Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.Markets Last Week

1.1 US Indices:

- VIX up 6.5% to 18.61; Dow down 44 bps; SPX up 55 bps; RSP down 56 bps; NDX up 2.4%; ; RUT up 36 bps; MDY down 14 bps; XLU up 4 bps; SMH up 9.1%; SOXL up 35.6%

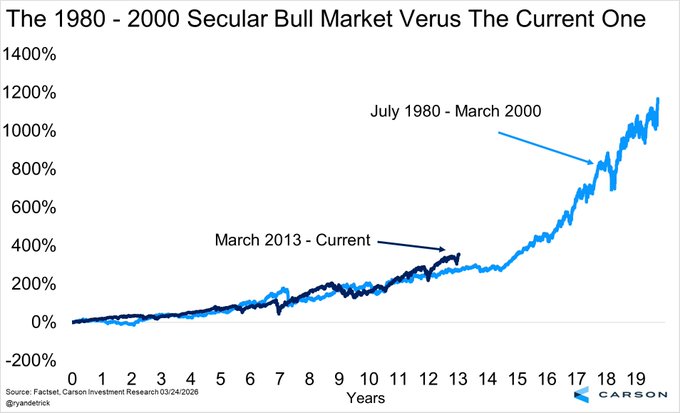

How long can this market run? One view says:

- Ryan Detrick, CMT@RyanDetrick – The last secular bull market lasted nearly 20 years. This one is just over 13 years. Be aware this could still keep going much longer than most think.

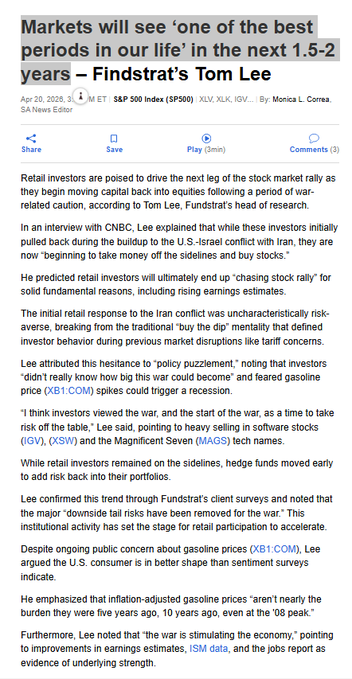

Another view speaks to the rewards of this bull market:

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – TOM LEE: Markets will see ‘one of the best periods in our life’ in the next 1.5-2 years @seekingalpha @fundstrat @fundstratdirect

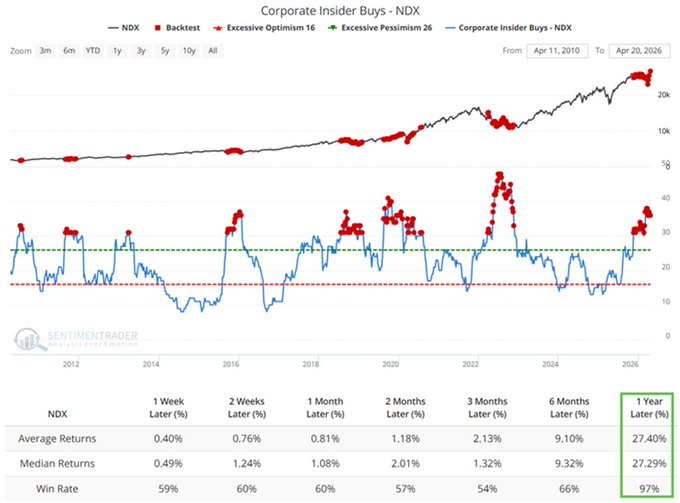

What are the insiders doing?

