Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.What’s going on?

Look what the U.S. Dollar did during the past 3 days:

This is the mighty Dollar, the reserve currency of the world. And its moving like a stock – down 92 bps post Powell presser on Wednesday; up 50 bps on Thursday and up 1.20% on Friday post strong NFP.

The real question is whether Fed Chair Powell knew what the Non Farm Payroll number was going to be 42 hours before 8:30 am on Friday. Based on his presser, our guess is he did not have an inkling. If so, that is really scary to us. If the Fed Chair, assisted by several hundred PhDs & multiple committee members with their own advisors, was so clueless, then aren’t we in trouble or aren’t we all doomed to drive monetary policy looking backward?

On a weekly basis, this week confirmed the trend we have been seeing lately – Treasury rates going more up than down; Dollar going up & Gold, Silver, Copper going down. In other words, a small but steady reversal of the 3 big trends that enabled the big S&P rally in 2023.

Will this reversal stick? At least until the next NFP report? We have no clue and it seems every one has opinions but no clue.

So we will stick to describing a clip in which two very bright, successful investment women express sadness filled resignation at the hot growth rally they were seeing on Thursday morning. It was kinda funny to see the resignation in their voices while the tech stocks were celebrating. Look at the facial expressions & tone of BTV’s Lisa Abramowicz and the sad, semi-hapless look & tone of Wei Li, BlackRock’s Head of Macro Strategy, as Lisa asked the following question at about 1:55 of the Thursday Morning Surveillance clip below:

- LA- “what’s your conviction level to lean heavily against the tech rally, to sell everything, cash out & just hide out in cash until you start to see that downfall?“

Seriously, look at LA’s face & notice the frustration built up in her face & gestures. In contrast, Wei Li looked merely resigned & unsmiling as techs rallied ferociously on Thursday morning:

- Li- “I think this is the time to stay invested; … right now we don’t want to chase this tech rally because of the incredible momentum you yourself described; …. so staying invested is important … “

In response to LA’s question about Powell’s posture,

- Li – “he was not consistent … markets are reading into it what it wants to read into it which is to jump & chase this rally …”

That may be why Wei Lie used the term “markets are pricing Take Off from here“. Watch the clip below & notice how the usually loquacious Tom Keene & Jon Ferro kept mum as the two women went into their resigned-upset discussion.

After that, we think it might be appropriate to include a tweet that might please Ms. Abramowicz.

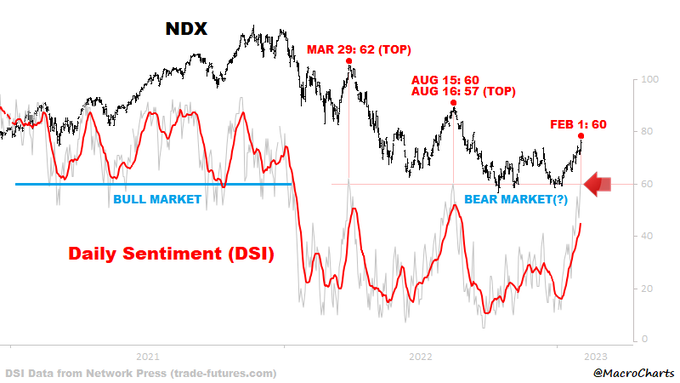

- Macro Charts@MacroCharts – Feb 2 – “Sentiment like this didn’t last long in Bear Markets. My Core Models are near Top levels. • Trash Stocks are rallying identical to last August. • Bulls are taking victory laps. • Bears are openly ridiculed. Human nature never changes – if/when this turns down, look out“.

Since neither we nor most have a clue, why not simply summarize the weird action this week?

US stock indices – Dow down 15 bps; SPX up 1.6%; RSP up 1.4%; NDX up 3.3%; RUT up 3.9%; IWC up 4%; DJT up 7.1%; SMH up 4%;

Dollar up 1%; VIX down 72 bps; Gold down 2.6%; GDX down 6.1%; Silver down 5.4%; Oil down 7.8%; Brent down 7.7%; OIH down 7.2%; XLE down 6%; FCX down 4.4%

International stocks – EEM down 3.4%; EWZ down 4.5%; EWY down 3%; EWG up 1.8%; INDA down 1.7%; FXI down 6.4%; KWEB down 7%

Treasury yields – 1-yr up 11 bps; 2-yr up 9 bps; 3-yr up 5.5%; 5-yr up 4 bps; 7-yr up 2 bps; 10-yr up 0.8 bps; 20-yr down 0.4 bps; 30-yr down 1.2 bps; EDV up 94 bps; ZROZ up 93 bps;

2. Adani Washout

The sensational news in Asian markets was the washout in the market cap of Adani Enterprises, the company mainly owned & run by Mr. Gautam Adani, the richest man in the world until recently. Reportedly, this washout was courtesy of a very negative research report from renowned short seller Hindenburg Research which said they had also taken a short position.

It was certainly a big markets story but not necessarily of major relevance to US markets. So CNBC sensibly seemed to take this in stride while Bloomberg.Com thought it was the biggest story in the world & devoted a majority of one-sided coverage to this, at least in their Asian coverage.

Besides what was known courtesy of Hindenburg, a large portion of mud was heaped, especially by Bloomberg.com, on India’s market regulations & what this washout might mean to Indian markets.

Our own view is that markets are smarter & figure out things better especially on an index level. So the chart below of INDA vs SPY seems to suggest that, the impact of the Adani washout on the Indian market is not material, at least not as of now. That impact is the crossover in the last 10 days in the chart below.

Frankly, the RSI & William %R levels seem to suggest a long flyer into INDA or Long INDA & Short SPY trade, at least to simple minds like ours.

We wonder if Andrew Ross Sorkin, the intellectual luminary of CNBC, would concur at least after looking at the chart below. Unlikely because a BrIndian Brahmin is always convinced that his/her intelligence is superior to market wisdom of plebians.

If you disagree with us, watch the clip below to see how Mr. Sorkin, a protege of NYT’s Tom Friedman, tries so hard to get Marko Papic, chief strategist at Clocktower group, to express negative opinion of India & Indian market regulations. The topic is serious but watching Sorkin’s desperation was really funny to us.

But we just can’t get upset with Mr. Sorkin or his petty pursuit above. After all he is so representative of BrIndian Brahmins that we know & grew up with. Their modus operandi is – forget the big story, the big picture & try so hard to make a petty intellectual point. No wonder we feel Mr. Sorkin has to have some BrIndian Brahmin ancestry in him!

* A note for CNBC’s Kelly Evans. She should learn from Sorkin how to use smart experts in topics like this instead of clueless, uneducated staffers. Having them on her show on topics such as these just makes her look laughable or worse. Wish she had used the Fred Kempe & John Kilduff model she used to discuss natural gas & China

What really eludes us is how both Bloomberg.com, Bloomberg TV & CNBC missed discussing a simple comparison of the world’s two richest men & the washout in their stocks in the last two months – Elon Musk & Tesla in December-January with Gautam Adani & his stock in January-February:

Any one interested in some detail about the big but uncovered event of last week re Adani as well as a more detailed discussion of the Adani washout should read our adjacent article Adani Washout – Our Reflections.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter