Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

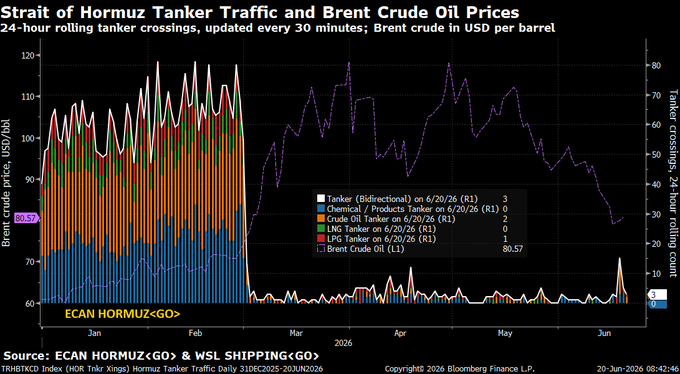

1. The figure that matters the most

What we saw on Friday, June 20:

- Michael McDonough@M_McDonough – Friday 6-20 – *6/20 Hormuz Tanker Crossings — Post-MOU Momentum Plunging* 🚢🛢️Today’s chart isolates Strait of Hormuz crossings by tanker class: Crude, Chemical, LNG, LPG. The initial post-deal surge is losing steam. After peaking at 15 tankers on June 18th, crossings dropped to 5 (reposted by Ryan Detrick)

In our humble opinion, nothing matters to financial markets more than the above number of crossings. Until it goes higher & stays higher, we see no point in speculating about what might happen on Monday June 22.

2. Markets Last Week

2.1 US Indices:

- VIX down 7% to 16.44; Dow up 1.1%; SPX up 94 bps; RSP down 80 bps; NDX up 2.6%; RUT up 1.2%; MDY down 39 bps; XLU up 52 bps; SMH up 6.4%; SOXL up 19%

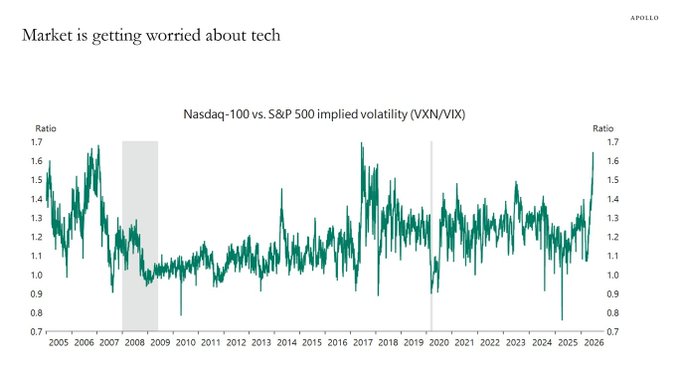

Nasdaq vs. SPX vol:

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – Options Markets Are Bracing for a Tech Shakeout -Torsten at Apollo; Nasdaq volatility relative to the S&P 500 has spiked to its highest level in many years.

And,

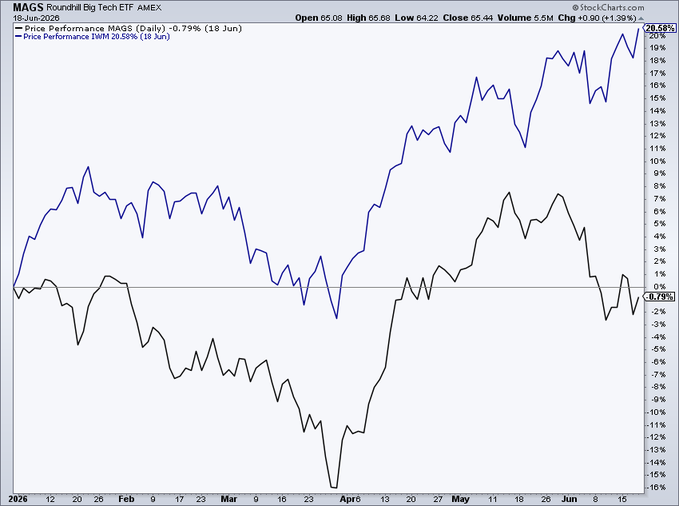

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – The Russell 2000 is up 21% YTD; The Mag 7 ETF is down 1%; $IWM $MAGS

2.2 MAG 7:

- AAPL up 2.4%; AMZN up 2.1%; GOOGL up 2.3%; META up 1.8%; MSFT down 2.9%; NFLX down 3.7%; NVDA up 2.7%; MU up 15.5%;

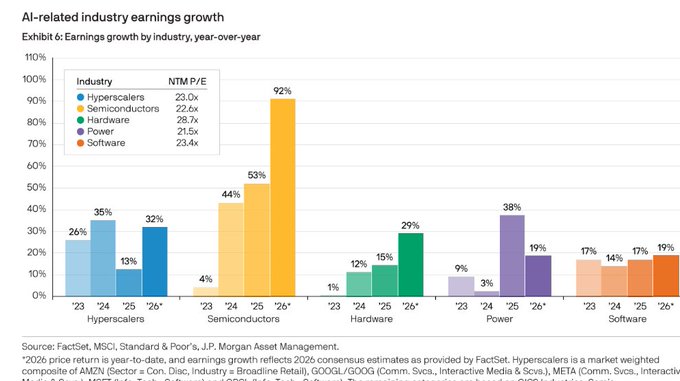

Hmm! Is this a picture of earners vs. spenders?