- Jay Kaeppel@jaykaeppel – NDX constituent company insiders are still buying. Are they crazy? Or crazy like a fox? Decide for yourself. @sentimentrader

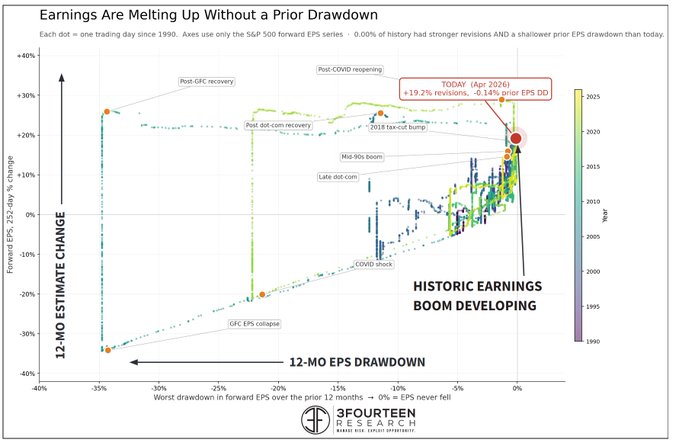

Not just company insiders. Warren Pies of 3Fourteen points out the fundamental reason for the market’s action:

- Warren Pies@WarrenPies – A historic earnings boom is developing. Estimates growing faster than they did in the mid-90s or late internet bubble years. Only covid recovery period saw a greater inflection. This boom is unique b/c it is not coming off an EPS drawdown (recovery).

Actually, as CNBC’s Mike Santoli points out in the clip below that Warren Pies raised his equity allocation the evening before. Watch how bullish he is despite his sedate tone & voice:

- “If it were not for the Strait of Hormuz, frankly, we would be max-overweight equities here; its an extremely bullish outlook if you could remove that variable from the equation; And I think what is happening is that the market is trying its best to look thru what is happening; to reiterate some of the bullish case: –

- this momentum thrust that we have seen off the bottom, as much as it feels like an overbought condition, you have to retrain your brain that these are very bullish things – a 63 day momentum thrust back in 2024 that ended the selloff then; a 28-day thrust that ended the selloff in 2025 & this is a 10-day momentum thrust – a very sharp & powerful thing;

- We have seen earnings grow by 9%; seen forward earnings grow by 9%; we are in 99th percentile in the S&P 500, I know that’s a bit concentrated in some of the hardware names …. supporting that is a fiscal backdrop, tax season that is coming off strong;

- the Mythos announcement – its been straight up for the Semis since then … its an ideal backdrop for the bull market when you see front-tier model improvement that gives you a green flag for “compute” demand & it ratifies the hyperscalar cap-ex & finally allows you to dream about the usercases from better models … So I think that’s a very bullish outcome ex-state of Hormuz

Mike Santoli pointed out that “the market is assuming …. the dominance of the cap-ex theme can sort of overcome whatever friction is caused by higher oil prices or a little bit of a sluggish job market“.

- Warren Pies replied “that is the push back; we put up a chart that shows earnings estimates have inflected higher than we have ever seen ….. it is very rare that … earnings estimates inflect by 20% year/year … earnings estimate breadth is rising & there are some pockets that related to the AI-buildout that are extreme right now – its a pushback – not something that has me worried really“

We are really scared to write what we are about to for sheer fear of jinxing it – The combination of Mike Santoli & Melissa Lee is working very well; both are intelligent & smart and they seem to working for us dumb viewers. Kudos to CNBC Mgmt for putting them together for the 4 pm show.

Max Kettner of HSBC said “basically we are bullish on every risk asset that we can… high-yield, EM Credit, Local Currency Debt, really across the risk asset spectrum; perhaps high-yield credit less so – about 25 bps from all-time highs“.

