Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1.One Step Further

Last week, Janet Yellen said “It’s possible we saw the last rate hike of the cycle “. Now this week, according to the Wall Street Journal,

- LongConvexity@LONGCONVEXITY – The latest Fed discussions indicate the bond portfolio runoff could end much sooner than expected. Next week’s meeting could yield more clues.https://www.wsj.com/articles/

fed-officials-weigh-earlier- than-expected-end-to-bond- portfolio-runoff-11548412201… via @WSJ

Specifically, what is in sight is “an end to the central bank’s portfolio wind-down“. So not only are rate hikes done but QT is also done?

The big question is how this is to be read. The hopeful option is:

- Lisa AbramowiczVerified account@lisaabramowicz1 – The Fed is “at the mercy of the markets…That’s why we have re-instigated a risk position” across stocks in the U.S. and emerging markets.

The Bloomberg article describes the views of Wouter Sturkenboom, Northern Trust Asset Management’s Amsterdam-based chief investment strategist for Europe and Asia. That firm sees sees “clear sailing for the rally for now.” They are “adding equities and bonds of developing nations while cutting cash and government debt“.

The Bloomberg article describes the views of Wouter Sturkenboom, Northern Trust Asset Management’s Amsterdam-based chief investment strategist for Europe and Asia. That firm sees sees “clear sailing for the rally for now.” They are “adding equities and bonds of developing nations while cutting cash and government debt“.

They think, “the five-year U.S. government bond yield would need to rise “meaningfully” to give the central bank the green light to push ahead with its indicative tightening plan“. And the other factor is “the belief that the greenback is losing steam“. Simply put,

- “If the Fed is pausing, if inflation is moderate, then a lot of the hugely wide rate differentials and spread differentials between the U.S. and the rest of the world will start to ease”

The other or a non-optimistic view was articulated by Greg Jensen of Bridgewater from Davos:

- “While people have certainly diminished their growth expectations and you’re hearing all about that at Davos, we don’t think they’ve done it enough,”

- “Earnings expectations particularly in the U.S. are too high, and generally the Fed and other policy makers are still expecting stronger growth than we see.”

- He expects to see “lower interests rates, particularly on the short-end of the Treasury curve. Regions that have priced in high growth expectations will be hurt the most. On the other hand, some emerging markets that have already suffered from the U.S.’s tighter monetary policy will benefit as policy makers resume easing,”

- “European markets will be the first test … as the region is “starting from a worse level in terms of the economy, lower inflation — close to deflation in many places — and already have negative interest rates, … Their movement will be kind of a leading indicator because they’re going to struggle more with”

Speaking of diminished growth expectations, you have:

