic data.

There is little doubt that Friday’s NFP report put back a 75 bps hike into September’s FOMC. Just look what the belly of the Treasury curve did this week:

- 2-year yield up 36 bps; 3-yr up 37 bps; 5-yr up 28 bps; 7-yr up 22 bps; 10-yr up up 17 bps

In contrast, the rally inflation-sensitive Treasury maturities actually yawned this week, relatively speaking:

- 30-yr yield up 4 bps; 20-yr up 5 bps with TLT down 80 bps on the week

What gives? Did the 2X beat of jobs added actually hide something not so good? Listen to Stephanie Pomboy of MacroMavens & Larry McDonald of Bear Traps Report explain that to Maria Bartiromo on Fox Business. Pomboy said flatly that “profits are going into outright recession” and McDonald quoted CEO of Uber to point out that “at the end of a cycle, people scramble for jobs“. Watch this clip:

Another question is whether the Fed & investors should depend too much on a single point of data that is 3-standard deviations larger:

- Robin Brooks@RobinBrooksIIF – – The Fed should NOT hike 75 bps in September because of yesterday’s strong payrolls. The recovery from COVID is very noisy, which you can see from how much payrolls data surprises have grown relative to history. We need to urgently stop making policy decisions based on noisy data.

Getting back to Stephanie Pomboy, Mike Wilson of Morgan Stanley must be happy to find that she is even more negative than he is about profits. He gave his cure 3 days prior on BTV Surveillance saying (min 1:34 – 1:39):

- “ … we have been bullish on bonds … we think the bond rally makes perfect sense; it is in context with our fire and ice narrative; we are staying long the long bonds & we think it is a great hedge against the equity portfolio right now …”

Ok, but what is a fair value for the 10-year yield now?

Remember the time when long Treasury Bonds bigly saved investors!

- The Market Ear – Friday – 2008 déjà vu still in place? – That nagging feeling is still with us, although we are “actively” waiting for the volatility puke in order to explore long volatility set ups. SPX futs now vs 2008 in % terms.

That is surely nuts, right? Of course with Russians & Ukrainians fighting near a Nuclear Power plant in Ukraine, with China sending squadrons of fighters into Taiwanese air & almost blockading Taiwan with naval ships, with Israel-Gaza in war mode, with Armenia-Azerbaijan fighting again in Nagorna-Karabach & with Serbia-Kosovo about to begin fighting, the present is not as placid as it seems.

If that was not enough,

- Jeff M. Smith@Cold_Peace_ – – Good. India-US joint army exercise Yudh Abhyas will be held in the Himalayas in October, 60 miles from the China-India border in Uttarakhand. Training together at 10,000 feet to increase interoperability for high-altitude warfare. https://theprint.in/defence/india-us-to-hold-high-altitude-military-exercise-near-lac-amid-rising-tensions-with-china/1067250/

- “This time it is a very important exercise because the Indian side will be showcasing their high-altitude warfare strategies, while the Americans will be showcasing a number of technologies that can be used in such scenarios. This exercise has been planned in such a way that both sides come together for any scenario,” a source said.

- Another source said that various activities have been planned for both sides to fully exploit the two weeks of focused high altitude military exercise and to see how the troops can operate together.

3. It doesn’t glitter but is it … ?

Look what the DXY, the U.S. Dollar ETF, did on Friday:

That should put the kabash on Gold, right? Strange as it might sound, 3 different gurus came out with a positive view on Gold going forward. The most detailed and most decisive was Larry Williams, who said via Jim Cramer, that “it should be ready to rally here“. The W.C. clip below gives 3 different reasons that suggest a rally in Gold. Watch it:

Next came Tom McClellan on August 4 in his article – Gold ETFs Being Shunned During Price Upturn:

- “We have seen this happen before, when gold prices would turn higher but the total combined assets in GLD and IAU would refuse to turn upward along with prices. In those cases, what usually would happen was a longer up move in gold prices, an upturn which lasted until “the crowd” finally decided to get on board. The longer that they hold off from buying into these ETFs, the longer that the uptrend can last. “

Finally on Friday, Carter Worth of CNBC Options Action:

A lookback on the gold miners!@CarterBWorth says it may be time for a reversal $GDX@Michael_Khouw explains the relation between energy and the miners. pic.twitter.com/py5WBFCNzk

— Options Action (@OptionsAction) August 5, 2022

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter