Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Dissipation of Uncertainty – good or bad for S&P?

The big question now is will the S&P miss the trident of uncertainty? First & the least was the Fed & their posture going forward. Then it was the British election for its potential to cause disruption in markets & the European economy. And last & the un-least was the sword of Trump hanging over the stock markets in the form of new tariffs on December 15.

The first was dissipated on Wednesday by Chairman Powell both by his statement & his presser. Not only did he say no Fed hikes until inflation gets angrily visible & not only did he confirm the his liquidity-adding posture into year-end but he actually hinted about buying Treasury bonds (meaning QE) if necessary.

Then came a beacon of light from President Trump about tariffs on Thursday morning and the S&P exploded up by 27 handles. And the Treasury market gave its total backing by rates exploding up by about 10 bps across the 30-5 year curve.

Finally on Friday came the stunning news of the wipe out of Britain’s left & its semi-nuts leadership. The scale of the victory now raises the happy prospect of a settlement of the Brexit mess. As James Gorman, Chairman & CEO of Morgan Stanley, told CNBC’s Wilfred Frost “... what is good for the U.K., is going to be good for Europe“. It certainly proved so for British & European banks with Barclays up 7%, British pound up over 1% & UK stocks up almost 3%. And EUFN, the European Bank ETF, was up 3.8% on the week.

Getting to China, FXI rallied almost 6% despite the daily protests in Hong Kong & the Chinese A-share ETFs closed up 5%. And EEM, the broader EM etf, blew away the S&P by rallying almost 3% on the week.

But what might be the biggest result of the above uncertainty killing trident?

- Lawrence McDonald@Convertbond – A key global shift in economic balance – the scale was tipped far heavy into the USA – less so today. #election2020 #TradeDeal #BrexitRIP