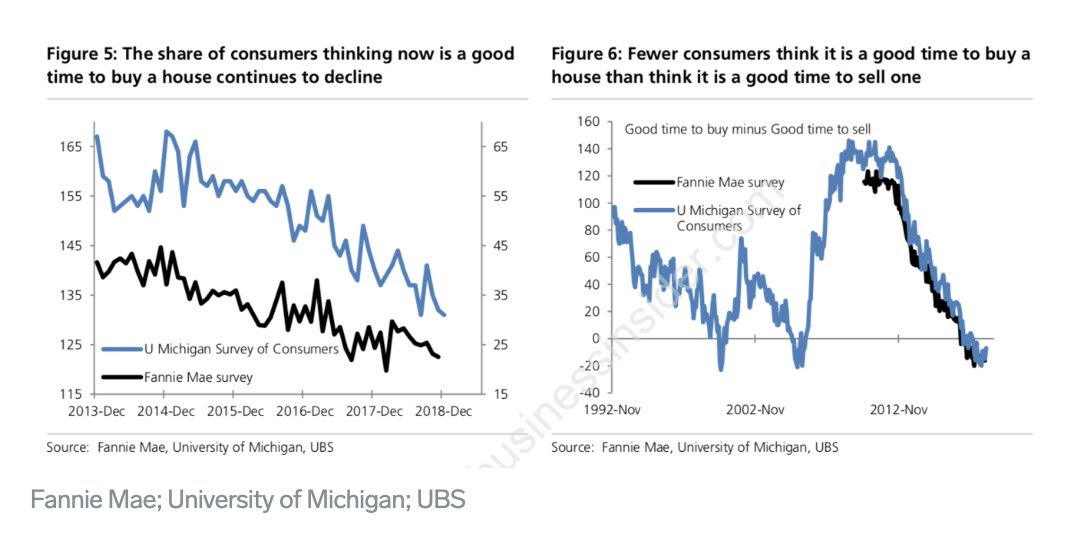

- Trevor Noren @trevornoren – .@UBS: “# of consumers who say it’s favorable time to buy a home has fallen below # who say it’s a good time to sell…happened only twice in 26 years those survey questions have been asked—and those instances preceded our two most recent recessions” https://www.businessinsider.

com/falling-home-sales-could- signal-us-recession-2019-1 …

Our own belief is that the Fed is steadily falling behind the economic cycle and they have little chance of reversing the US slowdown unless they jump ahead by cutting interest rates. Now that they have 3 weeks of respite from the shutdown, they should use to cut interest rates next Wednesday. But they won’t because of the blasted concept of Fed’s credibility which dictates Fed should move slowly & deliberately rather than moving at battle speed.

Our own belief is that the Fed is steadily falling behind the economic cycle and they have little chance of reversing the US slowdown unless they jump ahead by cutting interest rates. Now that they have 3 weeks of respite from the shutdown, they should use to cut interest rates next Wednesday. But they won’t because of the blasted concept of Fed’s credibility which dictates Fed should move slowly & deliberately rather than moving at battle speed.

Moving across the Pacific brings us to the real danger & its cause:

- Jesse Felder @jessefelder – ‘I fear this will be the third leg of the global debt supercycle, after subprime in the US and the eurozone debt crisis. It could be on the scale of 2008 and will be very bad for Asia, and there will be spillovers in Europe.’ https://www.smh.com.au/

business/the-economy/it-could- be-on-the-scale-of-2008- expert-sends-warning-on-china- downturn-20190124-p50t9q.html

The article describes the views presented by Professor Ken Rogoff at Davos and makes chilling reading:

- “key policy instruments of the Communist Party are losing traction and the country has exhausted its credit-driven growth model. This is rapidly becoming the greatest single threat to the global financial system.”

- “People have this stupefying belief that China is different from everywhere else and can grow to the moon, …. China can’t just keep creating credit. They are in a serious growth recession and the trade war is kicking them on the way down ”.

- “There will have to be a de facto nationalisation of large parts of the economy. I fear this really could be ‘it’ at last and they are going to have their own kind of Minsky moment,”

- He said it is an error to think that China’s current slowdown is entirely deliberate and calibrated. While the People’s Bank undoubtedly wishes to curb the credit boom, it is also riding a tiger that it cannot fully control.

That he calls, the “3rd leg of the global debt supercycle” that is on the scale of 2008. The danger he sees is “that China and Asian tigers could be forced to pull in some of their trillions of offshore global funds to cover urgent needs at home, drying up or even –reversing the Asian “savings glut”.”

- The eurozone is already suffering the fallout from the Asian downturn. Most of the region is in industrial recession. Germany and Italy buckled in the second half of 2018, and confidence has slumped to crisis-level lows in France.

- “I am very sceptical that the eurozone system can handle another big shock. It is a house half-built, and if there is something like 2008, it is all going to blow up. Some countries will have to be ring-fenced with capital controls,”

- The eurozone has little policy powder left to fight deflation. Interest rates are already minus 0.4 per cent and the ECB’s €2.6 trillion ($4.2 trillion) blitz of bond purchases has pushed the institution’s balance sheet to 43 per cent of GDP. The political bar to renewing quantitative easing is very high

- “This is the Achilles’ heel for Italy. Real borrowing costs could rise by 2-3 percentage points, … Italy’s debt dynamics could not withstand a regime shift of this sort. Markets would see the trouble coming and precipitate events.”