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – Semiconductors’ EPS growth 92% this year; Power EPS growth actually decelerating JPMAM $SMH $SOXX #AI

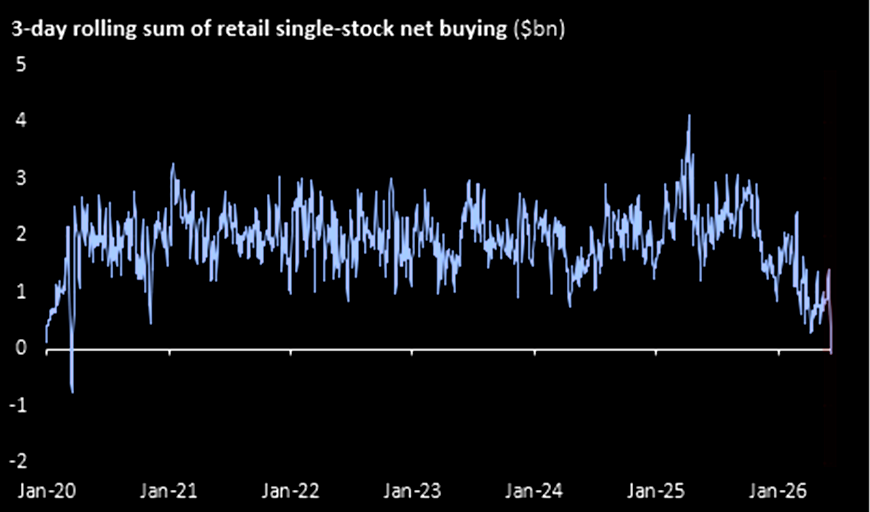

What about the Retail investor?

- The Market Ear@themarketear – Retail not roaring – Retail’s single-stock net buying has fallen to the lowest (on a 3-day rolling basis) since COVID. And if you strip out the SpaceX buying from retail over the past two trading days, there was not much more buying across the rest of the market.

2.3 Key Financials:

- BAC up 32 bps; C up 2.3%; GS up 3.2%; JPM up 1.4%; KRE down 2.3%; EUFN down 31 bps; SCHW up 2.5%; APO up 4.6%; BX up 6.5%; KKR up 3%; XHB up 3.9%; ITB up 4.4%; NAIL up 12.6%; IGV down 5.4%; CRM down 10.7%; PANW up 2.8%; NOW down 9.2%

2.4 – Dollar & Metals

Dollar was up 1.3% on UUP & up 1% on DXY:

