Summary – A top-down review of interesting calls and comments made last week in Treasuries, monetary policy, economics, stocks, bonds & commodities. TAC is our acronym for Tweets, Articles, & Clips – our basic inputs for this article.

Editor’s Note: In this series of articles, we include important or interesting Tweets, Articles, Video Clips with our comments. This is an article that expresses our personal opinions about comments made on Television, Tweeter, and in Print. It is NOT intended to provide any investment advice of any type whatsoever. No one should base any investing decisions or conclusions based on anything written in or inferred from this article. Macro Viewpoints & its affiliates expressly disclaim all liability in respect to actions taken based on any or all of the information in this article. Investing is a serious matter and all investment decisions should only be taken after a detailed discussion with your investment advisor and should be subject to your objectives, suitability requirements and risk tolerance.

1. Geo-Challenges & Movements

Despite what we cover in the market sections below, the overriding factor for global markets is the conflict between USA & Iran. Some like Warren Pies of 3Fourteen say (see Section 2.1 below) :

- “My view is the war is done; there is no appetite for further escalation; its just a matter of how that MoU gets massaged for the public”

If this turns out to be true, markets could be in a surge ahead. But it could be a different story if the conflict between Israel & Iran escalates & drags in the US.

On a different topic, look how Secretary of War Hegseth hailed “‘Powerful India’ defending National interests, praised growing military prowess“:

- “… And in South Asia, India is a critical anchor to hold the line. A powerful India acting in its own self-interest advances our shared goal of maintaining a balance of power across the region. India is modernizing its military to carry its share of the security burden, particularly in the Indian Ocean. It’s building out the heavy industrial and logistics capacity to sustain high-end military operations, including the ability to repair and maintain our shared platforms and support US Navy vessels operating forward in the theater. We’ve also committed to pursuing co-production with India to advance capabilities like Javelin anti-tank guided munitions. real tangible steps to improve the collective readiness of our forces.“

Look what happened a couple of days before the above – a strategic US-India partnership to secure the global supply chain for these essential minerals:

Moving east, recall our discussion of the visit of Vietnamese President & General Secretary To Lam to India between May 5-May 7. It was speculated then that one of the main topics was purchase by Vietnam of Brahmos missiles, one of the fastest supersonic ballistic missiles in the world. Guess what happened 2 days ago:

- “India has confirmed that Vietnam has signed a deal to acquire the BrahMos supersonic cruise missile system, while negotiations with Indonesia are in the final stages. Defence Secretary Rajesh Kumar Singh revealed the development at the Shangri-La Dialogue in Singapore. “

Vietnam is adjacent to China & has fought a successful war against China’s invasion. So this is not a faraway development for China. It brings supersonic cruise missiles adjacent to China. On the other side of the South China Sea is Philippines, one of the earliest countries to purchase India’s Brahmos missiles. Further south lies Indonesia which sits on top of the Malacca Straits and, as the clip above says, they are at final stages of acquiring Brahmos.

When it comes to the Middle East, everyone knows that Religion plays a major role in geopolitics. But many forget that Buddhism is a major religion in South East Asia & it is centered in India, north-eastern part of India. So it should surprise no one that, in his first-ever visit to India, Myanmar President first visited the MahaBodhi temple in Bodh Gaya.

A simple 1:30 minute clip like the below can do far more to cement positive image of India in the people of Myanmar.

What are the non-religious topics that are relevant to stronger relations between Myanmar & India? Rare Earth minerals that Myanmar exports in bulk to China.

Now look at the map of Myanmar & its neighborhood. Just as Vietnam is an obstacle for China to get into the south-western part of South China Sea, Myanmar is an obstacle to China’s entry of size into the Bay of Bengal

Remember how, a few years ago, India sent the Sacred Remains of Bhagvaan Buddha to Vietnam so the Vietnamese could see them & worship them. It turned out to be an amazingly successful move that cemented a geo-strategic relationship between Vietnam & India.

Now look what happened 2 days ago.