And you thought David Rosenberg was un-rosy!

2. Treasuries

Despite all the action in US Stocks, Treasuries can’t seem to maintain their high yields. This week the curve bull-flattened a bit again with the 30-year & 10-year yield falling by 4 bps & 3.8 bps on the week and the 2-year by 1.6 bps. The 5-year yield fell 3 bps to 2.584 once again falling a trifle behind the 1-year yield of 2.59%. German 30-year & 10-year yields fell twice as much as corresponding Treasuries, by 9 bps & 7 bps resp. TLT rallied by about 80 bps while HYG fell by 11 bps.

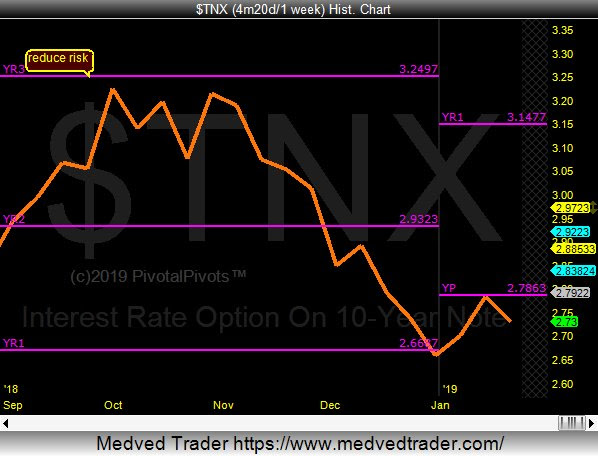

So where could the 10-year yield go?

- Jeff York, PPT@Pivotal_PivotsIs the Fed on Hold? So far, 10 yr. bond yields $TNX tested the 2019 YP @ 2.79% and got rejected there. Maybe a clue for the 2019 Ys1 pivot @ 2.33% @PivotalPivots.

If you thought 2.33% was low, listen to Carter Worth of CNBC Options Action predict 2.10% for the 10-year yield.

. In fact, Carter Worth recommended a pair-trade on Friday – Sell Amazon & Buy TLT.

That brings us to:

3. U.S. Stocks

Was this week a consolidation or the beginning of a down spell?