On the other hand,

- Scott Brown, CMT@scottcharts – The SOXX ETF (iShares Semiconductor ETF) is up 18 days in a row and +49% in that time. The best comparable reading the PHLX Semiconductor Index saw in the dot-com bubble was +44%, and it marked the March 2000 top

2.2 MAG 7:

- AAPL up 31 bps; AMZN up 5.4%; GOOGL up 80 bps; META down 2%; MSFT up 43 bps; NFLX down 5%; NVDA up 3.3%; MU up 9.2%;

What a fantastic call by Dan Niles to make Intel his largest position in March & argue that CPUs were better focus than GPUs! He said this week that ” … YOU’RE ONLY A FEW MONTHS INTO THIS AGENTIC STUFF. AND SO YOU SHOULD SEE VERY STRONG DEMAND, AT LEAST I THINK FOR THE NEXT YEAR AS CORPORATIONS PUT MORE AUTHENTIC WORKFLOWS IN BECAUSE IT HASN’T BEEN AROUND THAT LONG.”

Below we point out another bullish factor that Warren Pies described in his clip above about Hyperscalars:

- “… I think the macro concern that was with us in the beginning of the year is, I believe” lifting; … that macro concern was that this cap-ex was too much & it was going to crowd out other important, supportive behavioral-like share buybacks; I think the market had a little bit of cold feet with those cap-ex numbers ; … when you get the frontier-end models with those cap-ex numbers with the best improvement we have seen in years; you see what’s happening in the Semis; all of a sudden you have to rethink – may be that Cap-ex is in line or even not enough… you are seeing reports out of the Mag 7 – layoffs, employee buyouts at Microsoft, – there may be other levers they can pull to maintain buybacks & that’s the calculus that’s going on in the Macro Level; as you are seeing these models come thru in the scramble … for “compute” rally really take off…

2.3 Key Financials:

- BAC down 3.5%; C down 3.2%; GS up 10 bps; JPM down 65 bps; KRE down 2.1%; EUFN down 3.7%; SCHW down 4.1%; APO down 29 bps; BX down 5.8%; KKR down 1.7%; XHB up 1.1%; ITB up 1.6%; NAIL up 4.6%;

2.4 – Dollar & Metals

Dollar was up 44 bps on UUP & up 32 bps on DXY:

- Gold down 3%; GDX down 6%; Silver down 6.8%; Copper down 92 bps; CLF down 1.8%; FCX down 13.1%; MOS down 2.3%; Oil up 12.1%; Brent up 16.8%; OIH up 9.1%; XLE up 3.4%;

Comments about the US Energy sector are in the section below:

2.5 – International Stocks:

- EEM up 16 bps; FXI down 2%; KWEB down 5.3%; EWZ down 3%; EWY up 1.5%; EWG down 1.9%; INDA down 3.3%; INDY down 3.6%; EPI down 3.2%; SMIN down 3%;

The conditions in the Strait of Hormuz & its impact on Oil price & shipping is probably the critical factor at this time. Below, Ajay Raja-Dhyak-Sha (phonetically), the global chairman of research at Barclays, presents his views.

- There’s two things happening which collectively investors analysts underestimated.

- The first is and I know this sounds a little bad to say Sherry but the major economies the economies that matter to the world have less exposure to what is happening in Hormuz than many others. So the United States for example is a gigantic energy superpower. Sure prices go up that hurts the consumer but it’s largely a wealth transfer from US consumers to US energy majors. China, it is an energy importer, but it’s a big leader in clean tech. It has 1.2 billion barrels in reserves. Takaichi-San came out a couple of weeks ago saying, “Look, Japan still has 143 days of reserves.” Perhaps the one big economy impacted pretty significantly arguably is India. But for the most part so far, the damage has been in economies that just don’t matter as much on the world stage. You know, many of them are in this part of the world. the Philippines, Thailand, Pakistan, you know, soft works from home. It’s bad for those economies. It just doesn’t matter in a global context.

- And the second thing is that and I think we all underestimated this. I’m telling you, 2 months ago, if you had asked any oil analyst that Hormuz is going to be closed for 8 weeks, they would all have been running around with their heads on fire saying the world is ending. And it has been 8 weeks and that has not happened. And I think the reason is because the world collectively had slightly more inventories, a little more runway than we all estimated. And that is what we are we are playing our way through. But there’s no question about it. Every passing week now where Hormuz doesn’t open, It starts to ratchet up the pressure. It makes the equity rally staying at these levels are continuing more difficult. That part is true.

