Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Two Huge Events or Three?

No question about the first huge event: Yes it is a team game but America’s MVP is Jalen Brunson. He scored 45 points out of 94 points to drive Knicks to a great NBA Championship. And he tied Michael Jordan’s record in doing so. Just huge.

The second huge event was the IPO of SpaceX. As a result, we now have the World’s First Trillionaire in Elon Musk. The underwriters, Goldman Sachs & Morgan Stanley, deserve huge credit in managing it so well. The market jumped 36% in the last 2 days & the Dow rallied by 1280 points. Gold, Silver rallied hard, Dollar fell & Treasury yields fell a bit.

There is no one better than President Trump in his ingenuity & flexibility in getting out of seemingly impossible situations. That has been our belief & indeed our conviction. It was proven true again this past week. Thru smart & flexible negotiations & his skill to creating the right media framing, President Trump has now announced completion of a US-Iran deal to end the war. We will know in a while how this deal works out. If it does, then this would be the Biggest Huge Event not just of this week but for this year.

Thank you President Trump and a Very Happy 80th Birthday to You!

2. Markets Last Week

2.1 US Indices:

- VIX down 18%; Dow up 27 bps; SPX up 64 bps; RSP up 1.8%; NDX up 2.3%; RUT up 3.9%; MDY up 2.8%; XLU up 41 bps; SMH up 8.8%; SOXL up 28.6%

Semis reassert leadership:

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – $SMH +9% this week… will easily print a record high today

And,

- Trader Z@TraderZ – $SOXLis +50% in 4 days from intra-day lows by the way.

A leadership change in addition?

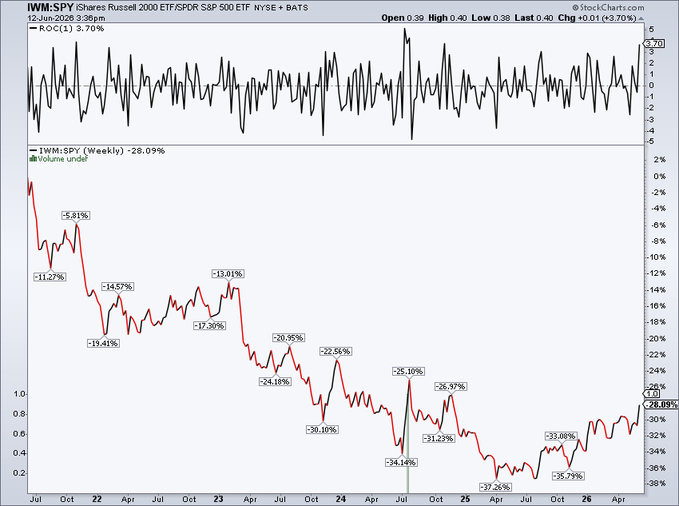

- Markets & Mayhem@Mayhem4Markets – The Russell 2000 is breaking out.

And a leadership change?

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – $IWM vs $SPY … ... best week since Nov 2024… fresh relative high back to then as well. Small caps now beating large caps since Oct 2023

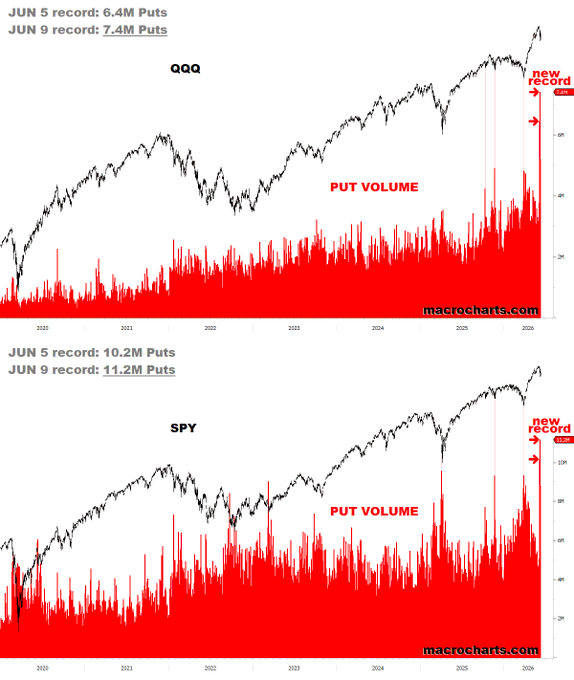

Too many puts, a reason for the rally?