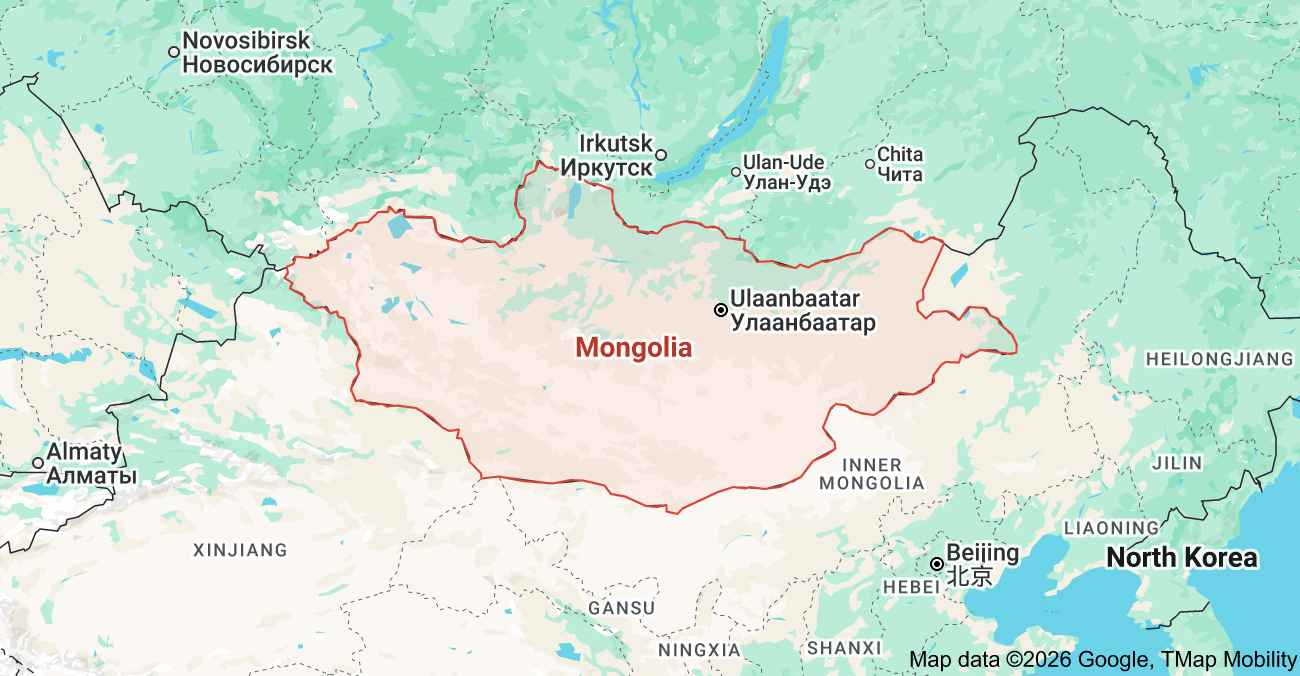

Look at Mongolia’s location below – sandwiched between Russia & China. And, besides Buddhism, it has significant reserves of rare earth minerals. Today Indian companies have to take their shipments north into Russia, then turn east & go down to Vladivostok for shipment to Chennai.

Now ask yourselves whether India’s above outreach is consistent with America’s goals in the above massive region thus endorsing Sec. Hegseth’s statement – A powerful India acting in its own self-interest advances our shared goal of maintaining a balance of power across the region

2.Markets Last Week

2.1 US Indices:

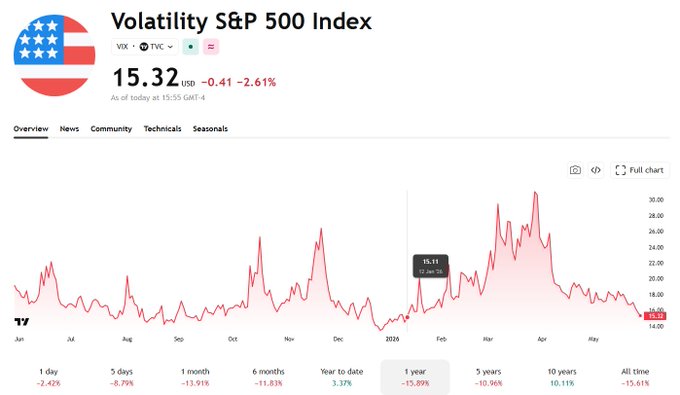

- VIX down 8.7% to 15.32; Dow up 89 bps; SPX up 1.4%; RSP up 1.1%; NDX up 2.9%; RUT up 1.7%; MDY up 1.5%; XLU down 2.1%; SMH up 3.9%; SOXL up 17.7%.