CNBC’s Sherry asked whether the market is due for a pullback or whether he “sees more FOMOing into equities from here?”

- Ajay – I do not think we get a sustained pullback. …. but I also think the equity rally is not just FOMO. This week I would argue was the first time where you had the long onlies who had degrossed a lot more than they should have in the initial round of selloff … God Forbid if there is an actual final deal then stocks will take off even further and we’ll be left behind. So this week that is starting to play out. It is showing up in every minor dip being bought. But there is a fundamental here at work. … Last year, the S&P 500’s earnings were up 12%. This year, coming into the war, consensus year/year on-year expectations were for earnings growth of 15%. That is not small. That is not something that analysts just pull out of a hat. They do channel checks. They focus on ongoing guidance from companies. Now, sure, ese these estimates usually tend to be a little more optimistic, but year-over-year, we were looking before the war started at one of the strongest years of earnings growth since the GFC and markets largely we think once they figured out that a ceasefire can stay in place that the United States is less exposed. We’re reacting to that. You you I mean, next week you’re going to start getting big six earnings on board. I would not want to be short going into that.

Another CNBC host asked a pointed question – “Do you think the outlook for risks for earnings, not this quarter but in the succeeding quarters of this year, might actually be rising?”

Ajay answered:

- “the risk is rising to the downside like I said every passing week makes life a little more difficult but less so than we all thought number one. Number two is the US equity markets are much much more insulated than the Asian equity markets than the European equity markets because sometimes it’s easy to to to go away from this fact but the United States is a gigantic energy superpower. It is it’s not just a technology superpower or military one. The United States produces over 20 million barrels a day of crude and refined products. So yes, it imports some crude of the type that it wants. it exports roughly the same amount of refined products. So that’s where you get a wealth transfer between the consumer and the US energy sector when prices go up on energy you know the money doesn’t largely leak out number one and number two is … if you look at the US equity sector as a whole right tech together is as much as 40% by valuation that is almost a cyclical you know I cannot overstate this enough guys I know that the Iran war is the topic dour every single day there is a new user

case that comes out in AI that drives both the bottom line and the top line. So yes, if oil goes up to $120 a barrel and stays there for 3 to four months, I would absolutely be worried. There is a level of oil where the US consumers starts to pull back hard, but we are not … anywhere close to that level. And just getting to 120 won’t do it. You need to stay at 120 for a long time.”

Then a CNBC host asked an interesting question – “Ajay, picking up on what you’re saying about the United States being not just a tech superpower, but an energy superpower as well. Three weeks ago, President Trump said, “Come and buy all from us. Come and buy from the United States of America. We have plenty.” And we’re already seeing, you know, countries from Europe to Asia needing to go to the US cap in hand and buying more of their crude, buying more of their natural gas as well. Do you think that this was all part of the original big plan for going hard on Iran?“

Ajay’s response:

- “No, I don’t think so. I do think that the like you said the US energy complex is one of the biggest winners in this; not so much on crude because oil is a fungible commodity right there is only a certain amount of oil is a physical commodity if it doesn’t flow at some point it hurts everyone it hurts Asia a lot more it hurts Europe a lot more but it hurts everyone and it’s a it’s a global asset. Natural gas is not a global asset… our gas prices actually went down since the war started. We have natural gas coming out of our ears. We don’t know what to do with it. And the good news for the United States is between 2026 to 2028. Every single year, the United States is putting in place more LNG, you know, because gas needs to be liquefied, then you transport it across in a tanker across the Atlantic. Then it gets gasified and then you pipe it to homes in Europe, right? That’s the process. So, we’re adding more LG permitting capacity every year than we ever have for the next 3 years straight. Europe is going to turn far far more to the United States than it has so far for natural gas. But for oil Hormuz needs to be solved. The United States by itself cannot solve the world’s oil problems. Nat gas. Yes.”