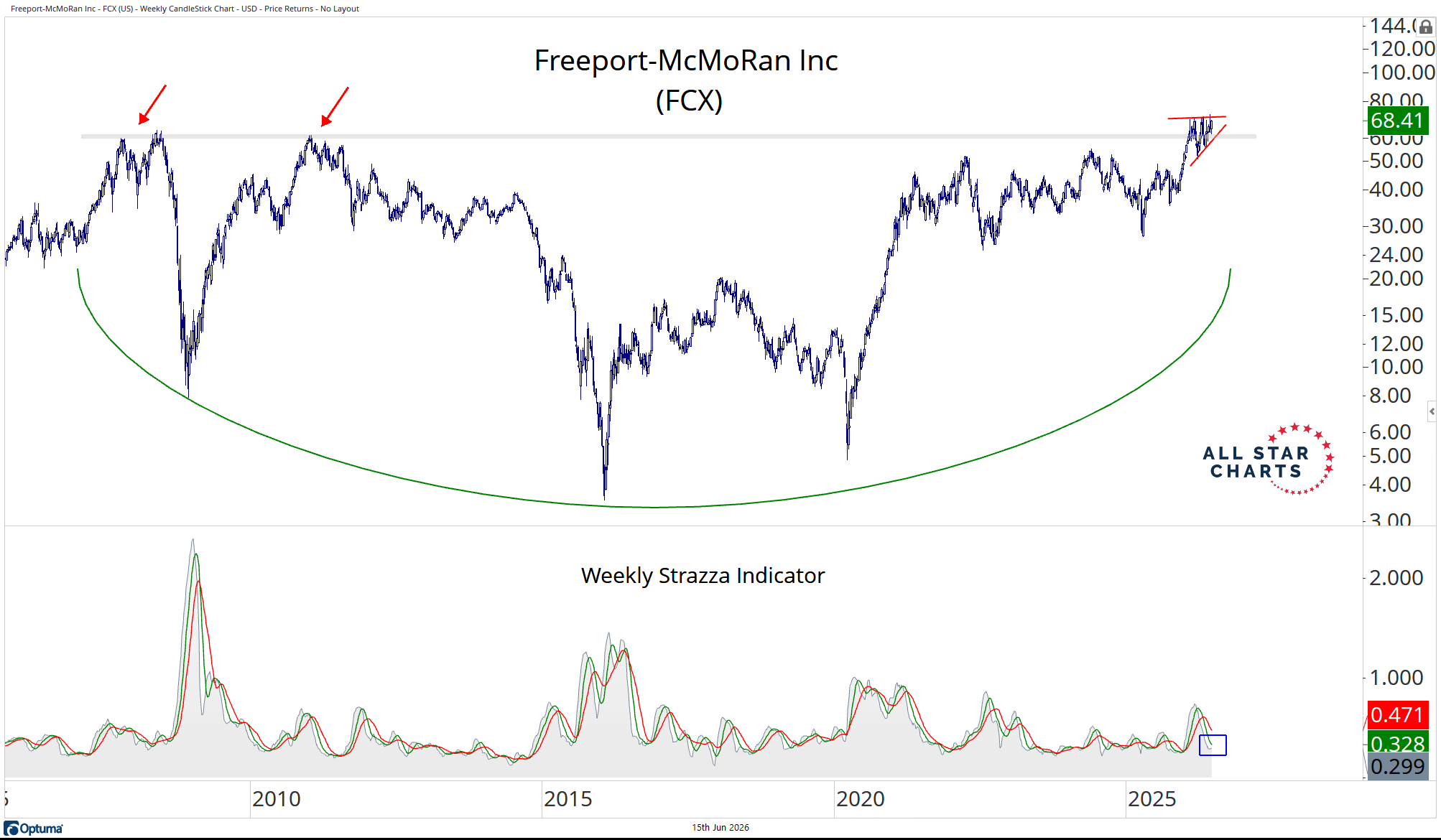

- Gold up 17 bps; GDX up 3.1%; Silver down 3%; Copper down 1.5%; CLF down 10.9%; FCX up 39 bps; MOS up 93 bps; Oil down 9%; Brent down 8.4%; OIH down 10%; XLE down 6.6%;

An idea?

- The Strazza Letter – FCX – Freeport-McMoRan is putting the finishing touches on one of the cleanest GFC bases anywhere in the market. After last year’s run, it’s been coiling at a key level. Digesting the move as momentum resets.

2.5 – International Stocks:

- EEM up 4.3%; FXI down 5.6%; KWEB down 4.7%; EWZ down 3.9%; EWY up 11%; EWG down 1.9%; INDA up 2.6%; INDY up 1.9%; EPI up 2.3%; SMIN up 3.5%;

Oil was down; Interest Rates were down; Which beaten-down asset price rallied? The Indian Rupee rose to 94.3 in a 5-day rally. And according to last computed figures, India received $137 billion in inward remittances while no other country received more than $100 billion. And, for the recent G7 meeting, France has designated India as a top-priority strategic partner &, because of this status, New Delhi was granted rare access to sit at every single major working session. The Indian stock market has been among the worst performing nations so far this year. We will see if that changes.

And Reliance Jio announced their plan to launch 1,600 LEO Satellites to create India’s own Space Internet Ecosystem along with its massive IPO.

On the other hand, Chinese tech ADRs keep getting roughed up. And the China macro story keeps getting rougher at least in the ASEAN region. We don’t know much about China & its neighborhood and perhaps neither does Daily Jagran:

2.6 Treasuries & Interest Rates – Happy Days are here Again?

- 30-year Treasury yield down 7.3 bps on the week; 20-yr yield down 6.7 bps; 10-yr down 3.2 bps; 7-yr down 0.7 bps; 5-yr up 1.6 bps; 3-yr up 5.3 bps; 2-yr up 9 bps; 1-yr up 13.5 bps;

- TLT up 1.1%; EDV up 2.1%; ZROZ up 2.3%; HYG up 9 bps; JNK up 9 bps; EMB up 38 bps

But for the Hormuz mess during the past 2 days, we would have not inserted the :”?” in our Happy Days quote above. It is pretty simple. A new Fed Chair who promises Price Stability is a Chair that makes us look at the 30-year Treasury Bond again. Interesting Gundlach also said that in his usual post-FOMC segment. The other positive about Warsh is that he is going to be Greenspanian at least in terms of “obfuscation“. That is another reason we seriously doubt will get a Fed Hike soon. subject obviously to the Hormuz mess & where Oil prices goes because of that.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.