Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we clude important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.“US is probably the place to be“

This week may not have proved that but it did demonstrate that US is better than the “not as good as rest of the world” place to which many have relegated it this year. This week the S&P hit its high point for 2023 and it was driven by President Biden’s speech on Wednesday. Look what happened after that “good news”:

A number of smart guys murmured about “overbought”, the most explicit among them being:

- Jason@3PeaksTrading – May 19 – They gonna try to pin this $SPX at 4200 but looking for that Monday weakness overall to follow through lower, could see 4100 just as quick next week once all this gamma fuel expires

What happens to the Debt Ceiling talks might determine the next couple of weeks but it is hard to see a real default happening. What really happened this week is that S&P & TLT (or Treasuries in general) diverged starkly after Biden’s speech.

- Dow up 38 bps; SPX up 1.6%; NDX up 3.5%; RUT up 1.9%; DJT up 92 bps; EEM up 1.2%; EWG up 1.7%; VIX down 1.3%; TLT down 2.9%; EDV down 3.7%; ZROZ down 3.5%; US Dollar up 50 bps;

Once again, a banking crisis prompted a loosening of liquidity measures that are reflected in the SPY – TLT divergence. Anneka Treon of Van Lanschot Kempen said on Friday early Bloomberg (minute 1:15:08) – “the reason why credit spreads have narrowed, the reason that VIX is rather moderate in because liquidity has been quite strong“. She then amplified by saying:

- “we were entering into a new era of QE going into QT into tightening & then you see 3 major Central Banks in the World actually halting their QT programs because of issues that have popped up; this addiction to liquidity is really hard to get rid off – BoE – Gilts crisis; Fed – banking crisis; BoJ – yield curve control”

You see the effects on the S&P vs. TLT chart for 2023, specifically the big divergence since mid-March as Fed’s measures to increase bank liquidity took effect:

Another effect of the Fed’s liquidity was to put a damper on the widely circulated “US is over-invest ex-US” opinions. At this point, it might be instructive to recall what Barbara Reinhard of Voya Investments had said on BTV Surveillance back on April 4:

- “what we saw in March is an important shift .. US outperformed rest of the world pretty strongly; …. we think 700 bps of the international markets outperformance over the US is largely behind us & we think it is the US that is going to be the leader going forward; .. the slowing inflation scenario that we have in the US gives the US Central Bank the opportunity to slow their rate hikes, possibly pause and that means the US is likely to be be one of the first ones to pause … remember that at the first rate pause there is usually a very big countertrend rally in equities”

This past Thursday she was back on BTV Surveillance (minutes 55:26 to 1:03:40) with a follow up beginning with a gentle “the US has some really good qualities” statement:

- “inflation in US has peaked; its going in the right direction; … if you think US has an inflation problem, Europe has a much bigger one & a stickier one and their central bank is much further behind the curve than the US is; so US is likely to outpace the world“

- “the visibility you have on the US is quite good; US Consumer is holding in there quite well in the face of jobs openings coming down; .. so the US just has more strength to it and, at the margin it is a relatively good thing”

- “you have had narrow leadership across the entire globe; what has been doing very well for the past 5 months is US Tech & European & Luxury goods… note if the US economy turns out to be too strong or if inflation data starts to break higher that’s right in the face of how we are positioned …. but we think at least for the next couple of months, its gonna go our way “

- “we are top down global macro .. we think the US is probably the strongest place to be in; … the only other place we may think about are parts of Japan; looks like it is so cheap & good from currency perspective but for us the US is probably the place to be“

Now a couple of tweets that tend to support the above:

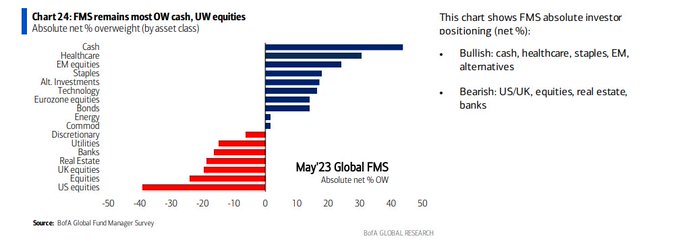

- Larry Tentarelli, Blue Chip Daily@LMT978 – May 20 – CTA’s moved to net long equities over a week ago. As prices move higher, they buy more, which starts to build on itself. Shorts cover, new longs come in & that’s how trends build. Fund managers max OW cash/UW equities + bearish individual investor sentiment at multi-year highs.