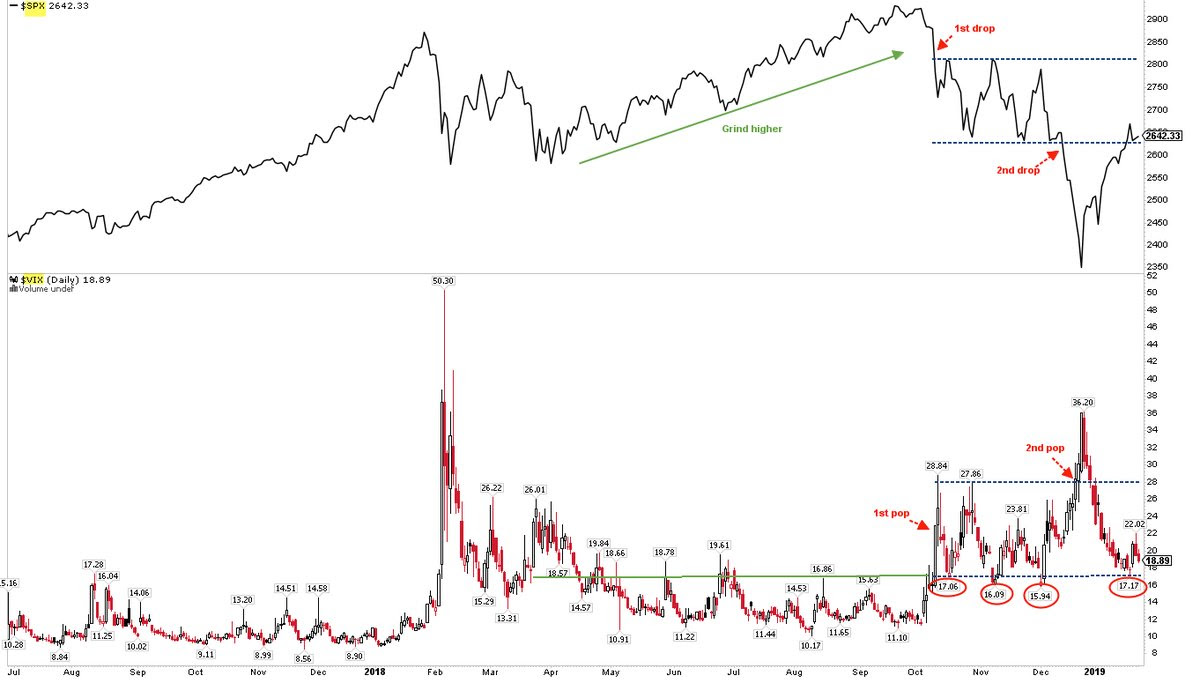

- Urban Carmel @ukarlewitz The bad news: $Vix at the bottom of a 4-mo range where every big sell off has started (circles) The good news: $Spx has regained (and so far holding) bottom of Oct-early Dec range A $vix drop under ~16 probably corresponds w/ $SPX grinding to the top of the range (~2800 area)

Lawrence McMillan of Option Strategist wrote in his Friday summary:

Lawrence McMillan of Option Strategist wrote in his Friday summary:

- “In summary, many of our indicators are still on buy signals. So we continue to feel that one should remain long for the short-term, rolling calls up to higher strikes to remove credits where appropriate and/or setting trailing stops as the rally progresses. Eventually, sell signals will emerge, and we will see then whether a bear market resumes or not. As long as $SPX is below 2800 and its 200-day Moving Average is declining, the chances of the resumption of the bear market loom large.”

The Dollar fell this week by about 65 bps but maintained its proximity to 96 on DXY.

- J.C. Parets @allstarcharts – do you guys think Euro is really going to crash here and head back down to the 2016 lows? Or dig in and start to rally from a very logical place? $EURUSD $DXY think about the implications that a weaker Dollar would have….

One implication is obviously Emerging Market Equities. So what did Mr. EM Equity, Mark Mobius, say to BTV on Friday:

Mobius said now is the time to buy their equities and favors India, Brazil and Turkey.

- “We’re particularly interested in India at this stage, … I just came back from a two-week trip to India and I was just amazed at the changes taking place. … It’s quite incredible, and of course you’re looking at 7 percent growth for a country that size, it’s very impressive,”

- His allocation is:

- 30 percent in India

- 30 percent in Latin America which includes Brazil, Argentina, Chile and Mexico

- 30 percent in Eastern Europe like Poland, Romania and Turkey

- The rest in China and other parts of Asia

Despite the election risk in India, Mobius said he doesn’t see a reversal of reforms, especially on the goods and services tax

- “There is no way that they are going to reverse it because everybody has got a vested interest. The states are benefiting from this and they have a say. One of the reasons why the country is growing is because the barriers between states are coming down”