- Macro Charts@MacroCharts – New record.

On Wednesday, Mike Wilson of Morgan Stanley came on Bloomberg & pointed out that earnings revisions, both in Semis & the S&P, have now exceeded their own expectations but the 2nd derivative of that change is suggesting a change in leadership. And he points to Consumer stocks, Transports, Regional Banks as beneficiaries of the change:

Mike Wilson was prosaic & helpful. In contrast, Rick Rieder on Friday went into phrases that flew over our simple head:

- “… I FEEL LIKE EVERY DAY I CAN’T KEEP UP…. THE NEWS FLOW IS, IS DYNAMIC, TO SAY THE LEAST. … IT’S THIS THIS CONCEPT OF DYNAMIC PATIENCE, MEANING YOU’VE GOT TO ADAPT TO THE NEWS FLOW. YOU’VE GOT TO TRY AND MANAGE YOUR RISK. YOU’VE GOT TO THINK THROUGH WHEN THINGS OVERREACT ONE WAY OR THE OTHER. … I STILL THINK EQUITIES WILL DO THEIR THING THIS YEAR. YOU GOT TO STAY IN THAT. AND THEN INCOME IS PHENOMENAL. …COMPOUNDING INCOME WORKS …..YOU KNOW WHAT IS TRICKIER IS WHEN EVERYTHING CORRELATES, WHEN RATES, EQUITIES, GOLD, ALL … YOU CAN LEAN IN A BIT. BUT YOU GOT TO BE A BIT CAREFUL ABOUT LEFT TAIL “

2.2 MAG 7:

- AAPL down 5.3%; AMZN down 3%; GOOGL down 2.4%; META down 4.4%; MSFT down 6.2%; NFLX down 2.2%; NVDA up 4 bps; MU up 13.6%;

A leadership change?

- The Chart Report@TheChartReport – Today’s Chart of the Day was shared by @scottcharts – The Russell 2000 closed at new all-time highs today while breaking out of an inverse head-and-shoulders relative to the Magnificent Seven.

Look what a recently criticized Mag 7 company has done!

Aren’t such AI centers huge power hogs? Yes & that is why this center is going to be based in Jamnagar where Reliance has its world’s largest and most complex single-site refinery in the world with 1.4 million barrels per day (MMBPD) crude processing capacity.

2.3 Key Financials:

- BAC up 4.1%; C up 5.6%; GS up 2.3%; JPM up 2.7%; KRE up 4.6%; EUFN up 4%; SCHW up 2.5%; APO up 4.6%; BX up 6.5%; KKR up 3%; XHB up 3.9%; ITB up 4.4%; NAIL up 12.6%; IGV down 5.4%; CRM down 10.7%; PANW up 2.8%; NOW down 9.2%

2.4 – Dollar & Metals

Dollar was down 25 bps on UUP & down 32 bps on DXY:

- Gold down 2.7%; GDX up 1.5%; Silver down 70 bps; Copper up 3.4%; CLF up 1.9%; FCX up 8%; MOS up 2%; Oil down 6.6%; Brent down 6.6%; OIH up 3.3%; XLE down 21 bps;

A recent AllStarCharts.com research piece pointed out:

- The importance of 100 goes well beyond the round number. It has repeatedly acted as a major pivot point over time. On top of that, the VWAP anchored from the COVID lows and the VWAP anchored from last year’s highs are both converging in the same area. When several levels align at the same price zone, that level tends to carry more weight. For now, the dollar remains below that threshold. As long as DXY stays beneath 100, the path of least resistance remains lower and the backdrop for risk assets remains bullish. A decisive move back above 100 would alter that picture. That’s the line in the sand

What about Gold?

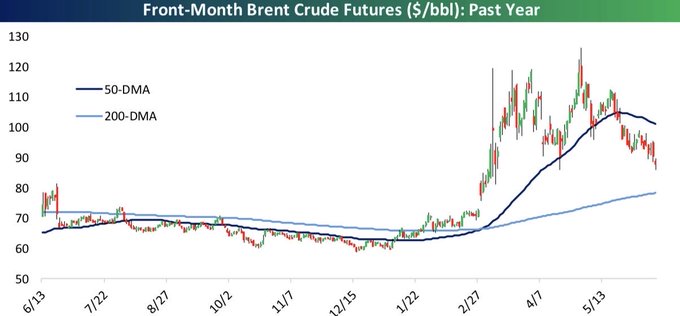

And now Oil:

- Bespoke@bespokeinvest – Crude oil started to break down at the end of the week, now closer to its 200-DMA below than it is to its 50-DMA above.