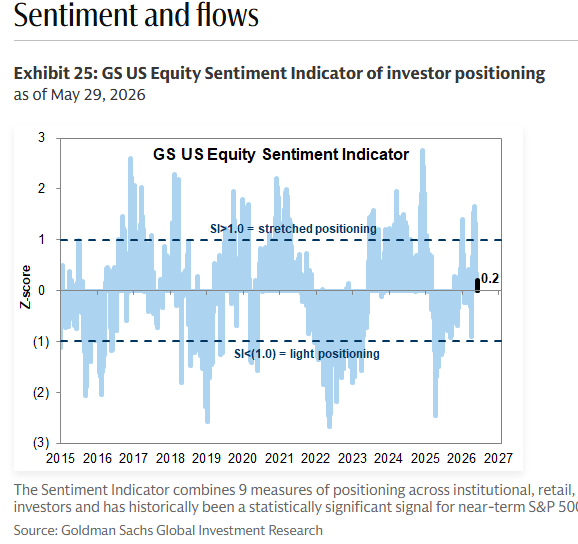

Equity Sentiment?

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – GS US Equity Sentiment Indicator of investor positioning remains subdued

On the other hand,

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – $VIX lowest since January 12th

And,

- Trader Z@angrybear168- $SPY noticeable amount of spike in bearish divergences, a short term shake out would be healthy.

- Trader Z@angrybear168 – $SPY – weekly tension closed bearish, dispersion continues.

Warren Pies of 3Fourteen Research suggests that Equal-Weight S&P might take the baton of the rally from here:

- Our sentiment model is still mildly optimistic & not showing …. a serious top.. the fundamentals behind all this are in good shape; …. that leads me to believe there is more upside here fundamentals supported;

- Regarding Iran Conflict – My view is the war is done; there is no appetite for further escalation; its just a matter of how that MoU gets massaged for the public; I think the market is sniffing it out; ..

- It has been a narrow rally ; there has been a lot of damage to capital markets from the conflict; we have lost probably a billion barrels of inventory; … we have probably put a floor of oil at $30 a barrel higher;

- As a consequence, we have caused the Fed to back off their cut cycle & that’s pushed the rates up; I think all that relaxes a little; we won’t revert to the pre-war level;

- That gives some room for the equal-weighted S&P to rise; the equal-weight S&P is much more rate-sensitive, much more macro-sensitive; the hedge funds that had paired consumer staples, utilities & financials as shorts to their AI longs; I can see some of that exposure rising & shorts closing out; and the equal-weight S&P taking a little bit of the baton over the summer;

- the important thing for the equity market is that we are taking off the right tail away which was scary; so the market probably thinks its not going to be a disaster in the oil market & that’s what is going to allow the market to broaden out

- ;

2.2 MAG 7:

- AAPL up 1.1%; AMZN up 1.6%; GOOGL down 69 bps; META up 3.7%; MSFT up 7.6%; NFLX down 2.9%; NVDA down 2%; MU up 29.3%;

Who would have thunk it?

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – $NVDA & $XLK have moved opposite since mid-May

This week, Ankur Crawford of Alger deigned to speak about $NVDA from an investment perspective:

- “… One of the issues for NVDIA, I think, is that there are bottlenecks in the ecosystem that are beyond the GPU; bottlenecks are now memory; its in the optical space; its how to get information off a chip onto the GPU…. the bottleneck plays – storage, memory, optics that are working; NVDIA is no longer the bottleneck …. its incredibly cheap ; it will eventually work but for now it doesn’t ; ….. “

Last week we expressed our utter frustration with Ankur Crawford. It was an individual frustration & a class frustration, class of small-medium investors. Ms. Crawford has expressed her positive investment views in the past about $NVDA, AppLovin (APP), Nebius (NBUS) and Astera Labs (ALAB), all phenomenal stock calls. Her media appearances were what Louis Rukeyser would have praised. She described the theory and then said buy this.

Now she has forgotten the individual investors or simple folks like us who need both. She has not given viewers a single name in the last 3-4 TV appearances. She just talks above us. We don’t like it and we are frustrated at the lack of buy-hold-sell type simple stuff.