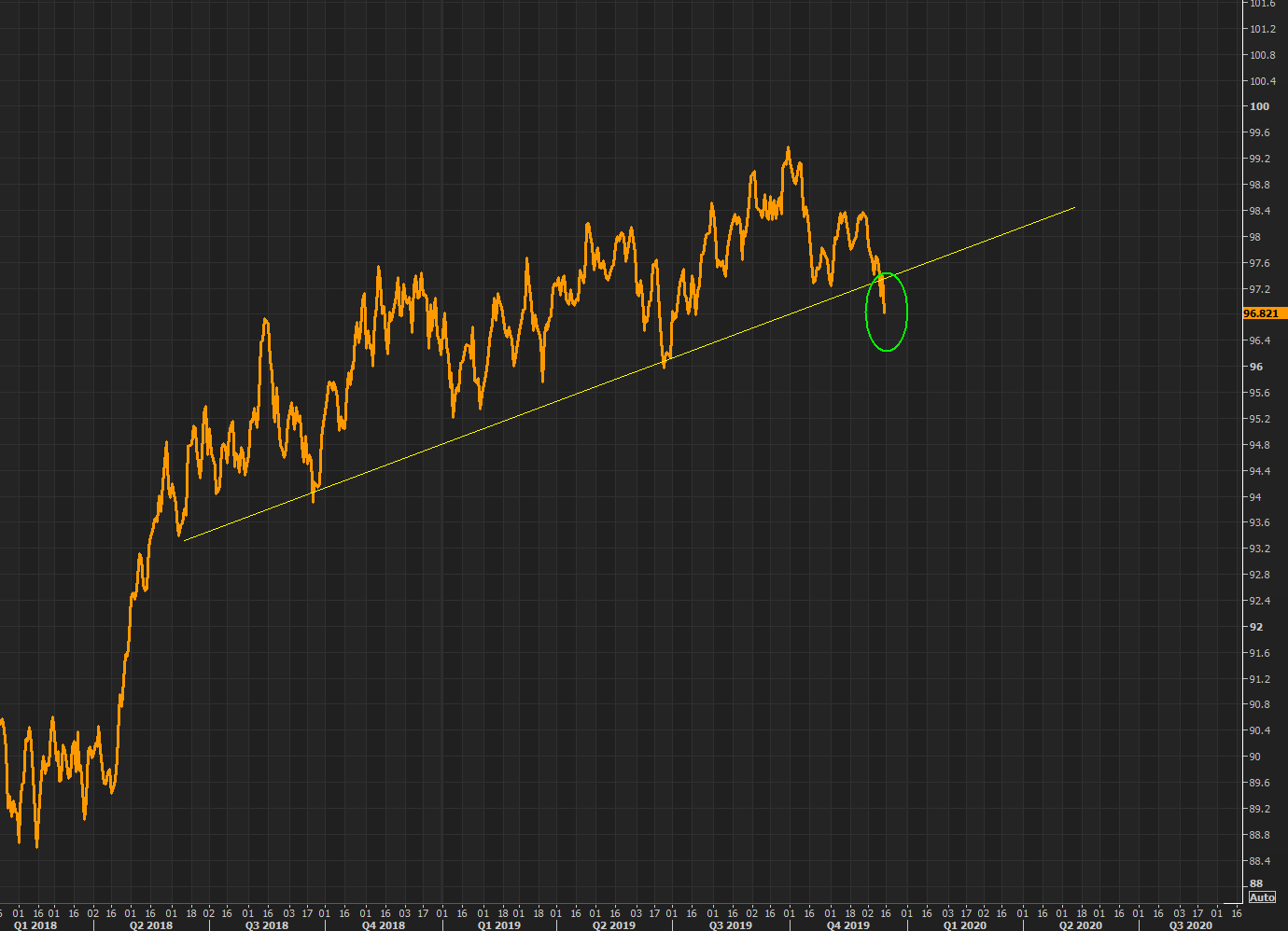

But what about the trendline that had not been broken so far?

- Market Ear – With all eyes on the mighty GBP, do not forget the much bigger trade of the weakening USD; DXY continues moving lower…

Look back to the past 10 years & ask what major trigger drove the Dollar weaker on a couple of occasions? A two-letter word – QE.

Sure, Dr. Powell tells us what he is doing now is NOT-QE and not QE. But if it talks, walks & act like QE, then can’t we at least pretend it is QE?

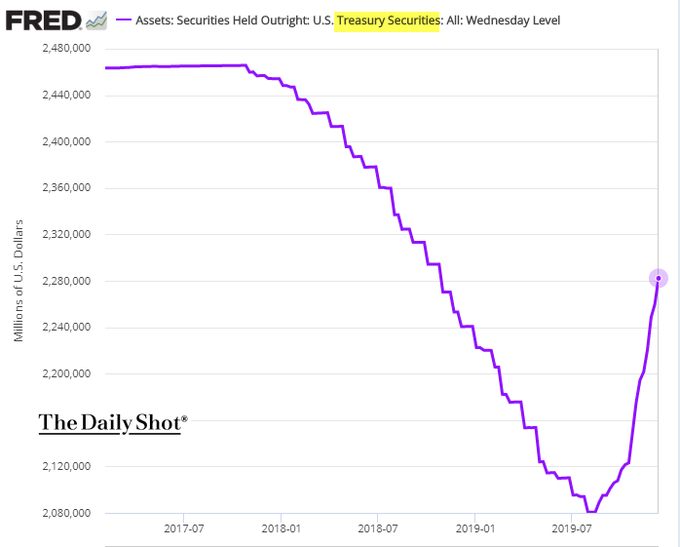

- (((The Daily Shot)))@SoberLook – The Fed has now bought about half of the Treasury securities it shed during the “balance sheet normalization.”

Isn’t the speed of the move more important in markets than the size of the move? It looks as if the normalization of the Fed’s balance sheet was on a down escalator while the re-expansion has been in an express up elevator. So, in the words of Lawrence McMillan of Option Strategist on Friday,

- In summary, the $SPX chart is strongly bullish, and that is the most important indicator. Really, the only sell signals are from put- call ratios and the mBB signal. So stay long and use trailing stops.

A big question is whether the end of uncertainty will remove obstacles for a rally in Q1 2020 or will it be as a DeMarkian said on Friday:

- Thomas Thornton@TommyThornton – Markets top on good news and since this trade deal have been anticipated for a year, this to me is pretty simple selling moment

He added in another tweet that “Dow Jones Industrial Average in wave 5 with new Sequential, and Combo 13.” Mr. Thornton has had a good track record with similar trend-exhaustion calls earlier this year. But, as we recall, that was before the Fed’s launch of Not-QE. Our own experience is that DeMarkian signals don’t work on the downside during QE phases while upside DeMarkian signals work well.

Case in point is Mr. Thornton’s bullish call on OIH we featured last week – “OIH Oil Service has downside Sequential Countdown 13. This is setting up for a long trade.” What a terrific call that was? OIH closed up 5%+ this week.

But what if the negative call on Dow Jones Industrial Average works next week? Our guess is that will just make the Santa Claus rally (post-Christmas into first couple of days in January) even more SantaClausian. And being SantaClausian is much much more fun that being a negative DeMarkian, isn’t it?