A new seller of LNG:

2.5 – International Stocks:

- EEM up 5.1%; FXI up 1.6%; KWEB up 3.2%; EWZ up 3.2%; EWY up 12.7%; EWG up 47 bps; INDA up 2.1%; INDY up 3.2%; EPI up 1.3%; SMIN up 1.4%;

Interesting clip – says $500 billion is the target for the move:

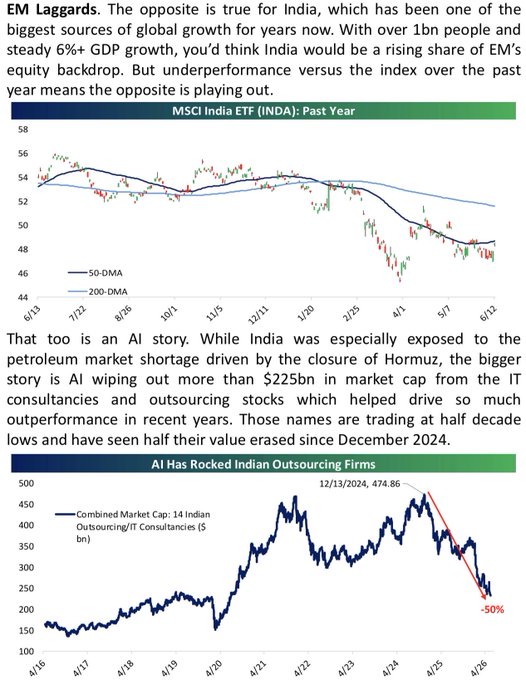

Indian market has been all about AI?

- Bespoke@bespokeinvest – India’s stock market has been in a downtrend all year. A big part of the reason is the AI obsolescence trade. IT consulting and outsourcing companies made up a quarter of India’s Sensex at the peak; that’s down to 14% after a 50% drawdown for the group.

On that topic,

- Tata Consultancy Services (TCS) on Thursday announced a global strategic partnership with Anthropic, the frontier AI company behind Claude, to help customers scale enterprise AI adoption. TCS will set up a dedicated business unit focused on delivering customer value propositions, joint industry solutions and AI expertise on the Claude family of models through early access to Claude models.

- The partnership is aimed at supporting enterprise AI deployment in regulated industries, where requirements for accuracy, auditability and oversight are more stringent, and the consequences of error are significantly higher. Combining TCS’ governance, controls and implementation expertise will enable enterprises to deploy Claude in production, not just in experimentation.

Going back to the Bespoke tweet above, Indian IT software & outsourcing companies have been hit hard as their core business has slowed down. And that has been one reason why performance of Indian Stock Market Indices has been so lackluster. But that might be just half the story.

We urge all to go back to Section 2.1 of our weekly article dated December 28, 2025. In that section, we discuss the Migration from Make Skill to Think Skill. Our introductory paragraph read:

- Today, leadership companies are moving to “Think” work by internalizing the tasks by building Global Capability Centers (“GCC“). These are captive units of global giants like JP Morgan, Walmart, Siemens and Boeing doing high value work – Data science, product design, cyber security, AI research, even R&D for electric vehicles and fintech.

A great American innovation for which, unfortunately, America doesn’t have adequate people-brain power. So, at that time, we pointed out:

- India is already home to 1580 GCCs, employing more than 1.6 million people and contributing upwards of $100 billion into the Indian economy.

What are the corresponding numbers now? As the clip below points out, India is now home to 2,100 GCCs employing 2.36 million people – a growth of 33% in the number of GCCs & a growth of 47.5% in number of people employed in the last 6 months. And the huge benefit is that the intellectual property remains 100% with the Corporation & is not shared with Indian Software companies.

That is one reason why performance of Indian IT companies has suffered while the Knowledge-Tec Sector of the Indian Economy has growth spectacularly. Apart from Indian IT companies, damage may have been done to job prospects for American & America-based technology employees. Watch the clip below titled INDIA’S GCC BOOM Is CRUSHING IT Services Hiring. Actually the title should read “Global GCC Boom” instead of India’s GCC boom.