Having said that, it seemed evident to simpletons like us that Ms. Crawford is no longer bullish on the names she made her media career on. Instead of saying Hold, she goes into phrases like “long arc of time“. We understand her “be patient” message but it should have some flavor to where or why she would say buy. One exception was driven by CNBC’s Scott Wapner who asked her “Micron – if you don’t own the name yet, can you?” Her reply – “I think you have to be just patient & wait; … it will give you opportunities“.

And then CNBC did its own thing- at the end of the live conversation, there was good conversation about Nebius (NBUS). That entire conversation was deleted from the posted clip above. What was it in that conversation that CNBC & Ms. Crawford wanted to hide from view of simple viewers like us? Has Ms. Crawford sold it already & not told CNBC’s viewers?

2.3 Key Financials:

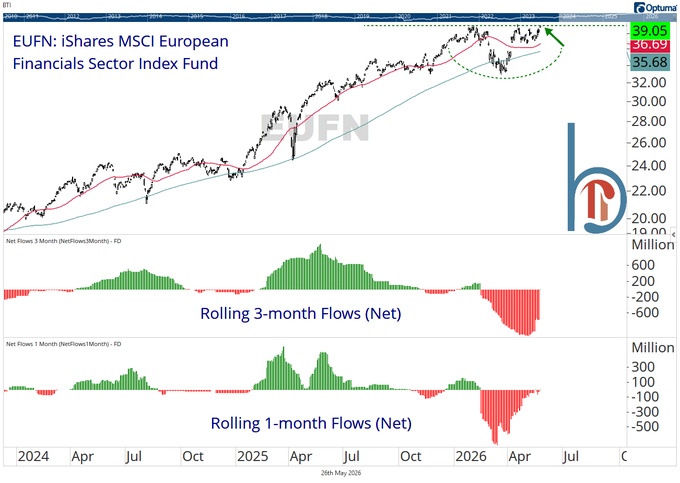

- BAC down 39 bps; C up 65 bps; GS up 2.9%; JPM down 2.3%; KRE up 35 bps; EUFN up 92 bps; SCHW down 3.1%; APO up 16 bps; BX down 1.3%; KKR up 2%; XHB up 2.6%; ITB up 2.3%; NAIL up 6.6%; IGV up 8.1%; CRM up 6.1%; PANW up 8.1%

- Scott Brown, CMT@scottcharts – May 26 – European financials breaking out with plenty of room for sentiment to get more aggressive

2.4 – Dollar & Metals

Dollar was down 40 bps on UUP & down 42 bps on DXY:

- Gold up 1.6%; GDX up 5.4%; Silver down 18 bps; Copper flat 6.40; CLF up 21.1%; FCX up 6%; MOS up 6.2%; Oil down 8.9%; Brent down 11.4%; OIH down 5.8%; XLE down 5.4%;

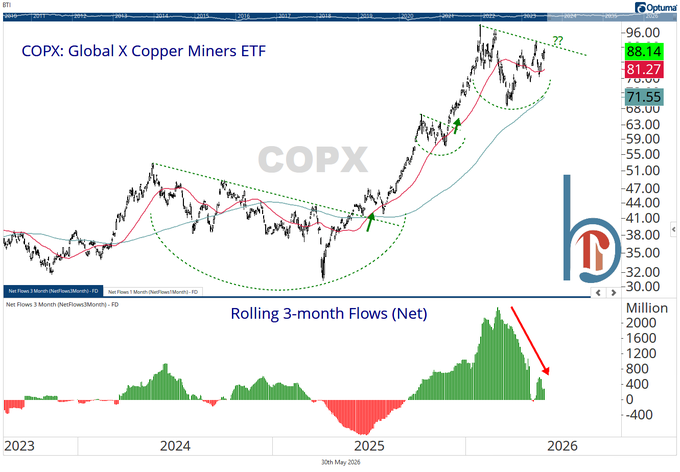

Did $FCX & $CLF provide a signal?

- Scott Brown, CMT@scottcharts – After a big sentiment reset, copper miners may be ready for another leg higher

2.5 – International Stocks:

- EEM up 4.1%; FXI down 1.3%; KWEB down 67 bps; EWZ down 1.3%; EWY up 13.1%; EWG up 1.2%; INDA up 35 bps; INDY up 35 bps; EPI up 45 bps; SMIN up 1.1%;

One of the more interesting views came from Mary Ann Bartels who argued that a 15-20 year secular bear market will begin in US around 2030 and a new Secular Bull Market will start in Japan, Europe, EM-ex-china providing a one of the greatest opportunities in history to diversify outside US.