An interesting historical signpost below:

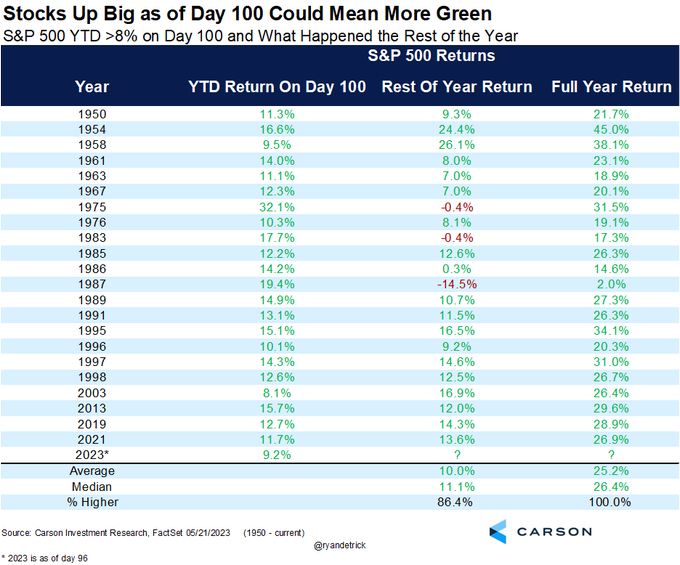

- Ryan Detrick, CMT@RyanDetrick – May 20 – This Thursday is the 100th trading day of the year. When the SPX was up >8% on this day (like ’23 could be), the rest of the year was up 10% on avg and higher 86% of the time. Also, the full year has never been lower. Anyone up for another 10% from here?

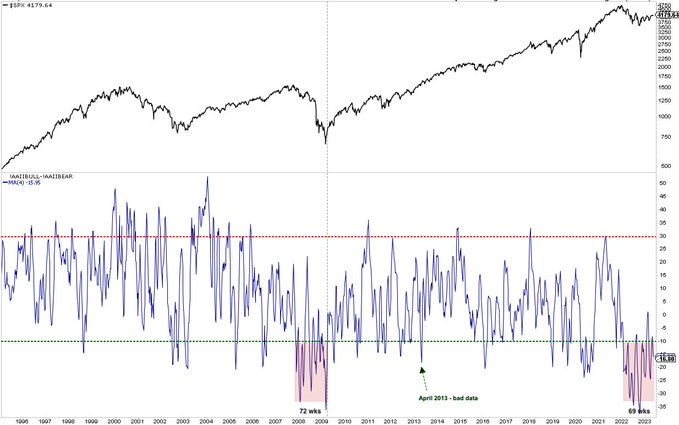

Now a comparison between the bearishness we saw before March 2009 & the bearishness now:

- Urban Carmel@ukarlewitz – May 18 – In 3 wks, the persistence of bearishness will eclipse the period that ended in March 2009. And it’s not just AAII: BAML, JPM, Barron’s and fund flows all saying the same thing

Does this suggest that we could see a rally from ending the current bearishness even somewhat like the rally we saw after March 2009? Holy whatever!!!

2. Thanks & looking forward

In our Investment TACs article dated April 30, 2023, (Section 2. Semiconductors) we had highlighted 3 opinions suggesting Semiconductors might outperform the S&P if the parallels hold. How accurate was the bullish message of those tweets? Yes, most of the outperformance came this past week but an outperformance of nearly 8% in 3 weeks is pretty good.

This is an example why we believe reading & listening to smart opinions is the easiest way to at least hang in there in this fantastic but often disheartening game. With this confidence, we highlight below two “off-the-charts” opinions from those who have been right in the past.

First is Jessica Inskip whose views were featured by Jim Cramer on Monday, May 15. Once again, the Mad Money clip of this helpful conversation is somewhere in another galaxy or in a secret place we can’t access. So below are our quick scribbles & our recollections of what we heard. If you want to do something with the below, please double check with Ms. Inskip or Jim Cramer:

- “.. megacap stocks leading the way; NDX is very very strong … now above 13210 & its now support; next hurdle 13720 …. there is lot to like here ; bullish trading cycle …. upward slope of moving averages; … MACD getting real close to bullish cross-over …. getting very close to MACD givng a buy signal. … S&P still trying to break out …. resistanece at 4195 …. going sideways but making higher lows … S&P decent but not as good as NDX ;; S&P can rally just fine without breadth ….”

Then on Thursday, Cramer relayed comments of the legendary Larry Williams including views on Tesla. Now we did find the clip below on YouTube. The charts of Mr. Williams need to be looked at with the commentary. A key point that we scribbled – “Long term up cycle pretty bullish & intermediate term cycle (in blue) up till mid-July“. Watch the entire clip is our suggestion:

Despite everything above, we do see that the stock market, especially big-cap techs, may be overbought here. So we feature below the clip of veteran technician Mark Newton. Besides arguing that large-cap tech is getting closer to stalling out, he says that Oil stocks may be set for a bounce:

3. The other side of the pair trade

Recall the comment above of Barbara Reinhard of Voya that “at least for the next couple of months, its gonna go our way”. That allows us to mention our own bugaboo or the fear that keeps us from getting all bulled up.