By the way, we read that smart bulls like Tony Dwyer & JP Morgan strategists have now raised their 2020 targets to north of 3400. But Michael Hartnett of BAML remains steady at 3333 by 3/3 of 2020.

Finally is there anything QE actually kills? Volatility. No wonder VIX closed below 13 on Friday.

2. Treasury Rates, Economy, Inflation

Removal of uncertainty had the natural effect on Treasury rates on Thursday – the entire 30-5 year Treasury curve exploded in yield by 9.5-10.5 bps on Thursday. And that is in spite of the strong 30-year auction on Thursday.

- Lawrence McDonald@Convertbond – Thu 12/12– Danger in Crowded Duration Finally, Clarity on Trade and Brexit Unintended consequences of a China – US trade deal with tariff rollbacks > than expected + a Boris Johnson landslide are striking for the bond market. Investors are too long duration – panic exit in the works

Then a strange thing happened on Friday. Almost 3/4 of Thursday’s explosive rise in Treasury rates was given up on Friday in a 6-8 bps fall in rates across the same 30-5 year curve. As a result, as Rick Santelli pointed out on Friday afternoon, buyers who had bought in this week’s Treasury auctions made money in each of the auctions by Friday’s close.

We also saw a reversal of opinion on Bloomberg Real Yield on Friday afternoon. This past summer Subadra Rajappa of SocGen was not in the rates will keep falling camp. But now she is calling for 1.2% 10-year rate by end of 2020. And, like Priya Misra of TD securities, she expects the Fed to cut rates 2-3 times in 2020.

Remember Bob Michele, JPMorgan Asset Management CIO & Global Fixed Income Head, who predicted the 10-year Treasury yield would fall to 1% this past summer? Now that the 10-year yield is at around 1.82%, BTV’s Jonathan Ferro asked him about his prediction for the 10-year yield in 2020. Look what Mr. Michele said:

- “I think we are going to test 1% and, if I am wrong, I think we are going lower“.

He thinks the Fed will be back into an easing mode in 2020. But what would a 1% 10-year yield mean for risk assets? He said,

- “It depends on what the Central Banks want; If they want to provide additional liquidity to the magnitude they did this year and you don’t have a recession, then all asset prices will inflate; “

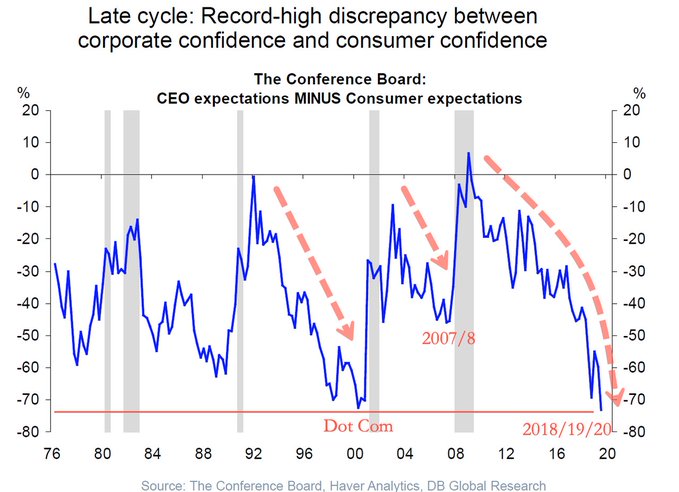

But why should the Fed come in & lower rates in 2020? Because underneath the happy stock market, the CEOs are not exhibiting confidence.

- Richard Bernstein@RBAdvisors – Consensus is the #household sector is very healthy. However, households are much more confident than are #CEOs and history says that’s not good.

We think the Fed now gets it & they will do everything they can to make sure we don’t have a severe slowdown in 2020, forget a recession.

Don’t forget the real possibility of a cut in payroll tax deduction in the first half of 2020, a cut that might be tailor-made to put more take-home money in pockets of households. This is a cut that the Powell Fed will support because they now understand that onset of deflationary potential is their biggest enemy.