In Section 1 above, we discussed some macro themes that might benefit India & Indian Economy in the future. But are current investors rethinking their posture re India at this time? Carson Block of Muddy Waters speaks in sensible detail about his recent thinking re investing in India on Bloomberg (starting at minute 15:04 of the clip below).

Carson Block says:

- “look, there are several factors at play. Obviously, recently, the concerns over the Iran the Iran war and the Strait Of Hormuz and energy crisis, that’s certainly India is very exposed to that. But, also, I think AI has been in concerns over what AI is going to do to, Indian outsourcing industry and Indian software industry. That’s been part of it as well.”

- “And, like this was a market that was very richly valued. So, I think, you know, as as much as we have a view on what’s gonna ultimately happen to the labor market in The US, You know, we are still trying to figure out who are the winners, who are the losers going to be. And I think that that’s really you know, that’s also a really complex question in India.”

- “But, there’s still a very good story there. We are still excited about India over the long term. But, and look, from a long term perspective, valuations coming in there, it’s not a bad thing. But we are reevaluating how we would approach India in light of our house view on on AI and how it’s gonna impact labor markets, … especially with India, damage to a number of the companies that have done software outs outsourced software development and BPO outsourcing.”

We think Carson Block is mostly right. To amplify what he is saying, biggest problem for us is that big ETFs, INDA, INDY, EPI etc. are heavily heavily weighted in the outsourcing software companies & in private banks, two of the worst sectors in terms of current growth. On the contrary, Big Defense Stocks that build fighters, battleships & Port Infrastructure companies are in a bull market. And there has been a crazy market in options of small drone producers. These stocks behave similarly to crazy cheap stocks in US.

At the same time, we agree with Carson Block that valuations coming down is not bad thing especially if you combine that with incoming investment growth. Speaking of investment growth:

The above clip points out that,

- “India recorded its highest-ever gross foreign direct investment (FDI) inflow, reaching $94.5 billion in FY26, marking the fastest economic growth in six years. This surge demonstrates significant global investor confidence and is driving substantial investment in India. The increase in FDI is directly contributing to the establishment of new factories, job creation, and the development of industrial parks across the Indian economy, signaling robust growth for the nation.”

We all know that Oil is a problem given the Iran conflict. Has that meant a boost for solar? The clip below suggests yes:

What about Natural Gas?

The clip says:

- India’s BIG Gas Discovery in Thar Desert? Rajasthan Becomes New Energy Powerhouse A major natural gas discovery in Rajasthan’s Thar Desert has put India’s energy sector in the spotlight. Oil India Limited has found a new gas reserve in Jaisalmer’s Dandewala region, close to the India-Pakistan border. The discovery at shallow depth could strengthen India’s energy security, reduce import dependence, and boost Rajasthan’s industrial growth. From the harsh conditions of the Thar Desert to the strategic importance of the Dandewala gas field, this video explains why this discovery matters for India’s future.

What about geothermal energy?

The clip says:

- “India has achieved a major breakthrough in Ladakh’s Puga Valley as ONGC successfully taps geothermal energy at 14,000 feet near the LAC. This strategic project can provide nonstop power to Indian military infrastructure in extreme weather conditions and reduce dependence on fuel logistics. The discovery is being seen as a major game changer against China in the high-altitude region. From energy security to military advantage, this project could transform Ladakh into India’s biggest energy fortress.”

2.6 Treasuries & Interest Rates:

- 30-year Treasury yield down 8.4 bps on the week; 20-yr yield down 9.9 bps; 10-yr down 11.7 bps; 7-yr down 11.4 bps; 5-yr down 11 bps; 3-yr down 11.8 bps; 2-yr down 11.7 bps; 1-yr down 7 bps;

- TLT up 1.3%; EDV up 1.8% ; ZROZ up 1.9%; HYG up 50 bps; JNK up 54 bps;