Kudos to CNBC’s Scott Wapner who made some straight & fair points about the political debate in America about the H-1 Visa program and its impact on the US employment market. The original H-1 visa legislation was stupidly written in such a stupidly asinine debate that we are amazed it still survives. As an example, the original legislation mandated the SAME NUMBER of H-1 Visas Per Year across countries. That meant India was allocated the same number of H-1 visas as tiny adjacent Nepal or BanglaDesh or even then Gaddafi’s Libya. We also think the idea of mandating higher wages for a H-1 Visa job-seeker than for an American job-seeker would remove the “slave-labor” type characterizations.

Moving to a different sector,

2.6 Treasuries & Interest Rates:

- 30-year Treasury yield down 3.9 bps on the week; 20-yr yield down 5.1 bps; 10-yr down 5.9 bps; 7-yr down 6.9 bps; 5-yr down 7 bps; 3-yr down 7.8 bps; 2-yr down 7.3 bps; 1-yr down 0.2 bps;

- TLT up 83 bps; EDV up 97 bps; ZROZ up 11 bps; HYG up 64 bps; JNK up 60 bps;

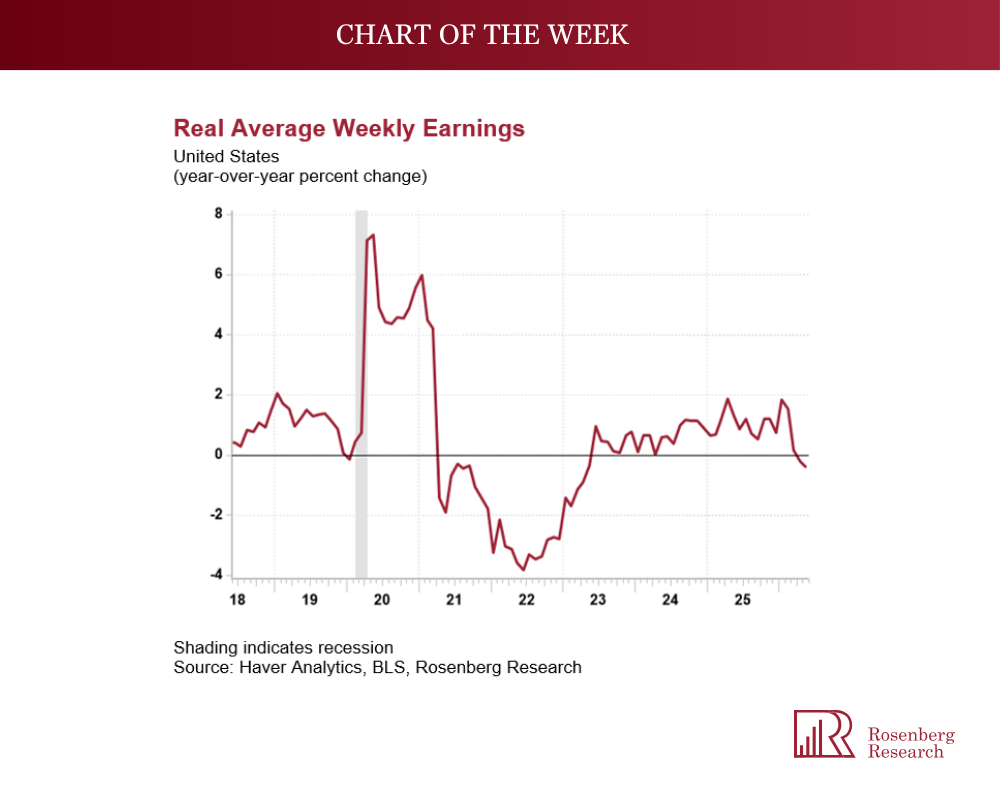

Can you talk about economy, inflation etc.. without bringing up Signor Rosenberg? We can’t now that we are into June, usually the pro-Rosie period!

- “core goods prices actually deflated −0.1% on the month, and there was barely a pulse when the total core index strips out the mismeasured shelter components. Second, there is also no spillover into wages, as real average weekly earnings fell −0.2% in May, having now contracted in each of the past three months — and dragging the YoY trend to negative −0.4% from +1.3% a year ago. As we have been saying time and again, this energy price shock hits the wall in the labor market with a contraction in real take-home pay, which then translates into negative prints on real consumer spending, which has already been slowing sharply of late….”

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.