Then you have the “most extraordinary dynamic we have ever seen” to quote Rick Rieder of BlackRock. Look what he quantified on CNBC Half Time on Thursday:

- “we are going to have $700 billion less supply [next year] than we had this year and the demand is going up a trillion & half just based on demographics, pension, insurance demand”

3. Stocks & Commodities

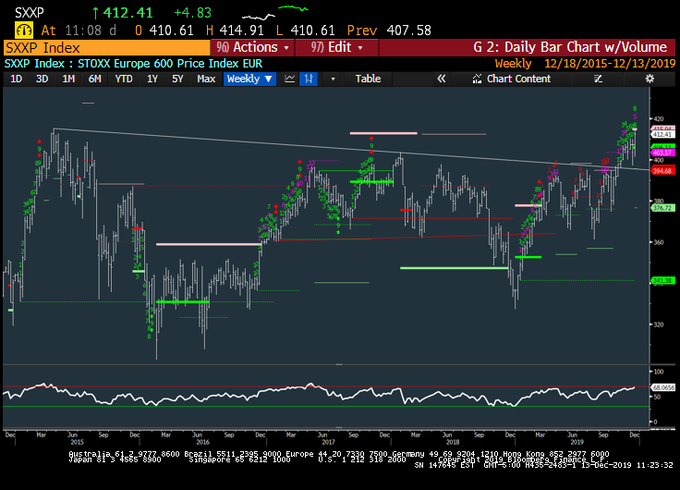

First a top of channel risk? A S&P chart from Market Ear:

Mark Newton likes the move in Commodities & Emerging Markets:

- Mark Newton@MarkNewtonCMT – Both #Commodities and #EmergingMarkets have ripped higher in recent days and near-term extended, but good moves in both– $CCI index- Thomson Reuters Equal-weighted Commodity index within 3-5 days of ST peak, but overall a very good technical move newtonadvisor.com

What about Oil, that special commodity?

- Mark Newton@MarkNewtonCMT – Crude oil (WTI) is finally pushing up above the key 60 level (Jan futs) & seeing constructive price action out of Brent and Gasoline- I had argued AGAINST Energy being at a bottom on CNBC this wk, but if Energy commods breakout, a bounce is likely around the corner, SHORT_TERM

But he expects a fade in Europe:

- Mark Newton@MarkNewtonCMT – Europe has outperformed US this past week, & the constructive breakout from Nov now closing in on Strong resistance at 2015 highs, w/ exhaustion due next week on Weekly and Daily- Expect stalling out in Europe as of Dec Expiration

4. UK Election

Just to remind ourselves, look what we had written on June 25, 2016 after the first Brexit election:

- “Well, the English people stormed their own proverbial Bastille or more appropriately demolished the new Berlin Wall that had imprisoned them. To paraphrase Nigel Farage, Thursday June 23 was the day England declared its independence by cutting the chains of group-think that imprison today’s world.“

- Every “elite” champion had come out against the Brexit vote. Every “intellectual”, every think-tanker, every globally elite “journalist” had publicly warned the English to vote for remaining within the new Berlin Wall of Euro-globalism. Gillian Tett, the US managing editor for the Financial Times of London, said she could produce a list of 100 economists who support remaining within Europe. Talk about group-think. The English people gave them the proverbial finger & declared their mental independence. By doing so, England became a beacon for others in Europe who are forced to remain beholden to neo-colonial rulers from Brussels”.

Just as we have seen with PM Modi of India, the first election that breaks out of mental servility to the global elite is not enough. For true mental independence from global group-think, the society needs a second & bigger election triumph. India & PM Modi got that in 2019 & you see results that you did not see after the first victory in 2014.

On Friday, in the second Brexit election, the English people demolished the hold of their European masters in Brussels & thunderously proclaimed their independence from the European Union. With this great triumph, PM Boris Johnson can now negotiate a smarter & stronger exit from the EU.

That brings on deck the third & most important breakout of the people of the most important country on earth in November 2020.

But for today allow us to enjoy the consistent & arrogant stupidity of the flag bearer of the global “elite”:

- Lawrence McDonald@Convertbond – Can anyone explain how the most Trump like political power base in Europe just won a landslide election in the UK?

To paraphrase what Ari Fleisher said on Laura Ingraham’s show on Friday:

- “The Economist is the most known & read publication in England that doesn’t understand England [or America or India, we might add]“

By the way, Mike Bloomberg imported the previous managing editor of The Economist (who had been wrong about Modi 2014, Brexit 2016, Trump 2016) and made him the managing editor of Bloomberg.com. Does that say anything about how well Candidate Bloomberg understands America? We will find out soon enough.

PS: The actual & well put statement from Mr. Fleischer was – The Press is the biggest institution in America that doesn’t understand America.

Send your feedback to editor@macroviewpoints.com Or @MacroViewpoints on Twitter