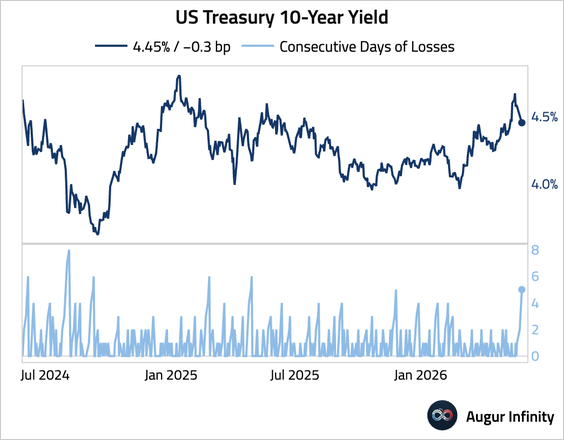

Rates were not merely down on the week but down every day of the past week:

- Mike Zaccardi, CFA, CMT 🍖@MikeZaccardi – US Treasury 10-year yield fell for five consecutive days. @augurininfinity https://augurdigest.com/p/augur-digest-253

And Income?

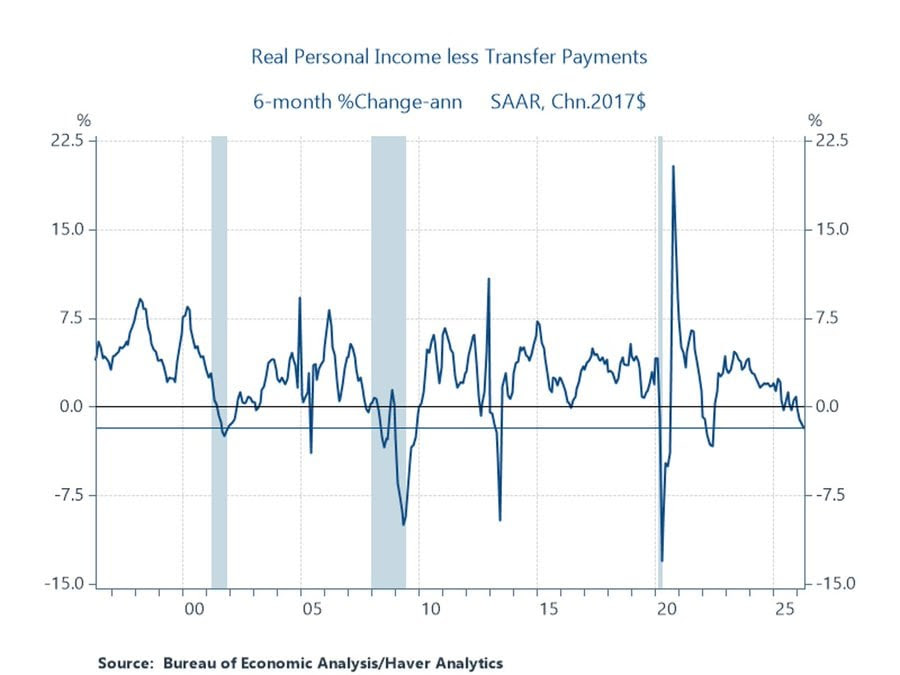

- Augur Infinity@AugurInfinity – 🇺🇸 Real disposable income growth declined for three consecutive months.

In a bit more detail from RenMac:

- Consumer running on fumes? Real personal incomes ex transfers fell 0.4 percent, the fourth decline in five months and the peak appears to be September 2025. Over the last six months, real incomes ex transfers have declined 1.8 percent. Historically, this is not good news.

What about housing?

- David Rosenberg@EconguyRosie – After today’s news that new home sales collapsed by -6.2% in April to a three-month low of 622k annualized units, I must observe that it really says something about the state of the U.S. residential real estate market that they are lower now than they were in late 2007, when the unexpected housing-led recession began to take hold.

Watch & Listen to David Rosenberg lecturing CNBC’s Sara Eisen after Thursday morning’s economic data:

Mary Ann Bartels also discusses her views on interest rates in the clip described in Section 2.5 above. Looking at the 10-year triangle, she says “if you break 4.60% on the upside, then you get to 5%-6%; but if you break 3.6% on the downside, rates are going lower“.

As we recall from an earlier presentation of hers, she thinks we are more likely to go lower but she says that would be the bottom of rates for a long time.

Send your feedback to editor.macroviewpoints@gmail.com Or @MacroViewpoints on X.