Just as a footnote, it is very smart of the CNBC team to ONLY use Ajay, the above guest’s first name. His last name is an inherited professional title which means Royal (Raj)-Adhya (chief)-Aksha (eyes or with responsibility) which is the title given to a Royally appointed Head Administrator . Clearly one of his ancestors was such a Royally Appointed Head Administrator.

Sauns-Krut is not only a recital-primary language BUT it is a language originally developed from Sound prior to humankind using any written material. This is why it is perfect to use with Quantum Vibration study & analysis and why spelling Sauns-Krut words today have to be uniquely spoken & have to be written as they are written. One day, we will include short clip of how a language can arise only from Sound.

2.6 Treasuries & Interest Rates:

- 30-year Treasury yield up 3.1 bps on the week; 20-yr yield up 4.5 bps; 10-yr up 6.2 bps; 7-yr up 7.5 bps; 5-yr up 7.8 bps; 3-yr up 8.5 bps; 2-yr up 0.1 bps; 1-yr up 3 bps;

- TLT down 41 bps; EDV down 46 bps ; ZROZ down 57 bps; HYG down 21 bps; JNK down 20 bps;

3. A Serious Crisis Again a Major Opportunity?

As Ajay Rajadhyaksha, global chairman of Barclays, said in the above CNBC clip,

- “the one big economy impacted pretty significantly arguably is India“.

He is absolutely correct. The Crisis in the Persian Gulf has hit India hard in a number of different ways. First obviously in terms of Oil Price & LNG price. India was caught without a huge Oil reserve unlike China & Japan. Over 50% of India’s oil imports came from the Strait of Hormuz. That’s history at least for a while. But a new pact with Russia has helped Indian Oil companies to acquire about 60 million barrels of Oil for April.

But oil is not India’s really big issue. The Emirates & other trading partners around the Strait of Hormuz were significant trading partners for India. In addition, remittances from the Indian expat community from the Persian Gulf were a very important source of Revenue. From what we hear, over a million of Indian-residents in the Gulf have returned to India.

So the question is whether there is anything that suggests a major new opportunity for India. Read on and decide for yourselves.

3.1 Remember the Adani Washout? And then the resurgence?

That sell-off resulting from “revelations” from a notorious short-seller rocked the stock of Adani group of companies in February 2023. That entire group was thrown by the wayside by the global media. We thought differently & wrote two more articles titled Adani Reflections – II & Adani Stabilization – III. You could have bought stock of Adani Ports around that time at or below Rs. 500/-. This week it traded at Rs. 1600/- (up more than 300% in just over 3 years. Not only that but the stock was up 20% in this month of April, 2026. Why you ask?

(Vizhinjam Port, Keral, India) (Dubai Jebel Ali port)

Because Adani’s Vizhinjam mega port, that opened in October 23, has proved its importance. It is a mega Transshipment port located a mere 10 nautical miles from the ocean route from Malacca Strait into the Indian Ocean. As we all know, Dubai, the previous mega destination of shippers, is now shut down for a period of time.

So, reportedly, about 100 mega container ships are waiting in line to dock at Vizhinjam port. No wonder the Adani Ports stock is up 20% in April. And yes, Adani Ports is building a 2nd terminal due for completion in 2 years and India is building another International Transshipment port about 140 miles from Mumbai.

If you look at a map, you will see that Mumbai is directly across the Arabian sea from Duqm, the Omani port that is already linked by road & soon by rail with Emirates & Saudi Arabia, bypassing the Gulf of Oman & the Strait of Hormuz.

In addition, 51% of the ownership of the port of Colombo in Sri Lanka, a current mega destination has recently been acquired by Mazagaon Docks located near Mumbai. That means these two Indian ports will now dominate the huge volume of mega-containers that need deep Transshipment ports in the huge Indian Ocean area.