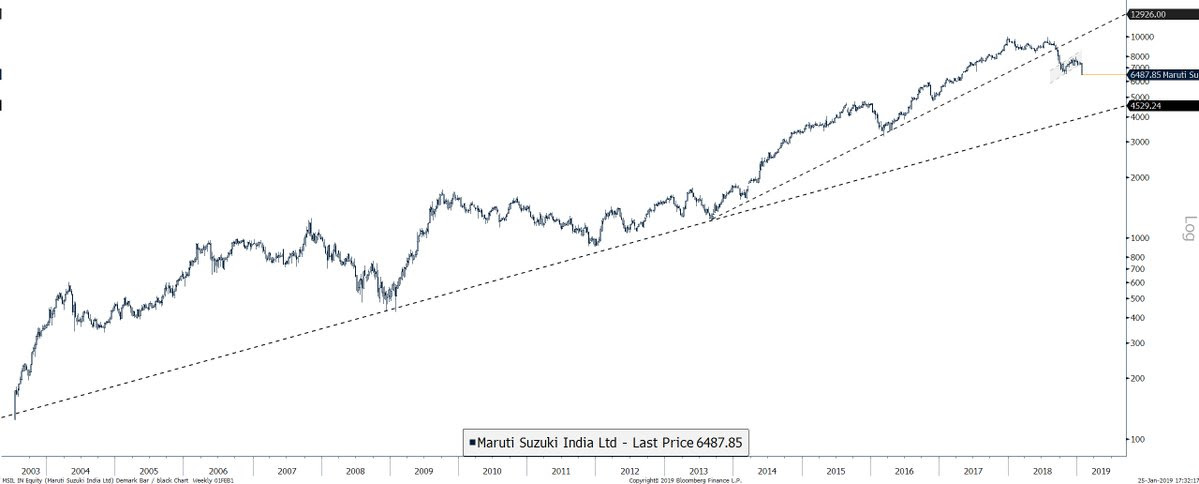

Mr. Mobius has forgotten more than we know but things don’t look all that great in India right now. The election is a big worry with the prospect of capital fleeing India if the result is a hung parliament with a coalition non-Modi prime minister. Consumer demand is not hot and there is a lot of rural stress.

- Real Vision Research @RVAnalysis – India’s largest car manufacturer misses profit estimates. breaks bear flag with heavy volume Adding to list of global auto companies missing sales and profit estimates

4. Gold

And what else does well as the Dollar loses steam and when the world looks dangerous? Gold rallied hard with Gold Miners up 4.5%. Silver rallied even harder. Previous rallies on Friday have dissipated during the following week. Will this rally be different?

5. Amazon in India

Will Amazon talk about their new challenge in India from Reliance and provide some guidance of their long term expectations in this week’s conference call? Amazon is the champion of low prices in America. But is Amazon prepared for India-style low prices? How low, do you ask? A Bloomberg article provides an answer:

- “Reliance Jio’s digital investments have already exceeded $40 billion. But in India’s hyper-competitive telecom market, the average revenue it can get from users isn’t even $2 a month.”

At that rate, even the 280 million customer base can only generate $560 million. At that rate, it would take Reliance almost 75 months to get their investment money back just on revenue & assuming zero operating costs.

On the other hand, the same customer base watches “almost 5 billion hours of video a month on their mobile phones and fiber broadband connections with [Reliance] Jio [phones]“.

So how does the retail business work with this base in an AWS+Retail platform? The Bloomberg article explains . Ambani’s plan is

- “to connect India’s 30 million small retailers with consumers. One, neighborhood marts will be connected to Reliance Retail Ltd.’s footprint of almost 10,000 stores, offering them common inventory-management, billing and tax platforms as well as low-cost payment terminals. That will give the expanded retail network formidable sourcing power.”

This seems incredibly ambitious. But then you see what Ambani’s entry in to telecom with Jio phones has done to the competition:

- “Vodaphone Idea Ltd. plans to raise as much as 250 billion rupees ($3.5 billion) via a rights offering to help India’s largest mobile-phone carrier fend off Asia’s richest man, who continues to roil the industry by providing 4G Internet at prices that would drive most carriers bankrupt in other countries.”

That has been the way for both Reliance in India and Amazon in America. The twain shall meet soon.

This Saturday is India’s Republic Day. National Geographic is unveiling the premier of Extreme Flying, a documentary on Indian Air Force. What web-platform did National Geographic choose to launch their documentary? Not Netflix in India, not Amazon Prime Video. They chose Hotstar, the web platform that is becoming a content giant in India. For more details, refer to the discussion on Hotstar vs. Netflix in our last week’s article.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints.com