We begin with the year-to-date chart of SPY vs. TLT:

Normally QQQ & the TLT are somewhat aligned because as long maturity rates go down, the market PEs of big cap tech stocks rise. The inverse was true in 2022 with QQQ falling hard & TLT falling hard as well.

So the above feels weird or entirely 1999-like. That possibility should not be ignored as many, including us, did wonder whether the Yellen+Fed injection of liquidity in March would lead to what the liquidity injection in October-November 1998 led to – 1999 tech bubble.

But that is not our gnawing fear. Our fear is what is shown in the 2007 chart below:

SPY kept going up & TLT kept getting discarded & trashed all through May 2007. But TLT made a bottom in early June 2007 and didn’t look back. Now let us use the “next couple of months” window Barbara Reinhard said is positive for her. That takes us from July 18 to August 18 2007 assuming “couple” means 2-3.

SPY rallied into mid-July 2007 & then sold off into mid-August and TLT rallied from mid-June 2007 into early September 2007. So the entire outperformance of SPY over TLT was reduced by mid-July 2007 & was totally extinguished by mid-August 2007. Now recall what happened on CNBC TV on August 3, 2007 :

Wonder now how quickly & steeply the economy & the credit conditions fell in June & July 2007 for Cramer to go so nuts (correctly we might add). Since we added that, allow us to wonder what drove Ms. Burnett to wear that dress on an important segment like this. Perhaps that animal-color led Cramer to go as animalistic as he did. Sorry, just kidofying of course!

Is there a slippage in the 2023 economy that is not being noticed by many outside of the Rosenberg coterie? Will it suddenly open into a smallish sinkhole by July 2023? We don’t have a clue but we recall very few except the Rosenberg coterie saw that economic slide in June-July 2007.

This is not an idle query. Because we heard Priya Misra of TD say on Friday on BTV Surveillance that she had added Treasury duration this week. She also said she prefers the 5-year Treasury to the 10-year Treasury & longer maturities. Listen to her directly on the Bloomberg Surveillance Friday clip (minute 26:59 to minute 33:51).

- “I still think we are about 6 months away from the first rate cut; risks are they don’t even cut this year; they start to cut next year; they are so hyper-focused on inflation; they are looking for a slowdown; I think they might be a little late; once they start to cut, I think they are going to cut a lot more than what’s priced in; the market is pricing what we are calling the trough rate; the end-point of these cuts is at 3%; 3% is actually higher than the Fed’s estimate of a neutral rate; so the market us not pricing in a recession; the market is pricing in normalization; …. in our view it is going to be a recession because of the bank-lending standards … because of the lagged impact of rate hikes … & now we might even have fiscal drag; the only way to get a debt ceiling deal is to get that fiscal drag;”

- “so as the economy slows down, I think the Fed is going to cut a lot more; but if you are too far out, there are a lot of factors that can move long-end rates; 5-years is the sweet spot; 3-5 yr rates are actually very attractive because they are positioning for the Fed whenever they start to cut or just an idea they are going to cut; the 10yr is benefiting from a significant inflow in bond market mutual funds; .”.

- “the economy is not that volatile; right now we are seeing a slowdown; once that starts to build up, I think it [economy] is going to lose momentum really fast; .. we are looking at the 10-yr below 3% by year-end; 2.5% by next year; so the 10-yr will also have a significant move; I just like the 5-yr a little bit more right now; …

4. Now Russia steps up

Last week we wrote about what we consider to be a globally mega deal that would connect the Indian Ocean to Europe via ship to Abu Dhabi to a new railway network from Abu Dhabi across Saudi Arabia to Haifa in Israel. As we pointed out, this globally mega deal is being handled by National Security Advisors of USA, UAE, Saudi Arabia, Israel & India.

It is obvious that this globally mega deal will exclude Russia, Iran & much of Central Asia. So guess what? Russia & Iran stepped up big & fast. By Big we mean at the level of President Putin & President Raisi of Iran. By fast we mean an agreement to complete the missing 164 km railway across Iran within 3 years.

Once that agreement was signed this week, President Putin announced that it will cut the St. Petersburg to Mumbai transport time to 10 days. Watch & listen to Putin and read about the ramifications in our adjacent article Now The Other Side of the Globally Mega Deal.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on Twitter