Guess the title of the October 2023 clip below proved prescient:

3.2 Enter South Korea, Japan & Germany:

The impact of the war in the Strait of Hormuz seems to have created an urgent need for major US allies in the Pacific to expand their relationships. Reportedly, this was triggered when the US removed the Patriot & THADD missiles from South Korea & Japan for use in the Strait of Hormuz.

The first country to move was South Korea which faces nuclear-armed North Korea. South Korea has enjoyed excellent trade relations with India with major companies like Hyundai, Kia, Samsung active in India. But this week, the President of South Korea travelled to India to sign a deal that reaches $50 Billion by 2030 & includes military equipment.

And Japan broke its old ban on defense deals & embarked on a new policy as described below:

And, in a first, Germany will build sophisticated submarines at the Mazagaon Docks in India in a deal that includes the transfer of critical technologies, including propulsion systems, stealth features, and combat management systems. The submarines will be equipped with Air-Independent Propulsion, allowing them to stay underwater longer and operate with greater stealth.

The above are all this week’s events. The speed of these deals seems to show the urgency of the medium powers, all US Allies, to expand their Technology, Defense deals with India.

We could be wrong but the speed & depth of these deals suggest the size of India, its dominant position in the Indian Ocean, and the power of its military, were important factors given how mere economic deals with the Mid-East economic powers proved transient.

In addition, the exclusive control of Vizhinjam port & Colombo Port is very positive for India’s continued business expansion into Africa. Just notice how close the Red Sea & Bab-el-Mandab strait is to India’s southern bases.

4. Ajay of Barclays vs. VK of Barclays

Our attempt here is to clear up some misconceptions & avoid potentially dangerous insults to the name of Shri Krushn, one of the 2 main Avataar of God on earth. The last name “Raja-Dhyak-Sha” is a non-Religious name, let alone be deemed blasphemous. On the other hand, the name Venu-Krushn (VK for us) of one of Ajay’s colleagues is extremely beloved of almost every Hindu in the world. How can CNBC invite the strategist involved while avoiding the intense insult to Hindus worldwide? Below is a gentle suggestion from us.

First Venu itself is a feminine term for a musical instrument like a Sitaar or Sarod. There is no masculine color to either instrument. So using it for a man, even a strategist at a major firm, by CNBC is insulting besides being defamatory to over a billion Hindus, both religious & atheist.

And it is common to use a compound term like Venu-Gopaal, meaning Gopaal with his Venu & Venu-Krushn meaning Krushn with his Venu. See the image below. Add to this appalling insult to Avataar Krushn by saying his name with a feminine “aa” sound like Krishnaa.

Given this, we would like to suggest a simple tactic that will enable the Barclays strategist to be invited on CNBC (in every show, on every day if so desired) without offending anyone.

We knew a professor of Mathematics at a major southwestern university who had to deal with the same problem. He did something very smart, something that is routinely done in India even today. He used the initials VK as his addressable name. Every student, every other professor knew him as VK or Professor VK. Despite our year-long association, we NEVER knew what V or K or VK stood for. Knowing him as VK was enough for every one at the Math. Department.

Would the pair of Mr. Vxxx-Krushn and CNBC accept this simple & commonly used method to address the Barclays gentleman gracefully as VK on the shows & avoid causing massive religious offence to the feelings of Avataar Shri Krushn? Again this is offered merely as a simple suggestion to help both this gentleman & the network we watch so often.

- And to help our emotions as well – Our Mother’s name was Venu & our Father’s name as Shri Krushn. So we have known & deeply cared about Venu-Krushn as an entity since our childhood.

Below is an excerpt from the immortal poem from 1200 CE by Poet Jayadev that describes Avataar Shri Krushn playing his flute & the effect it has on the forest, animals & people who came to listen. We have heard this exquisite poem since our childhood.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X